The 2–3 Year Window: What Banks Lose by Waiting on AI

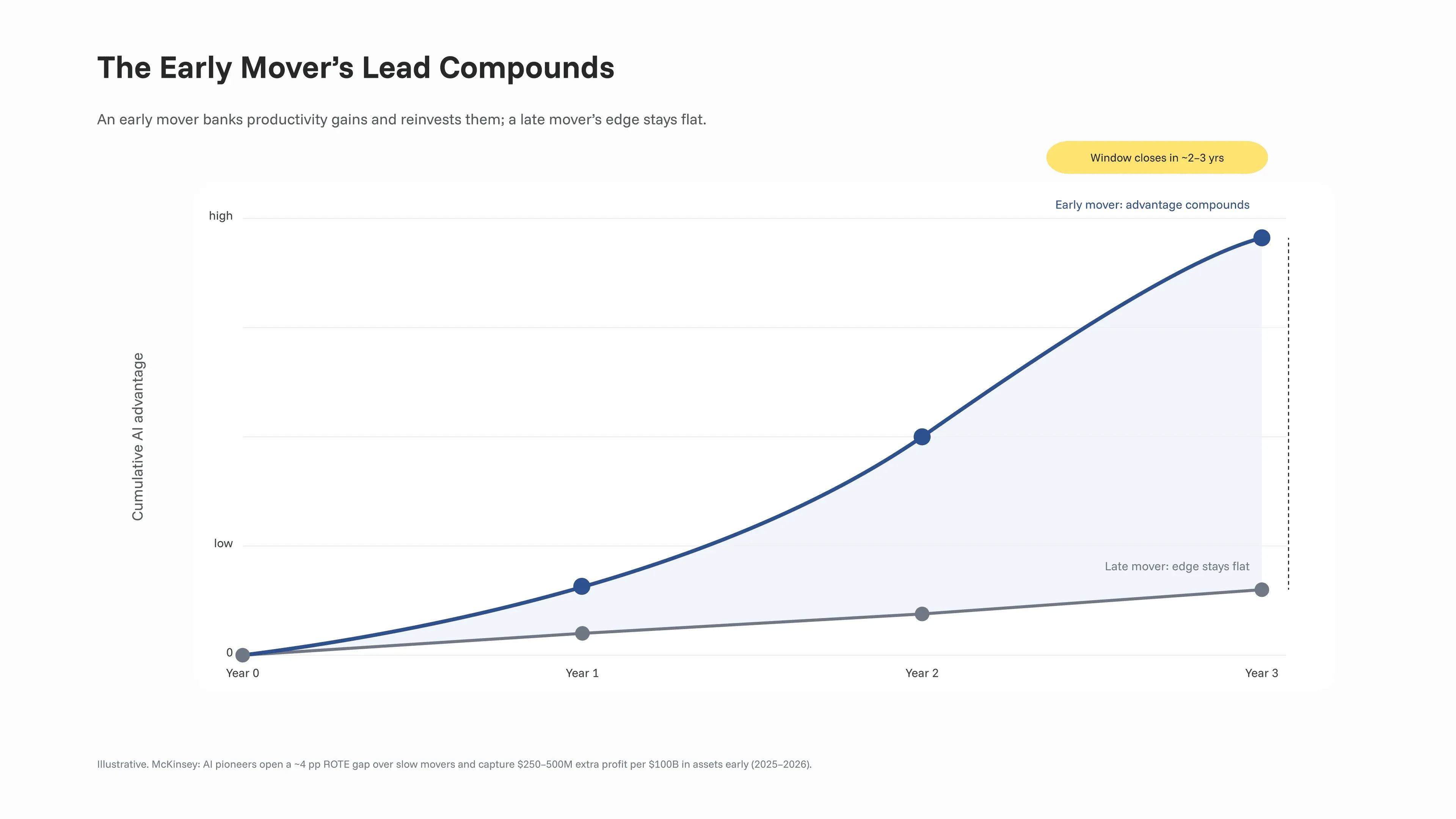

Most conversations about the future of AI in banking are framed as a question of whether — whether the models are ready, whether the use cases are proven, whether the regulators will allow it. That framing is already out of date. The more useful question is when, because the advantage AI creates does not sit still and wait to be collected. It compounds.

McKinsey estimates that AI pioneers can open a gap of four percentage points of return on tangible equity over slow movers — capturing years of productivity gains before the advantage normalizes (McKinsey, 2025 (opens in new tab)). We have argued before that digital banks were structurally winning before AI (opens in new tab) and that AI multiplies that gap rather than adding to it (opens in new tab). This article is about the consequence both point to: a closing window of roughly two to three years, and what a bank loses for every quarter it spends inside it without moving. The real decision is no longer “should we buy software” — it is “how fast can we build and change,” and that is a decision about the programmable building platform underneath the lending business, not about the next pilot.

Executive summary

- The lead compounds — it doesn’t accumulate. McKinsey estimates AI pioneers can open a four-percentage-point return-on-tangible-equity gap over slow movers, capturing years of productivity gains before the advantage normalizes — while a slow mover is left with an uncompetitive cost base (McKinsey, 2025 (opens in new tab)).

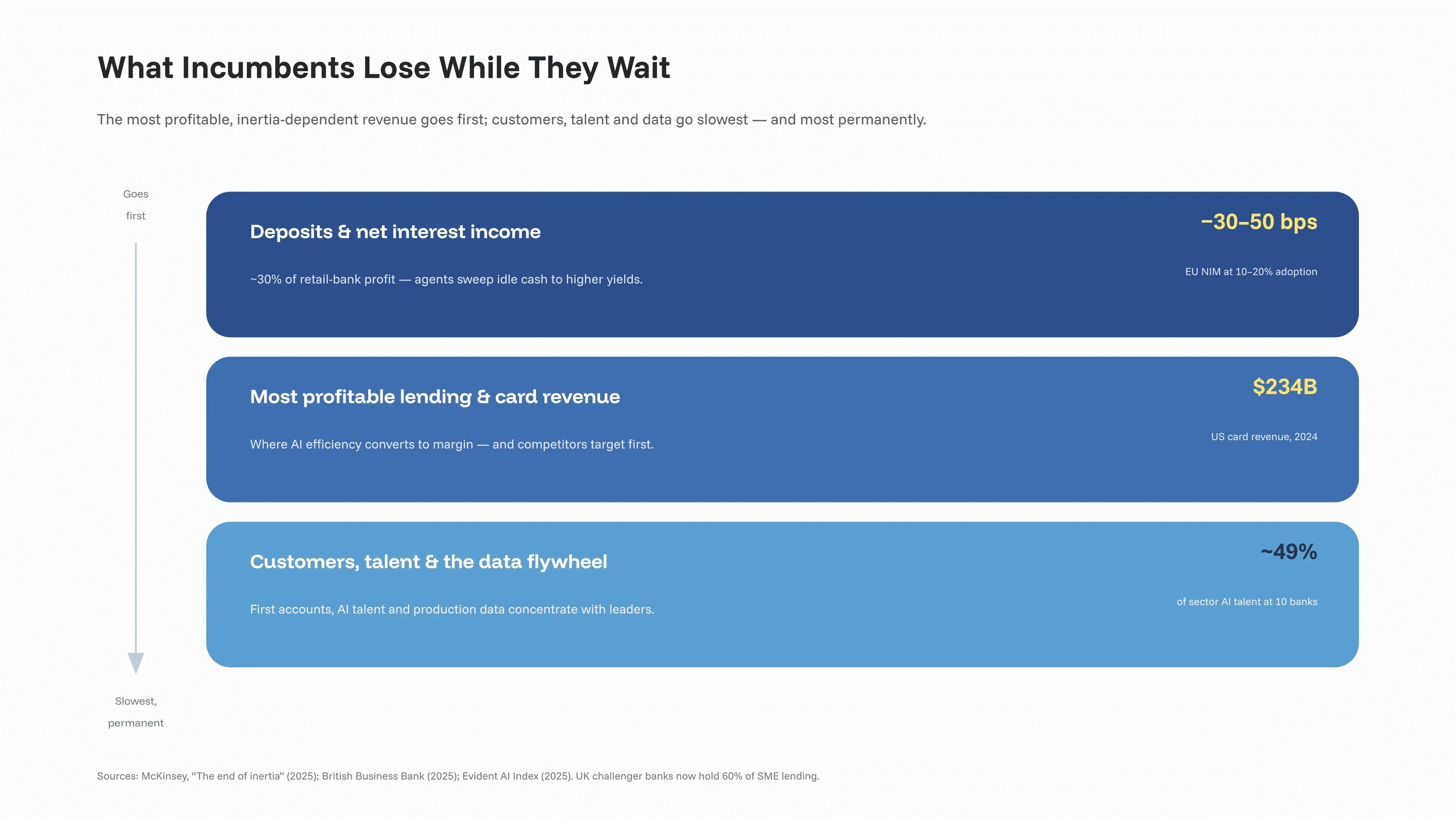

- The most profitable layers erode first. McKinsey projects global banking profit pools could shrink by as much as 10% over five to ten years if banks fail to respond. The most exposed engines are inertia-dependent: net interest income on deposits — roughly 30% of retail-bank profit — and credit-card economics, which generated $234 billion in US revenue in 2024 (McKinsey, 2025 (opens in new tab)).

- The window is roughly two to three years. It is set not by how fast the technology moves but by how fast a leader’s advantage in cost, customers and data becomes irreversible.

- “Wait and see” is not neutral. With most AI pilots never reaching production, doing nothing while running pilots feels like motion but functions as standing still — and standing still is choosing to fall behind while competitors iterate past you.

What the 2–3 year window actually is

The window is not a countdown on the technology. The models are commodities; everyone can buy them. The window is a property of competition: in a race where speed of adoption is the deciding variable, the lender that builds, launches and changes fastest wins its cohort, and everyone else loses ground that compounds quarter over quarter.

That is what makes it a window rather than a trend. A trend you can join late. A compounding advantage you cannot, because the gap you face when you finally move is larger than the gap that existed when you decided to wait. The lead is path-dependent: each quarter of delay raises the cost of catching up and lowers the odds that catching up is even possible.

The macro evidence is already pointing this way. McKinsey estimates that global banking profit pools — roughly $1.2 trillion — could shrink by as much as 10% over the next five to ten years if banks fail to reinvent their business models, and warns plainly that slow movers “will be caught out with an uncompetitive cost base in a rapidly changing market” (McKinsey, 2025 (opens in new tab)). The window is the time you still have before that compression hardens into positions that cannot be recovered.

What incumbents lose while they wait

The cost of waiting is not abstract, and it is not paid all at once. It is paid layer by layer, and the layers that go first are the most profitable ones. This is the part of the future of AI in banking that rarely gets quantified — so here is what actually erodes, and in what order.

Deposits and net interest income

The “sticky” money banks have relied on for decades is no longer guaranteed. Net interest income on deposits accounts for roughly 30% of retail-bank profit, and it rests on customer inertia — most depositors never move cash to chase a better rate. AI agents remove that inertia: they monitor balances, compare rates and sweep idle cash to higher yields automatically. McKinsey estimates that in Europe, where the deposit revenue pool exceeds $100 billion, even 10–20% adoption of agent-driven cash sweeps could tighten bank net interest margins by 30–50 basis points (McKinsey, 2025 (opens in new tab)). This is the layer that hurts first and hurts most.

The most profitable lending and card revenue

Lending and cards are where the pressure concentrates, because that is where margin lives. Credit cards generated $234 billion in US revenue in 2024 — interest, interchange and unredeemed rewards — held together largely by inertia, with more than 20% of cardholders redeeming no rewards at all in a year (McKinsey, 2025 (opens in new tab)). The share shift is already visible at market level: in the UK, challenger and specialist banks reached a record 60% of SME lending in 2025, leaving incumbents — who held 61% as recently as 2012 — with less than half the market (British Business Bank, 2025 (opens in new tab)). Lending is precisely where AI-driven efficiency converts into margin — which is why it is both the layer most worth defending and the layer competitors target first.

Customers, talent and the data flywheel

The slowest-looking losses are the most permanent. Younger customers are forming their first banking relationships with digital players — Millennials and Gen Z already make up roughly 78% of the global neobank user base — and a first account opened at 22 can anchor decades of lending and deposit relationships (eMarketer, 2026 (opens in new tab)). At the same time, AI talent concentrates with the leaders: the top ten banks in the Evident AI Index hold close to half of the sector’s AI talent (Evident, 2025 (opens in new tab)). And the mechanism underneath both is a flywheel — fewer customers and fewer production deployments mean less data, which means weaker models, which means fewer customers. It spins in favor of whoever is already ahead. In the euro area, digital banks’ aggregate share has climbed from 3.1% in 2019 to 3.9% in 2024 — still modest, but moving in one direction only (European Parliament, 2026 (opens in new tab)).

Why the window is closing now, not in ten years

If the losses are gradual, why is the window only two to three years? Because the advantage on the other side is not gradual — it is front-loaded. McKinsey estimates that a bank getting ahead early can capture $250 million to $500 million of additional profitability per $100 billion in assets, banking years of productivity gains before pricing compresses and the advantage normalizes (McKinsey, 2026 (opens in new tab)). Those are the economics of a first-mover advantage: the returns are largest while few competitors have moved, and they shrink as the field catches up.

Those returns are largest while few competitors have moved, and they shrink as the field catches up — McKinsey is explicit that the extra profitability “will be competed out” through pricing compression once attackers force the issue. The fintech revenue trajectory makes the pressure concrete: fintech revenues grew 22% from 2021 to 2025 against 5% for incumbent banks, lifting their share of industry revenue toward 17% (McKinsey, 2026 (opens in new tab)). Every quarter that differential persists, the base a late mover has to defend gets smaller and the lead they have to close gets larger. That is why “later” is not a smaller version of “now” — it is a structurally harder problem.

Why “wait and see” is the most expensive option

The instinct in a regulated, risk-managed institution is to wait for certainty. But the costs here are asymmetric. The cost of acting is bounded and predictable: a scoped implementation, on a known timeline, with a known budget. The cost of waiting is unbounded and partly irreversible: it compounds with the leader’s advantage and includes customers, talent and data that do not come back. When one option has a capped downside and the other has a downside that grows the longer you hold it, “wait and see” is not the cautious choice — it is the expensive one.

What makes the trap subtle is that waiting rarely looks like waiting. It looks like a portfolio of pilots. But pilots on a frozen base do not move the business. Roughly 70% of bank IT budgets go to maintaining technical debt rather than building new capability (Accenture, 2026 (opens in new tab)), and the large majority of AI initiatives never translate into impact: MIT Media Lab’s Project NANDA found that 95% of organizations saw no measurable return on their generative-AI investment (MIT, 2025 (opens in new tab)), and Gartner projected that at least 30% of generative-AI projects would be abandoned after proof of concept by the end of 2025 (Gartner, 2024 (opens in new tab)). The activity is real; the movement is not. As we put it in the work behind this series: every month a change sits in a queue is a month a competitor is already live with it.

| Wait and see (status quo) | Move now (programmable, AI-native) | |

|---|---|---|

| Launching or changing a product | Weeks to quarters in a vendor or engineering queue | Days, by the lending team itself |

| Inertia-dependent revenue (deposits, cards) | Margins compress as agents optimize balances (EU NIM −30–50 bps at 10–20% adoption) | Defended, plus new net interest margin |

| The leader’s advantage | Compounds against you (pioneers +4 pts ROTE) | You are on the compounding side of it |

| What AI multiplies | A frozen base — so close to nothing | A programmable base — so the gains land |

| Trust and audit | Exposure to “the model said so” | Deterministic, explainable decisions with shadow testing |

Numbers in this table are drawn from the sources cited above; vendor names are intentionally omitted.

What closing the gap actually requires: speed without losing control

If the window is real, the response that fits it is not another pilot. It is a change in how fast the institution can build and operate lending — without giving up the auditability a regulated lender requires. Those two requirements usually trade off against each other. Resolving the trade-off is an architectural question, and it is the whole point of a building platform.

A programmable, AI-native building platform gives lending teams deterministic credit primitives they compose into any product, risk model or workflow, with AI woven through the build itself. The distinction that matters is between configurable and programmable. Configurable software lets you pick from options a vendor pre-built — and bolting AI on top only makes the menu smarter; you are still choosing from someone else’s menu. A programmable foundation lets your own team change the underlying logic. It is the difference between a smarter menu and an open kitchen.

This is where timveroAI operates: a RAG-grounded implementation agent that accelerates building and changing the lending system, with human-in-the-loop approval gates and a shadow-run mode that tests AI-generated changes before they go live. Critically, the credit decision itself does not run on a language model that can hallucinate a confident-but-wrong answer. It runs on deterministic, explainable primitives — the same inputs always produce the same auditable output. The formula is AI for speed, deterministic logic for the decision. (timveroAI is an implementation agent, not a credit-scoring engine — a distinction important enough that we treat it separately.)

The urgency cuts both ways, which is why the window matters regardless of where a bank sits. For an incumbent, speed is defensive: match the pace of leaner challengers before more of the book walks out the door. For a digital bank, the same window is offensive — the profitable neobanks are the ones with a real lending engine generating net interest margin, and whoever launches and iterates fastest wins the cohort. Either way, the platform that lets a lender move fastest while staying trustworthy is the one that wins the race.

The proof that the timeline is achievable already exists. Finom, a European business-banking provider serving 200,000+ customers across five EU countries, reached a banking-grade lending operation in four months with 98% process automation on timveroOS (opens in new tab). Four months is inside the window. A multi-quarter replatforming is not.

“The banks asking whether AI is ready are asking the wrong question. AI is ready. The question is whether your platform lets your own team act on it this quarter or next year — because your competitors are answering it this quarter.” — Dmitriy Wolkenstein, CEO, TIMVERO

Frequently asked questions

What is the future of AI in banking — assistance or autonomy?

Both, in sequence. Generative AI assists people inside existing systems; agentic AI acts on the systems themselves, executing multi-step workflows with approval gates. The structural efficiency gains — and the competitive separation between banks — come from the second, which changes what an operation is rather than just speeding up the people in it.

How long do banks have to adopt AI?

Roughly two to three years before early-mover advantages harden into positions that are very hard to recover. McKinsey estimates AI pioneers can open a four-point return-on-tangible-equity gap over slow movers, and that banking profit pools could compress by as much as 10% over five to ten years. The window is set by compounding, not by the technology’s readiness.

What happens to a bank that doesn’t adopt AI?

It loses its most profitable, inertia-dependent revenue first — net interest income on deposits (about 30% of retail-bank profit) and credit-card economics ($234 billion in US revenue in 2024), as AI agents optimize balances and routing. McKinsey projects overall banking profit pools could compress by as much as 10%, alongside slower erosion of customers, talent and data. The losses compound, which is why delay is expensive rather than neutral.

Is it too late for an incumbent bank to catch up?

No, but the cost of catching up rises every quarter. Because the advantage is path-dependent, the gap a bank faces when it finally moves is larger than the one it could have closed earlier. Acting inside the window is far cheaper than acting after it closes.

How can a regulated bank move fast without losing auditability?

By separating the two jobs AI does. Use AI to accelerate building and changing the lending system — with human-in-the-loop approvals and shadow-run testing — while the credit decision runs on deterministic, explainable logic, not a language model. That is the architecture that delivers speed and audit trail together: AI for speed, deterministic logic for the decision.

What is the first step for a bank that wants to move now?

Audit the base before buying more tools. Ask whether your team can change a lending rule or product the same day, whether AI gains would land on recomposable building blocks or a vendor’s fixed menu, and whether your credit decisions are reproducible and auditable. If the answers are no, fix the platform first — pilots on a frozen base will keep stalling.

Ready to see the cost of waiting in numbers?

The window is measurable, and so is what it costs to stand inside it. See what a programmable, AI-native platform changes about how fast your lending team can build, launch and adapt — without giving up the auditability your regulators require.

-rsbxq-400x250.webp)

CEO at TIMVERO

Dmitriy Wolkenstein is the CEO of TIMVERO, leading the team building timveroOS and timveroAI. He writes about why the next generation of lending will be won at the infrastructure layer — and what it takes to get there.

LinkedinLatest News

Generative AI in Banking: Where It Works and Where It Can’t

AI in Banking: A 2026 Guide to Value, Risk, and Scale

AI Hallucinations in Lending Software: How to Stop Them

AI Agent vs Credit Scoring: The Two Layers of Lending AI

The AI Banking Efficiency Gap: Why It Compounds and Who Wins

How AI Is Transforming Lending in 2026: Platforms, Automation, and What Actually Works

Fraud Prevention in Digital Lending: How AI Is Reshaping the Battle in 2025–2026

Bank Efficiency Ratio: What It Is and How to Improve It

How to Implement AI in Lending and Pass a Regulatory Audit