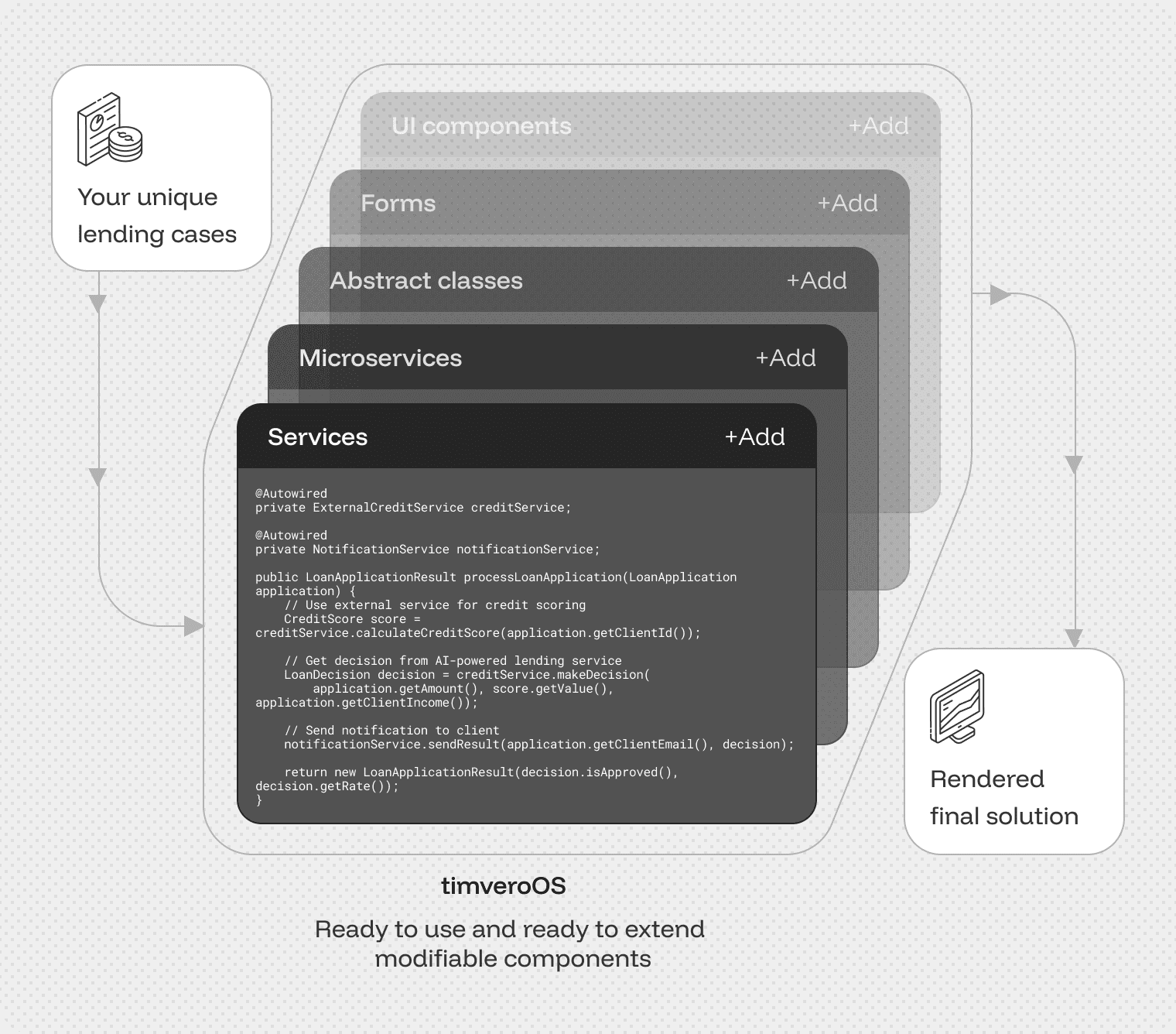

Low-Code BNPL Integrations Through Open SDK

Your stack, integrated as Building Platform blocks. The buy now pay later loan software connects natively to core banking, ERP, GL, payment rails, credit bureaus, open banking, KYC/AML providers, and merchant systems. Every integration becomes a first-class building block on the Building Platform. New vendors get composed by timveroAI in days through the Open SDK. No marketplace dependency, no per-call surcharges.

-

Core Banking and GL

Native GL posting from the Building Platform into core systems. No middleware layer, no separate reconciliation queue.

-

Payment Rails: ACH, SEPA, Card, Digital Wallets

Settlement, repayment, and refund flows composed for consumer, B2B, and embedded BNPL funding paths.

-

Credit Bureaus and Open Banking

Soft and hard pulls and permitted open banking use cases. Whether your bureau is Equifax, Experian, or TransUnion, composed into your scoring policies, not bolted on.

-

ERP and Order Management

Settlements, repayments, and overdue events sync to ERP and order systems through open API connectors configured in the admin panel.

-

SFA and DMS for B2B BNPL

Sales-force automation and distributor management systems integrate as building blocks for B2B trade BNPL exposure control.

-

KYC/AML and Identity Providers

Identity verification, device intelligence, and synthetic-ID detection feed the decisioning engine. New vendors compose in days through the Open SDK.