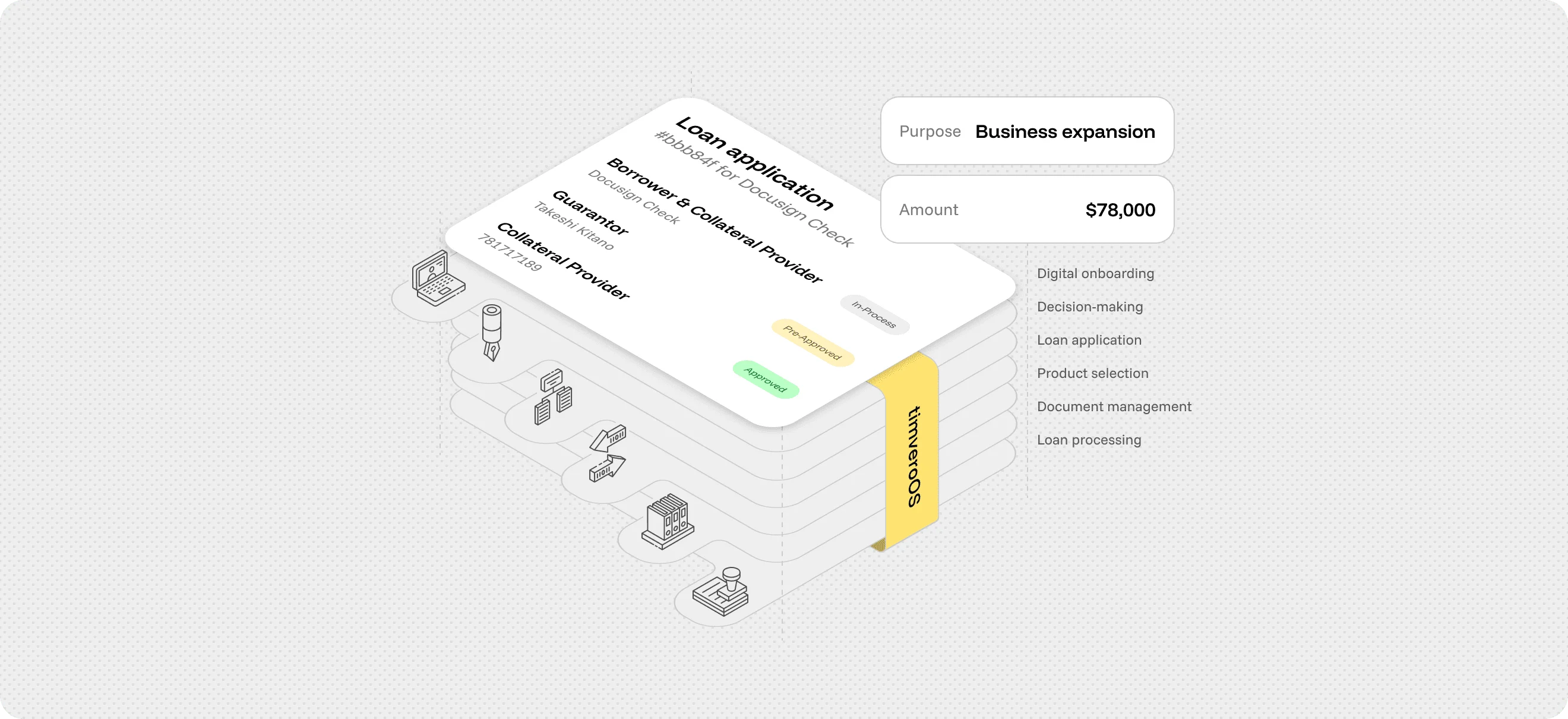

Loan Origination Software, Engineered on the timveroOS Building Platform

timveroAI helps you configure and launch new loan origination products in days.

timveroOS powers production loan origination for banks, fintechs, and credit unions across 13+ regulated markets. Deploy on your own cloud or on-premises, go live in 3–6 weeks via timveroAI.

Govern every origination rule, KYC, affordability, underwriting, offers, overrides, as immutable, auditable code your team owns.

- 100x FTE efficiency gains

- 5.0 ★ average customer rating across verified reviews

- 13+ countries served globally

- 20+ lending products live

Trusted by banks, fintechs, and credit unions across 13+ regulated markets

Loan Origination Software: What It Is and Why a Building Platform

Loan origination software (LOS) manages every stage of issuing a loan: application intake, KYC, credit decisioning, offer generation, approval, and disbursement. timveroOS delivers loan origination as a Building Platform, configurable building blocks you own, deploy on your own infrastructure, and extend in code.

-

Not a Packaged SaaS Loan Origination Platform

SaaS LOS gets lenders live quickly but locks credit policy, KYC depth, and offer logic into vendor-configurable patterns. Your data lives in the vendor’s tenant; data-residency requirements force trade-offs.

-

Not a Custom-Built Loan Origination System

Custom development inverts the problem: full ownership, full control, and 12–18 months of engineering before the first loan funds. The 6–10-engineer bench becomes a permanent line item.

-

A Third Path Between Them

The Building Platform ships 80% of the origination infrastructure already in place (application objects, entity-centric data model, KYC connectors, scoring engine, offer matrices, document generation, payment rails) and exposes the remaining 20% to your team in code.

SaaS, Custom Build, or a Building Platform?

Two architectural choices dominate the market. The Building Platform is the third path, SaaS speed with custom-build control, without trading one for the other.

SaaS Loan Origination

Pros

- Fast initial go-live (2–4 months)

- Lower upfront cost

- Prebuilt origination workflows

Cons

- Configuration capped by vendor schema

- Vendor-controlled roadmap and releases

- Data lives in vendor’s multi-tenant tenant

- Per-seat or per-loan pricing escalates TCO

Building Platform

timveroOS

Features

- Live in 3–6 weeks via timveroAI

- Code-level customization via SDK

- Your cloud or on-premises deployment

- Policies-as-code for KYC, affordability, offers

- Predictable TCO, tiered by portfolio size

- You control the roadmap, no vendor tickets

Custom Loan Origination

Pros

- Full control of code and UX

- Tailored integrations and data model

- No vendor lock-in

Cons

- 9–18 months to first production loan

- Permanent build and maintenance cost

- 6–10 lending engineers as standing line item

- Talent concentration risk grows with codebase

SaaS Loan Origination

Pros

- Fast initial go-live (2–4 months)

- Lower upfront cost

- Prebuilt origination workflows

Cons

- Configuration capped by vendor schema

- Vendor-controlled roadmap and releases

- Data lives in vendor’s multi-tenant tenant

- Per-seat or per-loan pricing escalates TCO

timveroOS

Features

- Live in 3–6 weeks via timveroAI

- Code-level customization via SDK

- Your cloud or on-premises deployment

- Policies-as-code for KYC, affordability, offers

- Predictable TCO, tiered by portfolio size

- You control the roadmap, no vendor tickets

Custom Loan Origination

Pros

- Full control of code and UX

- Tailored integrations and data model

- No vendor lock-in

Cons

- 9–18 months to first production loan

- Permanent build and maintenance cost

- 6–10 lending engineers as standing line item

- Talent concentration risk grows with codebase

3 The Resolution

AI brings the speed. The Building Platform brings the trust.

Traditional LOS implementations spend 3–6 months translating requirements into vendor configuration. timveroAI compresses that to days by composing Building Platform atoms instead of coding from scratch, and timveroAI never makes lending decisions or replaces your engineers, underwriters, or compliance team.

- Speed

3–6 weeks from kickoff to production. timveroAI automates 70–80% of implementation work.

- Trust

Policies-as-code, immutable audit logs, your origination code in your environment.

- Together

Bespoke loan origination for regulated institutions, fast AND compliant.

timveroAI

AI Brings the Speed. The Building Platform Brings the Trust.

From requirements to a working origination system

timveroAI is a RAG-grounded implementation agent, built on Claude Code, that interprets loan product specifications, composes the relevant Building Platform atoms, KYC checks, scoring inputs, offer matrices, document templates, and assembles a production-grade origination flow on timveroOS in days rather than months.

Explore timveroAI Features-

Requirement-to-Platform Mapping

Converts plain-language loan product specifications into a configured origination flow on the Building Platform. KYC rules, affordability tests, scoring criteria, and offer logic encoded as policies, every output traceable back to its source requirement.

-

Underwriting Flow Assembly

Assembles executable underwriting workflows from your data sources, scoring inputs, and approval hierarchy. Each workflow generated as Building Platform code your engineers can review, modify, and version-control before production deployment.

-

Offer and Product Configurator

Builds rate, term, and amount matrices, override rules, and product variants from your pricing logic. Configuration generated as Building Platform atoms, no manual setup, no repetitive testing cycles, no integration debt.

-

Compliance-by-Design Blueprinting

Every origination flow ships with versioned policies, audit logs, document templates, and decision traceability. When the AI doesn’t have enough context to compose safely, it asks before generating, it never hallucinates.

- 70–80% Implementation Automation

- 10× Speedup vs Traditional

- 3–6 wks Time to Launch

- 2–4 Engineers (vs 6–8)

Acquisition & Pre-Qualification

KYC & Identity Verification

Underwriting & Credit Decisioning

Offer Configuration

Approval & Documentation

Disbursement & Onboarding to Servicing

Implement Loan Origination in Weeks, Not Months

Traditional loan origination development cycles run 3–6 months. timveroAI compresses that to 3–6 weeks by treating implementation as composition, not coding from scratch, the Building Platform ships the 80%; AI assembles the 20% specific to your product, policies, and channels.

-

Run in Your Cloud, On-Premises, or Hybrid

timveroOS deploys to your AWS, Azure, or GCP environment, or runs fully on-premises in your own data centers. No multi-tenant default. Web-based loan origination, mobile origination apps, and API-driven channels all run on the same deployment.

-

timveroAI-Composed Configuration

Origination policies, scoring rules, offer matrices, and document templates composed by timveroAI from your business requirements. Your team reviews and approves each generated atom before production. Manual configuration work that traditionally takes weeks compresses to days.

-

Reusable Templates and Migration Paths

Origination templates ship for consumer installment, SMB working capital, commercial term loans, mortgage, auto, BNPL, leasing, and factoring. Lenders migrating from SaaS LOS or custom systems run parallel validation against the new flow before cutover.

Built for Control and Scalability

Control over your loan origination platform isn’t a deployment option, it’s an architectural property of the Building Platform. Three principles separate timveroOS from packaged loan origination systems at every scale.

-

Policies-as-Code on Every Origination Event

Eligibility, affordability, pricing, override governance, and consent flows are versioned policies, not hidden vendor configuration. Every credit decision logs its inputs, the active policy version, and the resulting reason codes. Policy changes are diff-able, reviewable, and reversible.

-

Entity-Centric Data Model

Borrowers, guarantors, co-applicants, agents, collateral holders, and corporate beneficiaries are first-class entities, not custom fields stretched over a single-borrower schema. This is what makes guarantor lending, factoring, syndicated loans, BNPL, and consumer credit run on the same origination platform.

-

Compose New Origination Products Without Rewrites

A new product variant, new term structure, new collateral type, new origination channel, is composed from existing Building Platform atoms, not a rebuild. The retail origination platform you launch this quarter and the commercial flow you launch next quarter share the same engine, audit trail, and admin panel.

Driving Down Loan Origination Costs Through Automation

Cost-per-loan-originated drops when manual policy enforcement, document generation, reconciliation, and compliance checks become Building Platform automation. timveroAI handles the implementation work; the Building Platform handles the operational work.

-

Automated Underwriting and Decisioning

Configurable scoring models, affordability calculators, and bureau integrations drive automated underwriting decisioning at production volumes. Conversion stays high because automation routes human review only where it adds value.

-

Auto-Generated Document Packages

Loan documentation generates from policy-driven templates with field-level data lineage. No re-keying, no manual template edits per product variant, no version drift between origination and servicing documents.

-

Continuous Compliance Validation

Every origination event validates against the current policy version. Configuration changes propagate immediately and consistently. There is no parallel compliance review cycle to catch downstream effects.

-

Origination Operations on a Single Admin Panel

Queue management, decisioning overrides, document corrections, and manual interventions all run from one admin panel. Loan officers, underwriters, and compliance staff operate from the same source of truth, not across 4–6 disconnected vendor tools.

Audit-Ready Originations From Application to Disbursement

Every origination event logs to an immutable audit trail tied to the application object. Policy versions stay queryable six months later, audit-ready by default, not as a separate compliance pass.

-

Faster Time-to-Yes

40% lower time-to-decision through automated underwriting, configurable bureau integration, and per-applicant offer matrices.

-

Built-In Regulator Replay

Full replay of every application: KYC, bureau responses, active policy version, approver, documents, disbursement.

-

Compliance Overhead Drops

Policy-driven automation replaces manual checklists. Cost per loan originated falls correspondingly.

Why Lenders Choose timveroOS for Loan Origination

Four properties ship as defaults on the Building Platform, not as add-ons, partner integrations, or enterprise-tier upgrades. They’re what lets origination teams own their product roadmap without owning the lending infrastructure itself.

-

Own Your Code, Data, and Releases

Your engineers extend timveroOS at the architectural layer through an open SDK and component library. Configuration limits don’t determine how far your origination product can evolve; code does. No vendor ticket required to add a new applicant type, integrate a niche bureau, or model a new product structure.

-

Predictable TCO That Scales With Portfolio

Pricing is tiered by portfolio size, not per-user seat, not per-loan transaction. No surcharges when you onboard new loan officers, no per-loan fees when origination volume expands, no roadmap-locked upgrades to access features your team builds itself.

-

Entity-Centric Data Model

The same entity model that powers guarantor lending also powers factoring, syndication, BNPL, and consumer credit origination. One platform, one schema, one audit trail across the entire lending product portfolio.

-

AI That Asks Before Assuming

timveroAI is RAG-grounded on the actual Building Platform source code and atom library, no invented APIs, no hallucinated imports. When the AI doesn’t have enough context to compose safely, it asks before generating. Every composed configuration is reviewable before production.

One Loan Origination Platform for Every Institution

Banks, fintechs, and credit unions face fundamentally different pressures: compliance depth for banks, product velocity for fintechs, operational efficiency for credit unions. timveroOS adapts at the segment level without forcing one model on all three.

-

Banks

The Building Platform deploys in the bank’s own environment with policies-as-code enforced at every decisioning step. Basel III, IFRS 9, Reg Z, and local rules encoded as versioned configuration your compliance team controls, not concealed in vendor settings.

Explore Solution for Banks -

Fintechs

The Building Platform gives you architectural freedom of a custom build with 3–6 week implementation via timveroAI. Launch new origination products in weeks, extend the platform as your roadmap evolves, no SaaS vendor approval cycle in the loop.

Explore Solution for Fintechs -

Credit Unions

The Building Platform’s admin panel runs day-to-day origination operations; timveroAI handles implementation. Pricing is tiered by portfolio size, not per user, not per loan, and member data stays on credit union infrastructure.

Explore Solution for Credit Unions

Built for Every Lending Vertical

Consumer Lending

Explore Consumer →Real Lenders. Real Results.

Three lending teams, a European fintech, a litigation finance company, and a regulated bank, built production origination stacks on the Building Platform. Each ended with the same answer: an origination system they own, deployed on their own infrastructure, in weeks rather than months.

98% Origination Automation Across Six Countries

7 mo Implementation From Kickoff to Production

Finom, Multi-Country SME Origination, 98% Automated

timveroOS gave us a single platform we could extend per country without a separate engineering project for each market.

Read the Full Finom Case StudyMore Stories

- 8× Faster Origination vs Previous Platform

AMIO Bank

AMIO needed an origination flow with guarantor-backed lending after three previous vendors couldn’t support the structure. The Building Platform’s entity-centric data model supports guarantors, co-applicants, and collateral holders natively. AMIO went live in six months with 95% automation.

Read AMIO’s Story - 8 wks Origination MVP at ~10% of Prior TCO

Cartiga

Cartiga ($1.6B+ deployed in US litigation finance) migrated from a CRM-based lending platform that couldn’t express bespoke multi-party origination logic. They shipped their origination MVP in 8 weeks at roughly 10% of the prior platform’s TCO, extended in code by Cartiga’s own engineers.

Read Cartiga’s Story

Frequently Asked Questions About Loan Origination Software

Talk to Sales-

What is loan origination software?

Loan origination software (LOS), also called a loan origination system, manages the full lifecycle of issuing a loan: application intake, KYC and identity verification, underwriting and credit decisioning, offer generation, approval, document execution, and disbursement. timveroOS delivers loan origination as a Building Platform, every stage is a configurable, auditable building block you own, deploy on your own infrastructure, and extend in code.

-

How is timveroOS different from a SaaS loan origination system?

SaaS loan origination platforms host your data in the vendor’s tenant, limit configuration to what the vendor exposes, and tie your origination roadmap to the vendor’s release schedule. timveroOS is a Building Platform, deployed on your infrastructure, governed by policies-as-code your team controls, and extendable at the architectural level through an open SDK. No vendor ticket required to add a new applicant type, bureau, or product structure.

-

How quickly can we go live with loan origination on timveroOS?

Typically 3–6 weeks from kickoff to production. timveroAI, our RAG-grounded implementation agent, automates the mapping of business requirements to Building Platform configuration, reducing implementation work by 70–80% compared to traditional loan origination software development cycles that take 3–6 months for the same scope.

-

Does timveroOS support regulated loan origination markets?

Yes. The Building Platform runs loan origination in 13+ regulated markets, including the US (CFPB, Reg Z), UK (FCA, Consumer Duty), Canada (OSFI), the Netherlands (DNB), and Spain (Bank of Spain, EBA). Regulatory requirements are encoded as policies-as-code, not hardcoded into vendor logic.

-

Can we use timveroOS for both consumer and commercial loan origination?

Yes. timveroOS covers consumer, SMB, commercial, and specialty loan origination on the same Building Platform. The entity-centric data model supports borrowers, guarantors, co-applicants, agents, and collateral holders out of the box, so you configure the origination flow per product type without forking the platform.

-

What happens to our data on timveroOS?

Your loan origination data stays on your own infrastructure. timveroOS deploys on-premises or in your private cloud, no multi-tenancy, no data residency trade-offs, no vendor egress charges. This is a core Building Platform design principle, not an optional add-on for enterprise tiers.

-

How much does loan origination software cost on timveroOS?

timveroOS pricing is tiered by portfolio size, not per-user seat or per-loan. You pay for continuous access to the Building Platform, timveroAI implementation capacity, and platform updates; configurations remain your IP. Cost scales predictably with portfolio growth, and specific tiers are sized per engagement during the demo.

-

What should we look for when comparing loan origination software vendors?

Six criteria separate platforms that scale from those that become bottlenecks: architectural extensibility (code-level access versus configuration ceilings), data residency, compliance configurability, implementation velocity, pricing transparency, and entity model depth. timveroOS is built as a Building Platform precisely along these dimensions.

-

Can timveroOS replace our existing loan origination system?

Yes. Lenders migrate from SaaS LOS platforms and legacy in-house systems onto timveroOS regularly. The Building Platform supports data migration from common loan origination system schemas, with parallel-run validation before cutover. Implementation typically completes in 3–6 weeks with timveroAI handling configuration work.

-

How does timveroAI handle loan origination compliance?

timveroAI composes the Building Platform; it does not make lending decisions. Every origination flow it assembles includes versioned policies, immutable audit logs, document templates, and decision traceability. Compliance is a property of every Building Platform block, not a separate review pass. Your compliance team retains full review authority over generated configurations before production deployment.

-

Can timveroOS run as a cloud-based or on-premises loan origination platform?

Both. The Building Platform deploys to AWS, Azure, GCP, or your own data center, full on-premises, private cloud, or hybrid topologies. Web-based loan origination workflows, mobile origination apps, and API-driven integrations all run on the same timveroOS deployment.

-

Does timveroOS support mobile loan origination workflows?

Yes. The Building Platform exposes origination through native mobile applications, responsive web channels, and API integrations for embedded experiences. The same application object, policy engine, and audit trail serve all channels, no separate "mobile LOS" to integrate, configure, or maintain alongside the core platform.

15 What’s New

View all Latest Insights on Loan Origination

Ready to Own Your Loan Origination Infrastructure?

Banks, fintechs, and credit unions managing $5.5B+ in loans built their origination systems on the Building Platform. See how timveroOS fits your product, your infrastructure, and your timeline, in a working demo, not a slide deck.