Installment Loan & Servicing Software, on a Building Platform

timveroOS runs pre-qualification, decisioning, disbursement, and servicing as building blocks in your own environment. Affordability, APR and term waterfalls, hardship flows, and collections logic live as policies-as-code.

Banks, fintechs, and credit unions running consumer installments at scale get explainable decisions, precise amortization, low-touch servicing, and a system they own at the code level. timveroAI compresses implementation from months to weeks.

Request a Custom Demo

Tell us the installment product you want to see: personal loan, debt consolidation, refinance, small-dollar, or your own affordability and APR waterfall. We tailor the demo bench to your exact case.

Request a DemoYour Product. Our Bench.

- 100x FTE efficiency gains

- 13+ countries served globally

- 5.0 ★ verified customer rating

- 2-6 wks from signing to first disbursement

Trusted by banks, fintechs, and credit unions running consumer installments across 13+ regulated markets

Where Standard Installment Platforms Break

Installment lending looks simple on a deck: same loan, same schedule, same servicing. In production it stops being simple. Affordability rules diverge between products, APR and term waterfalls need versioning, and hardship and collections have a dozen edge cases. Banks, fintechs, and credit unions running consumer installments hit the same architectural ceiling.

-

Affordability and APR Rules Trapped in Vendor Config

Standard installment LMS lets you tune a handful of parameters. The moment your DTI rule needs cash-flow surplus from open banking, or your APR waterfall depends on a behavioral score, you wait for vendor support. Tier 3 and Tier 4 banks regulated by CFPB, FCA, OSFI, DNB, or ECB cannot accept "your compliance is in our config" as an answer.

-

Per-Loan and Per-User Pricing Breaks Unit Economics

SaaS installment platforms price per loan, per seat, or per active borrower. At 50,000 borrowers, that surcharge is a line item that grows with the portfolio. Fintech lenders who outgrew their first platform want portfolio-tiered pricing, not a vendor tax on every disbursement.

-

Servicing Operations Bolted On, Not Native

Billing, autopay, reminders, hardship, promises-to-pay, charge-offs, bureau reporting. In stitched stacks, each lives in a different module with its own admin panel and its own data model. A credit union with five operations staff serving 50,000 members cannot run six dashboards to close one delinquent loan.

-

AI Decisioning Hidden Behind a Vendor Black Box

Risk and compliance teams need to explain every default-risk model output to a regulator and an applicant. SaaS platforms surface AI scores without the underlying logic. The platform vendor cannot show you what the model weighted. You cannot show your regulator. The applicant gets a reason code with no story behind it.

End-to-End Installment Lifecycle on a Building Platform

From first click to final payment, the installment lifecycle runs as connected building blocks on timveroOS. Pre-qualification, decisioning, disbursement, and servicing share one data model, one policy layer, and one audit log. Branch, web, or mobile, the same logic applies.

Request a Demo-

Smarter Acquisition and Instant Pre-Qualification

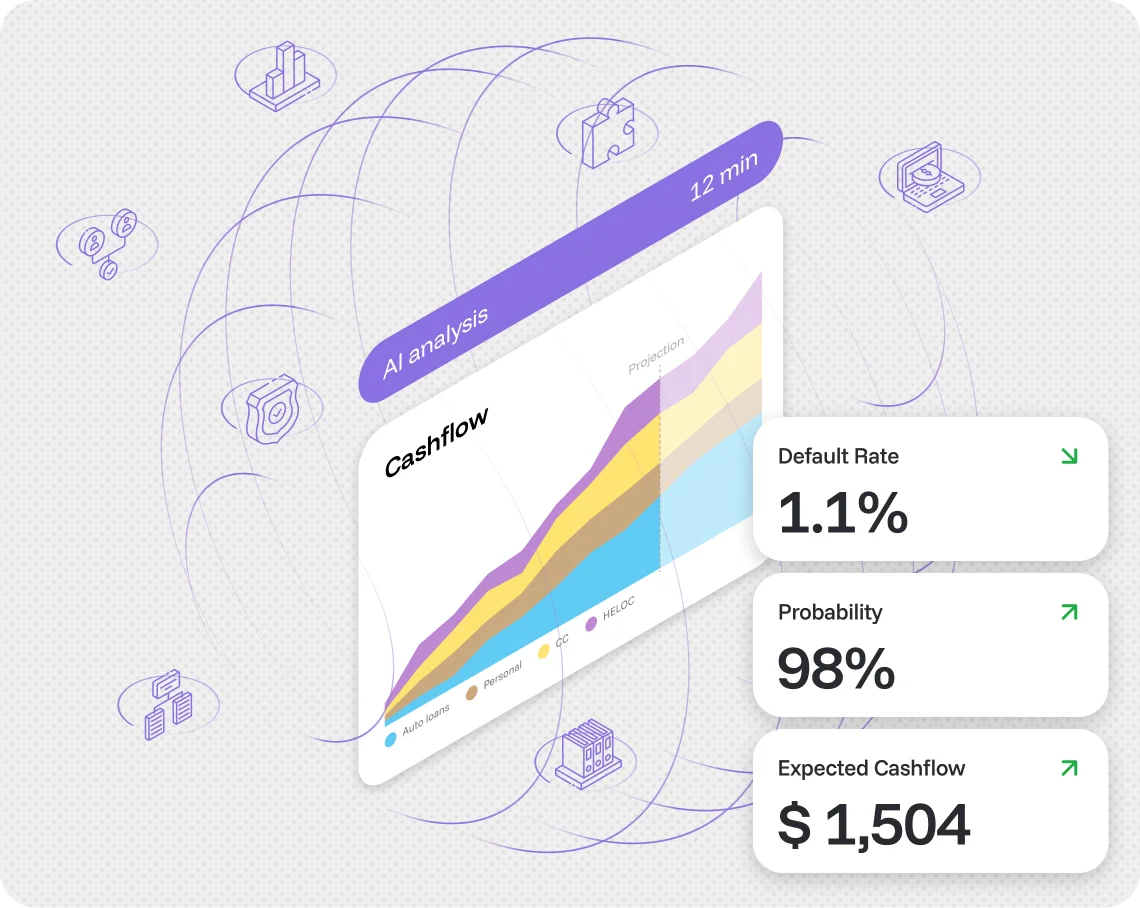

Streamlined acquisition across branch, web, and mobile. Leads are captured once and routed through built-in KYC/AML, device, and open-banking checks. Soft-pull bureau data and affordability rules generate instant pre-qual ranges with explainable reason codes. Identity and income are verified automatically. Exceptions flow through governed overrides. Every artifact and decision is versioned and audit-logged, creating a compliant data trail from the start. Lower drop-off, faster onboarding, applicant trust earned in the first interaction.

-

Explainable Risk Decisions You Can Trust

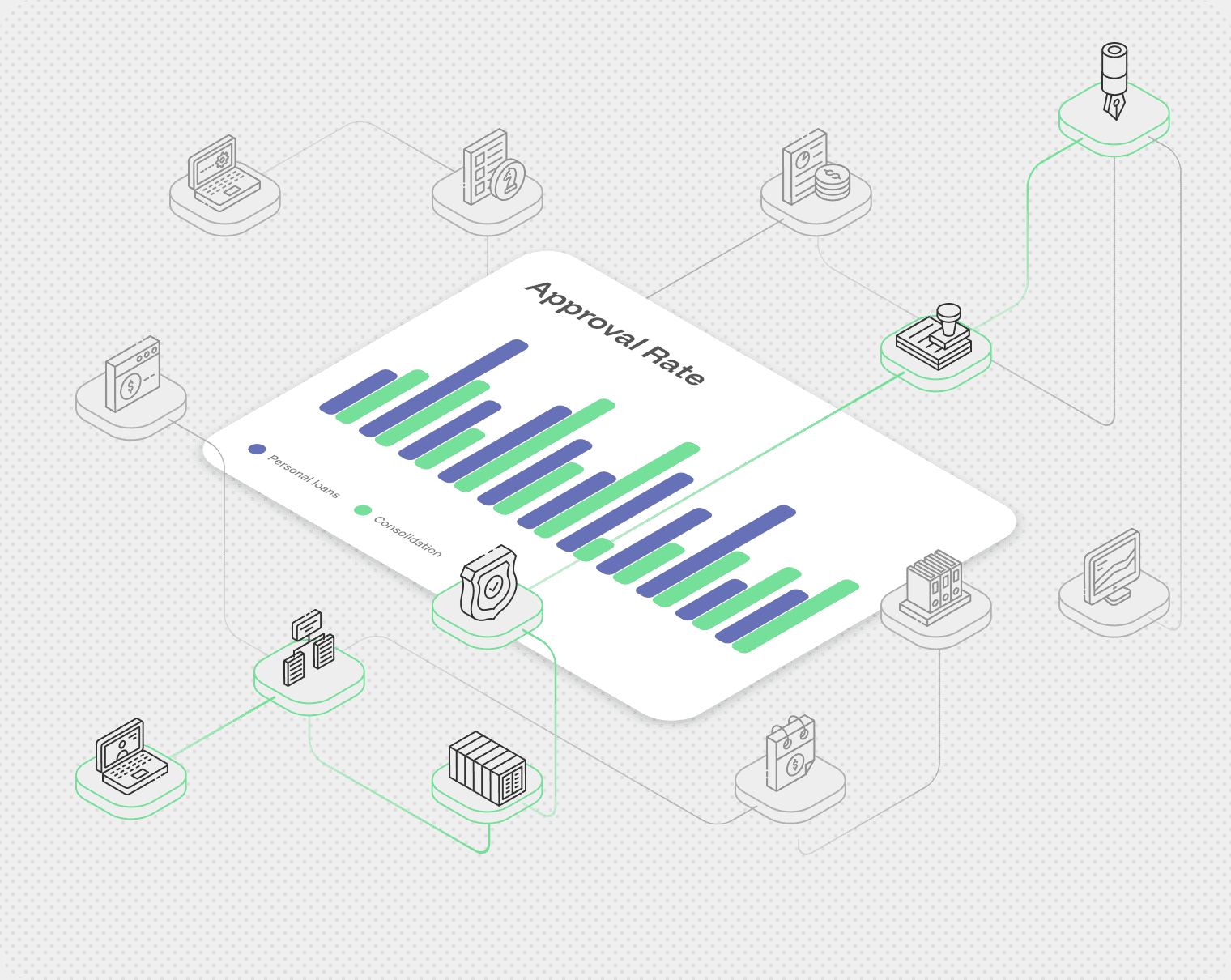

timveroOS unifies bureau data with open-banking insights like income stability, obligations, and cash-flow surplus. Affordability, DTI, and APR and term waterfalls are defined as policies-as-code, producing decisions that are both explainable and auditable. Secured, unsecured, and co-applicant structures are supported natively. Manual overrides route under governance. Every decision, model, and policy version is logged. Faster approvals for qualified borrowers, controlled losses through governed thresholds, full explainability for applicants, risk teams, and committees alike.

-

Instant Offers, E-Sign, and Payout in One Flow

The installment origination flow assembles offers with APR, term, fees, and due dates, autopay options already embedded. Disclosures generate automatically. Applicants complete e-sign in the same flow. Final fraud and account checks run in the background. Funds disburse via ACH, wire, or card issuance. Amortization schedules post directly to borrower portals. Every action, from GL postings to early-repayment handling, is versioned and audit-logged. Borrowers experience a simple, compliant process. Finance and legal teams keep full visibility across offers, payouts, and schedules.

-

Low-Touch Servicing With Built-In Hardship Flows

timveroOS automates billing, autopay, and reminders. Borrowers get clear portals for balances, payoff quotes, and extensions. Payment holidays, hardship, and forbearance are handled natively. Pre-delinquency alerts trigger before defaults. Promises-to-pay, charge-offs, and recoveries are governed and logged. Installment payment collection management runs as a building block, not as a stitched workflow. Bank file reconciliation and bureau reporting automate. Portfolio dashboards surface early-warning signals for risk and finance. Lower operating cost, higher cure rates, greater resilience in collections.

From Applicants to Products on a Unified Architecture

Every object in installment lending is modeled natively on the Building Platform. Applicants, households, co-applicants. Accounts and devices. Bureau, open-banking, and fraud data. Document sets and configurable flows for pre-qual, underwriting, offers, e-sign, and servicing. Together, these building blocks assemble personal loan, debt-consolidation, refinance, and small-dollar installment products, all extensible in code and integrated through the SDK.

Launch Installment Products in Weeks With timveroAI

AI brings the speed. The Building Platform brings the trust.

timveroAI is the AI acceleration layer for the Building Platform. Not a decisioning agent, not a no-code builder. A controlled, RAG-grounded implementation agent built on Claude Code, anchored on the Building Platform source code, atom library, and past installment implementations. For an installment program, timveroAI compresses 3 to 6 months of implementation into 2 to 6 weeks, handling 70 to 80 percent of configuration. Your developers review and extend the rest through the SDK.

Learn About timveroAI-

Requirements Gathering

Natural-language dialog with your product and risk teams about credit policy, APR waterfalls, servicing rules, and the integration stack. timveroAI asks clarifying questions like a senior product owner instead of guessing.

-

Architecture Checkpoint

A plan with atoms (AccrualEngine schedules, state machines, services, integrations) and flows, surfaced for your team to approve before any generation begins.

-

Composition From Building Blocks

Code generation uses actual Building Platform components and prior installment deployment patterns. No invented APIs, no hallucinated imports. Production-grade code on trusted infrastructure, not a prototype.

-

Shadow-Run and Human-in-the-Loop

Shadow-run mode validates before production. Human approval gates remain throughout. Multi-language requirements supported. Your engineering team reviews and extends through the SDK.

Explainable AI for Risk, Fraud, and Collections Decisioning

Where timveroAI accelerates implementation, the XAI scoring engine handles runtime decisioning. Two different capabilities of the Building Platform, kept distinct on purpose. Models train in your environment on your data. Decisions stream through the same policy layer as the rest of your installment loan management platform. Every model output, every policy version, every override is logged.

-

Affordability and Default-Risk Scoring

Transparent feature weights ready for risk committee and regulator review. Predicts default and early-payment risk, estimates affordability from bank-transaction data.

-

Fraud Detection Across Synthetic and First-Party Cases

Scored at application and at servicing events. Catches identity manipulation, synthetic profiles, and behavioral anomalies that pure bureau data misses.

-

Offer Optimizer for APR, Term, and Amount

Parameterized to your portfolio risk appetite. Yields explainable scores your risk committee can defend, your regulator can audit, and your applicants can understand through readable reason codes.

-

Pre-Delinquency Alerts and Cure-Probability Scoring

Early intervention before charge-off. Surfaces the borrowers most likely to respond to outreach, hardship terms, or restructuring before the account hits default.

4 Reasons Installment Lenders Choose timveroOS

-

Affordability You Can Explain and Adjust

Author affordability, DTI, and APR and term waterfalls once, in code. Governed overrides and versioned rules make every decision explainable and auditable. timveroOS removes custom plumbing, so you adapt pricing or credit policy without waiting for vendor releases.

-

Precise Schedules and Clean Accounting

The installment loan management system generates accurate amortization schedules automatically. Fees and interest post to the GL. Refunds and chargebacks automate. Built-in reconciliation supports audit. Schedules stay consistent across servicing, finance, and reporting.

-

Omnichannel Journeys on One Building Platform

Branch, web, and mobile journeys share the same widgets and flows. Borrowers get portals with reminders, payoff quotes, and hardship options. Autopay and exception workflows reduce manual work. One codebase, five distribution channels.

-

Launch in Weeks, Not Months

timveroAI composes the Building Platform building blocks for your specific installment product. Configurations, integrations, and policy layers assemble in 2 to 6 weeks. Your engineering team reviews and extends through the SDK. Shadow-run mode validates before production. Human-in-the-loop approval throughout.

Your Installment Stack, Integrated as Building Blocks

Cores, GL and accounting systems, payment rails, credit bureaus, KYC and AML providers, open-banking aggregators, fraud signals, communications, and CRM connect natively to timveroOS. Implemented during deployment, owned in your code. New vendors get composed by timveroAI in days via the Open SDK. No marketplace dependency, no per-call surcharges, no integration partner gatekeeping.

-

Cores and GL

Whether your core is built in-house or sourced, integration happens at the architectural level, not through marketplace permissions. GL postings, fees, and reconciliation run on your accounting system of record.

-

Payment Rails

ACH for disbursement and autopay, wire for high-value, card issuance for instant access. Bank file reconciliation automates against the same data model as servicing actions.

-

Credit Bureaus and Open Banking

Whether your bureau is Equifax, Experian, or TransUnion, consumer credit data and cash-flow data combine in the same affordability and DTI logic. Open-banking signals feed default-risk and fraud models alongside bureau pulls.

-

KYC and AML, Fraud, Communications, CRM

Identity verification, sanctions screening, synthetic-fraud detection, SMS, email, and CRM all run as first-class building blocks. Add a regional rail or niche provider through the Open SDK, or let timveroAI compose it in days.

Trusted by Installment Lenders Worldwide

Banks, fintechs, and credit unions running consumer installment products at scale. Different operating models, same architectural primitives on the Building Platform.

-

Banks (Consumer Installments)

Launch personal loans, debt consolidation, and refinancing on a Building Platform built for regulated lending. Affordability, APR, and pricing as code. Explainable underwriting. Precise schedules. Connect to your core, bureaus, and open-banking feeds. Generate audit-ready reporting for risk and finance teams.

-

Neobanks and Consumer Fintech Lenders

Deliver instant pre-qualification, device and fraud checks, and low-touch servicing while keeping code, data, and release control. timveroOS gives consumer fintech lenders a compliant Building Platform foundation to scale installment products on portfolio-tiered pricing. Unit economics stay intact at scale.

-

Credit Unions (Member Installments)

Launch member installment products on the Building Platform admin panel. timveroAI handles the heavy configuration. Your IT team focuses on credit-union-specific extensions through the SDK. Member-focused affordability logic. Portfolio-tiered pricing scales with assets, not with logins. On-premise or private-cloud deployment keeps member data in your environment.

Installment Lenders Deploying timveroOS

- 80% ready-to-use lending infrastructure supplied

Finom

timveroOS partners with a fast-growing European fintech to launch a multi-country proactive credit product for SMEs delivering full automation, regulatory compliance, and rapid market rollout at a fraction of the cost and time of traditional banking systems.

Read now - 90% cost reduction compare to the previous solution

Cartiga

timveroOS enables a US-based litigation finance company to launch complex working capital products for law firms while achieving full automation, faster time to market, and significantly lowering costs compared to their previous enterprise platform.

Read now - 100% bespoke origination requirements coverage

AMIO Bank

timveroOS enabled a leading Armenian bank to transform a complex lending concept with guarantor support into a fully automated, production-ready solution. The platform ensured full compliance and rapid deployment - bringing the new product to market in just six months.

Read now

SaaS vs Building Platform vs Custom Development

SaaS installment platforms launch quickly but trap your credit model in vendor config. Custom builds give you full control at the cost of 9 to 18 months and a long maintenance tail. The Building Platform delivers SaaS speed with custom-level control: faster deployment, predictable TCO, full governance. Policies-as-code for pricing, fees, hardship, and collections, running in your own environment.

SaaS solutions

Pros

- Fast initial go-live

- Lower upfront cost

- Prebuilt workflows

Cons

- Limited policy and UX flexibility

- Vendor roadmap and data custody constraints

- Volume and per-seat fees escalate TCO

timveroOS

Features

- Modules and SDK in your environment

- Policies-as-code: posting, fees, hardship, collections

- Open APIs to core, GL, rails, bureaus

- Immutable log: explainable changes and reversals

- Predictable portfolio-tiered pricing

- From signing to first disbursement in 2 to 6 weeks with timveroAI

Custom Development

Pros

- Full control of code and UX

- Tailored integrations and data model

- No vendor lock-in

Cons

- 9 to 18 month delivery risk

- High build and maintenance cost

- Talent and knowledge concentration risk

SaaS solutions

Pros

- Fast initial go-live

- Lower upfront cost

- Prebuilt workflows

Cons

- Limited policy and UX flexibility

- Vendor roadmap and data custody constraints

- Volume and per-seat fees escalate TCO

timveroOS

Features

- Modules and SDK in your environment

- Policies-as-code: posting, fees, hardship, collections

- Open APIs to core, GL, rails, bureaus

- Immutable log: explainable changes and reversals

- Predictable portfolio-tiered pricing

- From signing to first disbursement in 2 to 6 weeks with timveroAI

Custom Development

Pros

- Full control of code and UX

- Tailored integrations and data model

- No vendor lock-in

Cons

- 9 to 18 month delivery risk

- High build and maintenance cost

- Talent and knowledge concentration risk

Frequently Asked Questions

Common questions from product, risk, and engineering leaders evaluating installment loan software on a Building Platform.

Talk to Our Team-

What is installment loan software?

Installment loan software is the system that originates, decisions, disburses, and services fixed-term consumer loans with scheduled repayments. Standard categories include personal loans, debt consolidation, refinancing, point-of-sale installments, and small-dollar credit. timveroOS delivers installment loan software as a lending solution on a Building Platform, with pre-built building blocks for the full lifecycle, policies-as-code for every credit and servicing rule, deployed in your own environment.

-

How does timveroOS differ from a SaaS installment loan management software platform?

SaaS installment loan management software locks your credit model into vendor schema and prices per loan or per seat. timveroOS is a lending solution on a Building Platform. You own the code, deploy in your own environment, and configure policies-as-code without vendor permissions. timveroAI composes the building blocks for your specific installment product in 2 to 6 weeks. Pricing is portfolio-tiered, not per-loan or per-user.

-

Can timveroOS deploy on-premise or in our cloud?

Yes. The Building Platform deploys in your own environment: public cloud (AWS, Azure, GCP), hybrid, or on-premise. Data sovereignty, code ownership, and platform version remain in your control. Compliance-sensitive operations such as Tier 3 and Tier 4 banks and regulated credit unions can deploy on private infrastructure. timveroAI runs in the same controlled environment, anchored on your codebase.

-

What amortization schedules and repayment options does timveroOS support?

timveroOS supports any amortization schedule configurable as a building block: equal-installment, declining-balance, balloon, interest-only periods, grace periods, holiday months, biweekly, monthly. Any daycount method (Act/360, Act/365, 30/360). Any payment calendar. APR and term waterfalls, fees, and early-repayment handling are policies-as-code on the Building Platform. New schedule variants take days, not vendor roadmap quarters.

-

How does installment loan servicing software work on timveroOS?

Installment loan servicing software on timveroOS handles billing, autopay, reminders, balances, payoff quotes, hardship flows, promises-to-pay, charge-offs, and bureau reporting as connected building blocks. Pre-delinquency alerts trigger before defaults. Bank file reconciliation and bureau reporting automate. Portfolio dashboards surface early-warning signals. Installment payment collection management runs in the same governed policy layer as origination.

-

How long does it take to launch a new installment product on timveroOS?

Two to six weeks for most installment products. timveroAI composes the Building Platform building blocks for your specific product: affordability rules, APR waterfalls, repayment schedules, integration stack. Your engineering team reviews and extends through the SDK. Shadow-run mode validates before production. Human-in-the-loop approval gates remain throughout. Faster than custom development (9 to 18 months), more flexible than SaaS (vendor roadmap).

-

Does timveroOS support small-dollar and short-term installment products?

Yes. The Building Platform handles small-dollar installment products, short-term installments, payday-to-installment programs, and consumer installment products of any term and amount. Affordability and APR rules are configurable per product. Compliance constraints (state APR caps, ATR/QM, military lending) live as policies-as-code. The same building blocks scale from $200 four-week products to $50,000 60-month consolidation loans.

-

What is a Building Platform in installment lending?

A Building Platform is the third path between SaaS and custom development: pre-built building blocks for the full installment lifecycle (origination, decisioning, servicing, collections), combined with an SDK for architectural-level extension. You own the code. You deploy in your own environment. You configure policies-as-code without waiting for vendor releases. timveroAI accelerates configuration from months to weeks. Faster than custom, more flexible than SaaS.

Related Lending Solutions

Launch Your Installment Product on timveroOS

$5.5B+ managed across 13+ countries. From signing to first disbursement in 2 to 6 weeks with timveroAI. Built on a Building Platform that gives you code-level control over affordability, APR, schedules, and servicing.

Request a Demo Explore the Architecture