Commercial Lending

- B2B Installment Loan

- Asset-Based Lending

- Invoice Factoring

- Leasing

- Construction Loan

- Private Credit

- Merchant Cash Advance

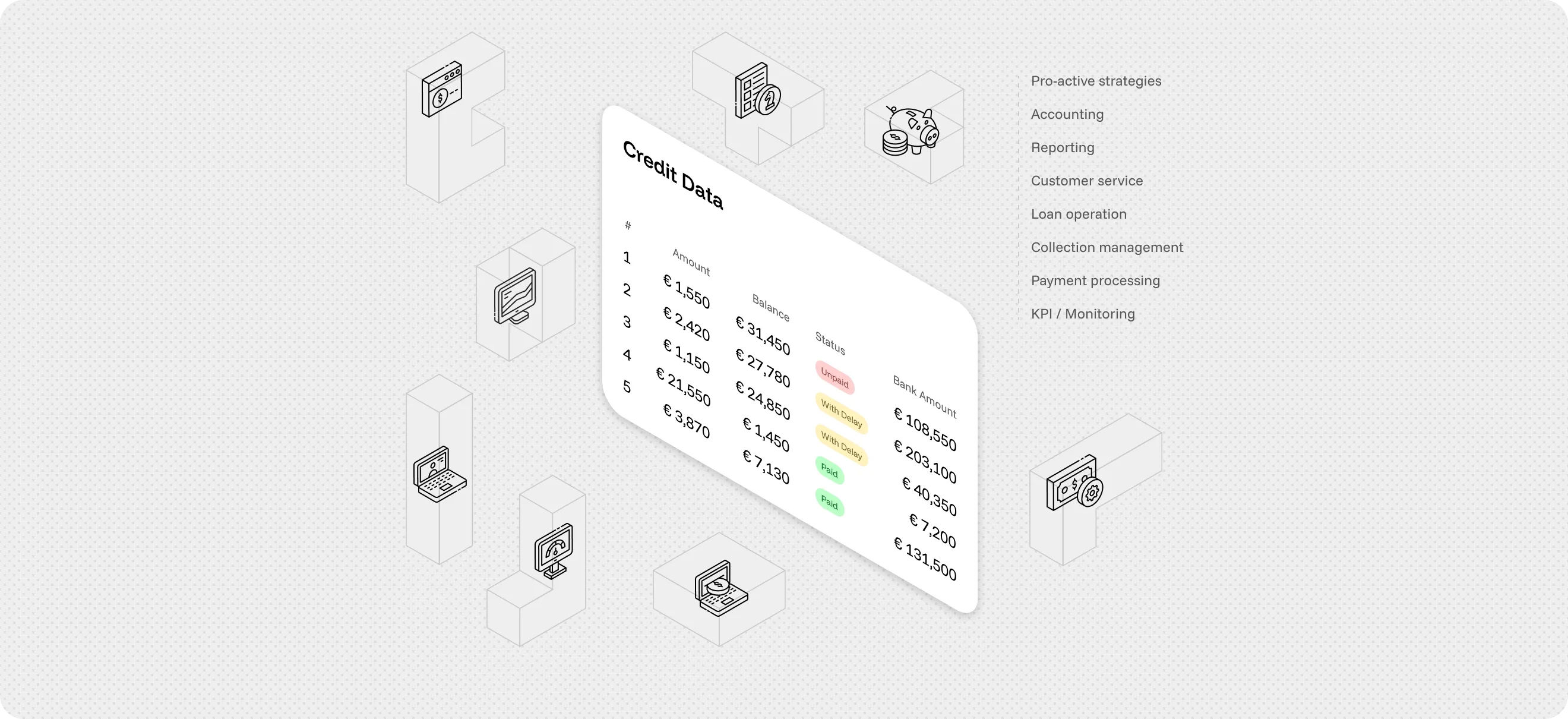

End-to-end servicing, posting, hardship, and recoveries, governed by policies-as-code. Cloud or on-premises.

Loan software for lenders: banks, fintechs, and credit unions running enterprise and small business portfolios.

Trusted by banks, fintechs, and credit unions across 13 countries

Loan management software automates the post-origination lifecycle: billing, payments, posting, reconciliation, hardship, collections, reporting. The timveroOS platform delivers this as policies-as-code on infrastructure you own, deployed in 3–6 weeks across cloud or on-premises, with full audit trails on every event.

Customization isn’t capped at vendor roadmap. Every workflow, posting rule, and policy composes in your own code.

Building blocks already in place: accrual engine, state machines, GL posting, integrations. 18 months of work delivered.

Your team composes the loan product on top, in code you already own. Java and Spring Boot, your developers, your environment.

SaaS systems launch quickly but cap customization. Custom builds give control at 12–18 months of timeline. The Building Platform delivers the middle: your environment, your code, fast deployment.

Together, timveroOS and timveroAI deliver bespoke lending systems for regulated institutions, without forcing a choice between fast and compliant.

2–6 weeks from kickoff. timveroAI automates 70–80% of work.

Policies-as-code, immutable log, your code in your environment.

Bespoke lending systems for regulated institutions: fast AND compliant.

The platform is composed of building blocks you assemble into your operating model. Start with the modules you need today, extend with SDK and timveroAI as your product evolves.

Loan origination

Application intake, decisioning, doc generation, approvals. Multichannel digital + branch, policy-driven underwriting.

Loan servicing

Schedule management, accrual, payments, statements. Reason-coded entries, controlled reversal and refund workflows.

Advanced loan analytics

XAI scoring and portfolio analytics: up to 12× faster decisioning, +20% profit per loan. Explainable, regulator-ready.

timveroAI implementation

RAG-grounded AI composes timveroOS building blocks from your requirements. 70–80% automation; 2–6 weeks to launch.

From operating model to a governed loan management system

timveroAI is the AI acceleration layer for timveroOS: a controlled, RAG-grounded implementation agent built on Claude Code. It interprets requirements in plain language, then composes timveroOS building blocks into production-grade configuration. Operates within the Building Platform, asks before assuming.

Explore timveroAI Features

Maps account structures, product hierarchies, and event triggers into executable policy code, framework-native and version-controlled.

Assembles repayment, billing, adjustment, and hardship workflows from plain-English business rules. Ready for compliance review day one.

Configures posting hierarchies, refund flows, dispute handling, and bank-file reconciliation logic with end-to-end traceability.

Replicates governed setups across markets and entities with version control. Each rollout saves 70–80% of implementation work.

Three architectural commitments distinguish a Building Platform from both SaaS and custom builds.

Deploy in your cloud (AWS, Azure, GCP, private) or on-premises. Full control over code, data, and release schedule, meeting UK, EU, and other regulated jurisdiction standards. Open SDKs and APIs to core, GL, rails, KYC/AML, bureaus.

Posting hierarchies, fee tables, hardship rules, collections logic: all as version-controlled policy code. Each action records inputs, calculations, approvals, reason codes in an immutable log. Single source for runtime, audit, regulator response.

Start with billing, payment ops, account maintenance, collections. Extend or replace in code. SDK, event bus, 90+ connector kits add portals, workflows, analytics without touching the core. Java/Spring Boot: code your team owns.

Policies-as-code automates routine posting, adjustments, and reconciliation end-to-end. Manual exceptions disappear; outputs standardize; breaks surface before they reach finance.

Routes payments by policy, retries failed debits intelligently, surfaces NSF risk before it cascades to collections.

Allocates partial and over-payments by versioned policy; reversals and refunds execute through controlled workflows.

Bank-file matching runs without batches; breaks expose with reason codes for finance review and resolution.

Borrower portals for payoff quotes, schedule changes, statements, and hardship requests on the same engine as ops.

Delinquency, hardship, and recoveries on one governed engine. Cure probability and case prioritization come from the Advanced Loan Analytics layer with explainable model outputs.

Behavioural, transactional, and macro indicators feed prioritization scoring from the Advanced Loan Analytics layer.

Channel sequencing, dunning rules, and contact-compliance encoded as policy, versioned and fully auditable.

Forbearance, modifications, and payment plans execute as policy-bound workflows with explicit reason codes.

Promise-to-pay through charge-off recorded in one auditable framework, regulator-ready by default.

Four structural choices competitors do not offer in combination, derived from how the timveroOS Building Platform works, not from marketing positioning.

Customizations and configurations belong to your team. Deployment runs in your environment. You choose when to adopt new Building Platform versions. No forced upgrades, no multi-tenant data commingling, no vendor lock-in.

Tiered subscription aligned with portfolio size, not per-seat, not per-loan. Scale users, branches, and product lines without surcharges. Cartiga cut platform costs 90% migrating from their previous enterprise platform.

Borrowers, guarantors, intermediaries, co-signers, beneficiaries are first-class entities. Complex commercial structures, joint applications, syndications, guarantor flows (AMIO Bank) run on the same engine as simple consumer loans.

timveroAI is RAG-grounded on actual timveroOS source code and atom library. It does not hallucinate APIs or invent patterns. When uncertain, it asks clarifying questions like a senior product owner.

Three institution types, three operating contexts. The same Building Platform underneath, composed differently for each.

Manage consumer, SME, and small business portfolios with policies-as-code, precise schedules, GL cleanliness, bureau reporting. Enterprise loan management system software for tier 1 books and a loans management system for digital-first business lending.

Lending Software for BanksScale digital servicing with embedded portals, wallet/ACH/card rails, payoff quotes, explainable posting. Build new lending products on the same engine that serves your existing book. Iterate at your product roadmap’s speed, not the vendor’s.

Lending Software for FintechsAssisted branch + digital servicing, governed hardship and forbearance, predictable TCO without per-seat fees. Data and releases under your control. Member-first UX on the same audit-ready core that serves regulated institutions.

Lending Software for Credit UnionsDeployments that show what loan management looks like when teams own the code, the deployment, and the audit trail.

timveroOS partners with a fast-growing European fintech to launch a multi-country proactive credit product for SMEs delivering full automation, regulatory compliance, and rapid market rollout at a fraction of the cost and time of traditional banking systems.

Read now

timveroOS enables a US-based litigation finance company to launch complex working capital products for law firms while achieving full automation, faster time to market, and significantly lowering costs compared to their previous enterprise platform.

Read now

timveroOS enabled a leading Armenian bank to transform a complex lending concept with guarantor support into a fully automated, production-ready solution. The platform ensured full compliance and rapid deployment - bringing the new product to market in just six months.

Read nowLoan management software automates the post-origination lifecycle of a loan: billing, payments, posting, reconciliation, hardship handling, collections, and reporting. Modern loan management software unifies servicing, accounting, and compliance on one governed engine, replacing spreadsheets, batch jobs, and disconnected vendor modules. The timveroOS loan management platform delivers this as policies-as-code on infrastructure you own, with full audit trails on every event.

SaaS loan management systems run on the vendor’s infrastructure, cap customization at what the vendor’s roadmap allows, and meter usage by user or by loan. timveroOS runs in your cloud or on-premises, gives you the source for your customizations, and prices on portfolio tier, not per seat. The Building Platform fits non-standard lending products that SaaS cannot accommodate without vendor engineering tickets.

A Building Platform contains the lending building blocks (accrual engine, participant data model, servicing state machines, GL posting logic, integrations) that custom development would otherwise require 18–24 months to write from scratch. Your team composes these blocks into your loan product using the SDK instead of writing lending primitives. You get full code ownership without paying the 12–18 month build timeline.

Both. timveroOS runs as a fully online loan management system in your cloud (AWS, Azure, GCP, or private) or as a web-based loan management system on-premises in your data centre. You retain full control over data residency, security configurations, and release schedules. This makes timveroOS suitable for regulated lenders in the UK, EU, and other jurisdictions where on-premises deployment is required, and for any institution prioritising data custody and audit defensibility over vendor convenience.

Yes. timveroOS is a Building Platform: customization is the normal operating mode, not an exception. Your team uses the SDK (Java / Spring Boot) and the configuration layer to compose loan products, workflows, integrations, and policies. With timveroAI, the typical implementation runs in 2–6 weeks, with up to 70–80% of the work automated by the AI agent and the remainder owned by 2–4 engineers on your side.

Tiered subscription aligned with portfolio size, not per-seat, not per-loan, not per-transaction. Adding users, branches, or new products does not change the price tier, so growing teams and expanding product lines do not face escalating costs. See our pricing page for the current tier breakdown. The total cost of ownership is typically a fraction of equivalent SaaS platforms over a 3–5 year horizon, as documented in the Cartiga case study.

Consumer (auto, BNPL, POS, micro, installment, retail, personal, mortgage), SME and commercial (working capital, asset-based, factoring, leasing, construction, private credit, B2B installment), and specialized products (litigation finance, embedded credit). Multi-participant entity model handles guarantors, co-signers, syndications, and intermediaries natively. See the AMIO Bank case for an example of complex guarantor-backed lending on the platform.

90+ ready connectors ship as standard timveroOS building blocks: core banking, general ledger systems, ACH and card rails, wallet providers, KYC/AML, credit bureaus (US, UK, EU), document signing, identity verification, and reporting platforms. New integrations are added through the SDK in days rather than waitlisted on a vendor marketplace. The integration layer is framework-native, same code patterns as the rest of the platform.

Every transaction, configuration change, override, and approval is logged with actor, timestamp, reason code, and policy version in an immutable log. The same source drives runtime execution, audit reporting, and regulator submissions: no spreadsheet drift, no hidden business logic. Out-of-the-box modules cover IFRS 9 and CECL provisioning, regulatory reporting templates, and explainable model outputs for analytics. Policies-as-code makes compliance reviewable line by line.

Join lenders managing $5.5bn+ on the timveroOS Building Platform. See how loan management runs when your team owns the code, the deployment, and the audit trail.