Microfinance Software for MFIs With Explainable Thin-File Scoring

timveroOS powers microfinance software for MFIs, digital lenders, and credit unions running thin-file borrowers across emerging and established markets. Onboard agents in low-bandwidth mode, score thin-file applicants with affordability-as-policy, disburse to mobile wallets, and govern PAR30/90 from one platform you deploy and own.

Launch a production-ready micro loan management product in 3 to 6 weeks on a Building Platform, not in 9 to 18 months on a custom build. timveroAI composes the configuration, your engineering team reviews and extends through the SDK.

Book a Personal Demo

See timveroOS configured for your microfinance product. Thin-file scoring, wallet rails, and agent flow, tailored to your case.

Request a DemoYour Product. Our Bench.

- 100x FTE efficiency gains

- 13+ countries served globally

- 5.0 ★ verified customer rating

- 3-6 wks from signing to first disbursement

Trusted by MFIs, digital lenders, and credit unions running thin-file portfolios across 13+ regulated markets

Where Generic Microfinance Software Breaks

MFIs and digital lenders running microloans face four operational tensions that generic SaaS and one-size-fits-all loan management platforms were never designed to resolve. Thin-file applicants, field-agent operations, microeconomics at scale, and rising regulatory expectations push standard tooling past its limits.

-

Thin-File Scoring Without Bias

Borrowers come with no bureau record, no payslip, no formal address. Scoring has to ingest alternative data (telco usage, wallet history, device signals, employment proxies) and produce decisions that pass internal credit committee review and regulator audit. Generic SaaS hands you a black-box score; MFIs need policies-as-code with transparent reason codes and governed overrides.

-

Field Agent Ops Without Leakage

Agents enroll borrowers in low-bandwidth villages and high-volume retail corridors. They handle KYC documents, biometrics, group and guarantor forms, and cash-in operations. Off-process activity, paper drift, and unreconciled cash are the biggest sources of portfolio leakage. The tooling has to enforce workflow guardrails in offline mode and reconcile on sync, not on month-end.

-

High-Volume, Low-Value Microeconomics

A typical microloan is $50 to $2,000 with 30 to 180 day tenor. Per-loan fees, per-seat SaaS pricing, and per-API-call vendor models destroy unit economics at scale. Microfinance software has to run thousands of decisions per day on portfolio-tiered pricing that does not punish you for growth.

-

Regulatory Maturity in Emerging and Established Markets

Central banks across Africa, Asia, Latin America, and Eastern Europe are tightening data privacy, capital adequacy, and AI governance rules. Lenders need transparent decision logic, audit trails, and data sovereignty options, not a vendor compliance certificate. The Building Platform surfaces every decision and policy change as versioned code.

Micro Loan Software With Zero Blind Spots From Outreach to Top-Up

From the first agent interaction to the last top-up repayment, timveroOS manages every micro lending lifecycle stage as configurable code and UI on a Building Platform. Onboarding, underwriting, disbursement, and servicing share one data model, one policy layer, and one audit log. MFIs, digital lenders, and credit unions run the same primitives, configured to their product.

Request a Demo-

Frictionless Agent-Led and Digital Onboarding

Borrowers enroll through mobile app, USSD shortcode, or field agent with offline store-and-forward sync. timveroOS supports ID verification, biometrics, OTP, language capture, and consent flows. Configure eligibility by geography, household structure, and group or guarantor rules. Wallets and cash-in agents map directly into participant data. Workflow guardrails enforce KYC stips, role-scoped approvals, and immutable audit. timveroOS plugs into your existing loan origination workflows or runs as the origination layer itself.

-

Responsible Instant Offers for Thin-File Borrowers

Alternative data ingests from telco usage, wallet transactions, device signals, employment proxies, plus open banking or bureau feeds where available. Affordability rules, exposure limits, and segmentation waterfalls live as policy code, not vendor configuration. Decisions return reason codes, governed override paths, and full version history. Individual and group lending with guarantors run on the same data model. Committees and regulators see how every approval was reached. MFIs increase approval rates responsibly, without compromising credit quality.

-

Cash-In, Cash-Out, and Clean Settlement

Disburse approved microloans to mobile wallets, bank accounts, or agent cash-out. Configure fees, grace periods, and repayment calendars: weekly, biweekly, monthly, or bullet. Transactions tokenize, refunds and chargebacks live in workflow, and wallet provider files reconcile automatically to your general ledger. Borrowers and agents see schedules and payoff balances in branded portals with multilingual reminders. Finance teams cut leakage and audit prep time; field operations stay in sync with the same data model.

-

Servicing, Collections, and Responsible Top-Ups

Billing and autopay run on schedule across wallets, bank debits, and cash agents. Hardship, extensions, and forbearance live in loan servicing automation. Pre-delinquency alerts and dunning sequences configure by policy with logged promises-to-pay. PAR30/90 dashboards feed risk monitoring. On-time borrowers qualify for governed top-ups, accelerating responsible portfolio growth. Bureau reporting, where available, automates as a building block. The micro loan management system runs one governed policy layer end to end.

A Micro Lending Data Model That Mirrors How MFIs Actually Operate

timveroOS uses an entity-centric data model purpose-built for microfinance. Borrowers, groups, guarantors, agents, devices, wallets, and documents live as first-class entities with their own state machines and audit trails. Configure onboard, underwrite, disburse, service, collect, and repeat workflows by composing the Building Platform building blocks in your own deployment environment.

Launch Microfinance Products in Weeks With timveroAI

AI brings the speed. The Building Platform brings the trust.

timveroAI is the AI acceleration layer for the Building Platform. Not a decisioning agent, not a no-code builder. A controlled, RAG-grounded implementation agent built on Claude Code, anchored on the Building Platform source code, atom library, and prior MFI deployments. For a microfinance program, timveroAI compresses 3 to 6 months of implementation into 3 to 6 weeks, handling 70 to 80 percent of configuration. Your developers review and extend the rest through the SDK.

Learn About timveroAI-

Requirements Gathering

Natural-language dialog with your product, credit, and field-ops teams in English, French, Russian, Spanish, or Arabic. timveroAI asks clarifying questions about group lending, guarantor rules, top-up eligibility, and wallet rails instead of guessing.

-

Architecture Checkpoint

A plan with atoms (participant data, scoring policies, state machines, agent workflows, wallet adapters) surfaced for your team to approve before any generation begins. Human-in-the-loop gates remain throughout.

-

Composition From Building Blocks

Code generation uses actual Building Platform components and prior microfinance deployment patterns. No invented APIs, no hallucinated imports. Production-grade code on trusted infrastructure your engineering team owns, reads, and extends.

-

Shadow-Run and Human-in-the-Loop

Shadow-run mode validates configurations before production. Approval gates remain at every checkpoint. When timveroAI does not know something, it asks. It does not invent.

Explainable AI for Thin-File Decisioning, Fraud, and Collections

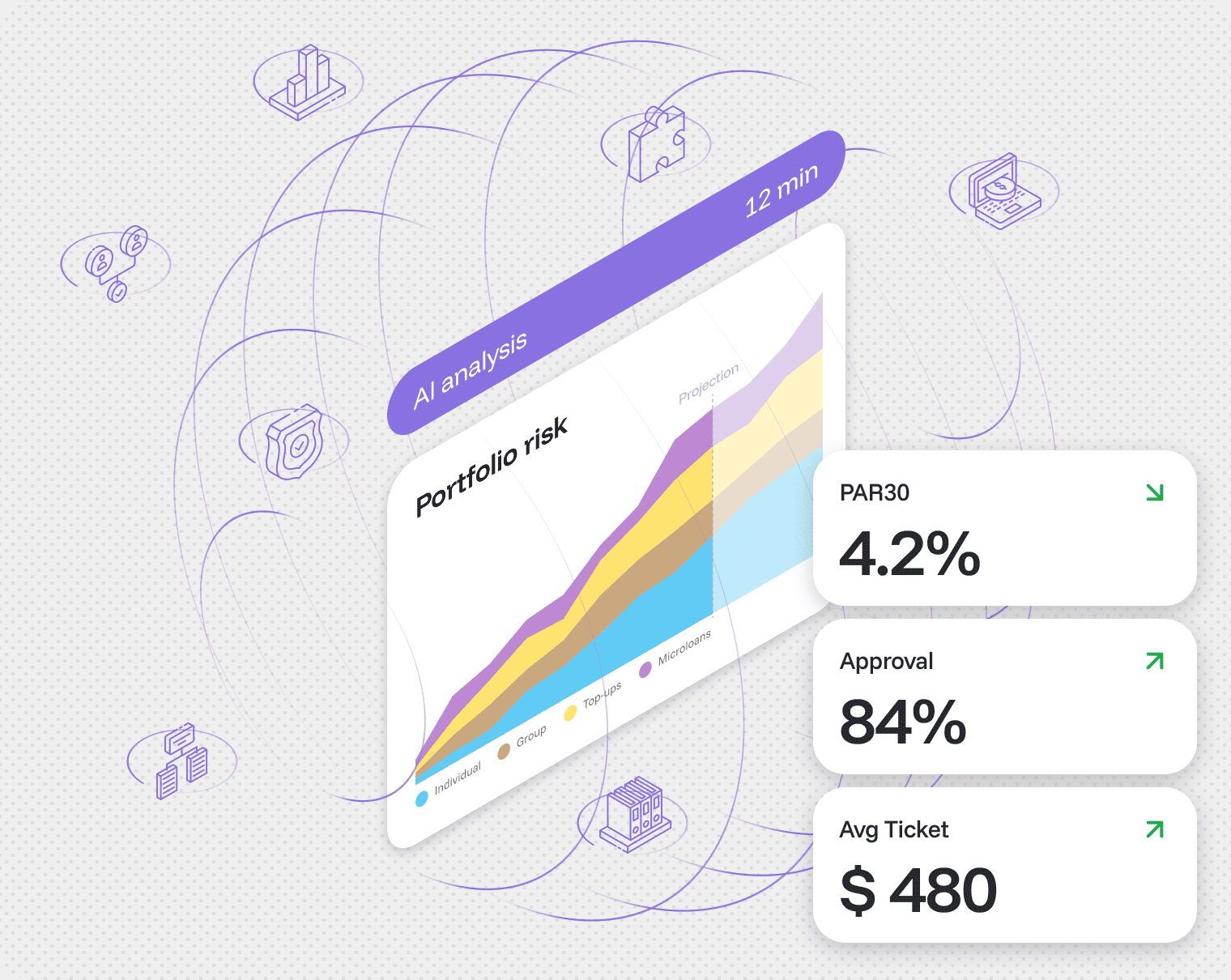

Where timveroAI accelerates implementation, the XAI scoring engine handles runtime decisioning. Two different capabilities of the Building Platform, kept distinct on purpose. Models train in your environment on your data. Decisions stream through the same policy layer as the rest of your micro loan software. Every model output, every policy version, every override is logged.

-

Thin-File Affordability and Default-Risk Scoring

Alternative-data pipelines feed transparent feature weights ready for credit committee and regulator review. Estimates affordability from telco, wallet, and device signals; produces reason codes on every approval and decline.

-

Fraud and Collusion Detection

Scored at application and at servicing events. Catches identity manipulation, synthetic profiles, agent-borrower collusion, and behavioral anomalies that bureau-only data misses entirely.

-

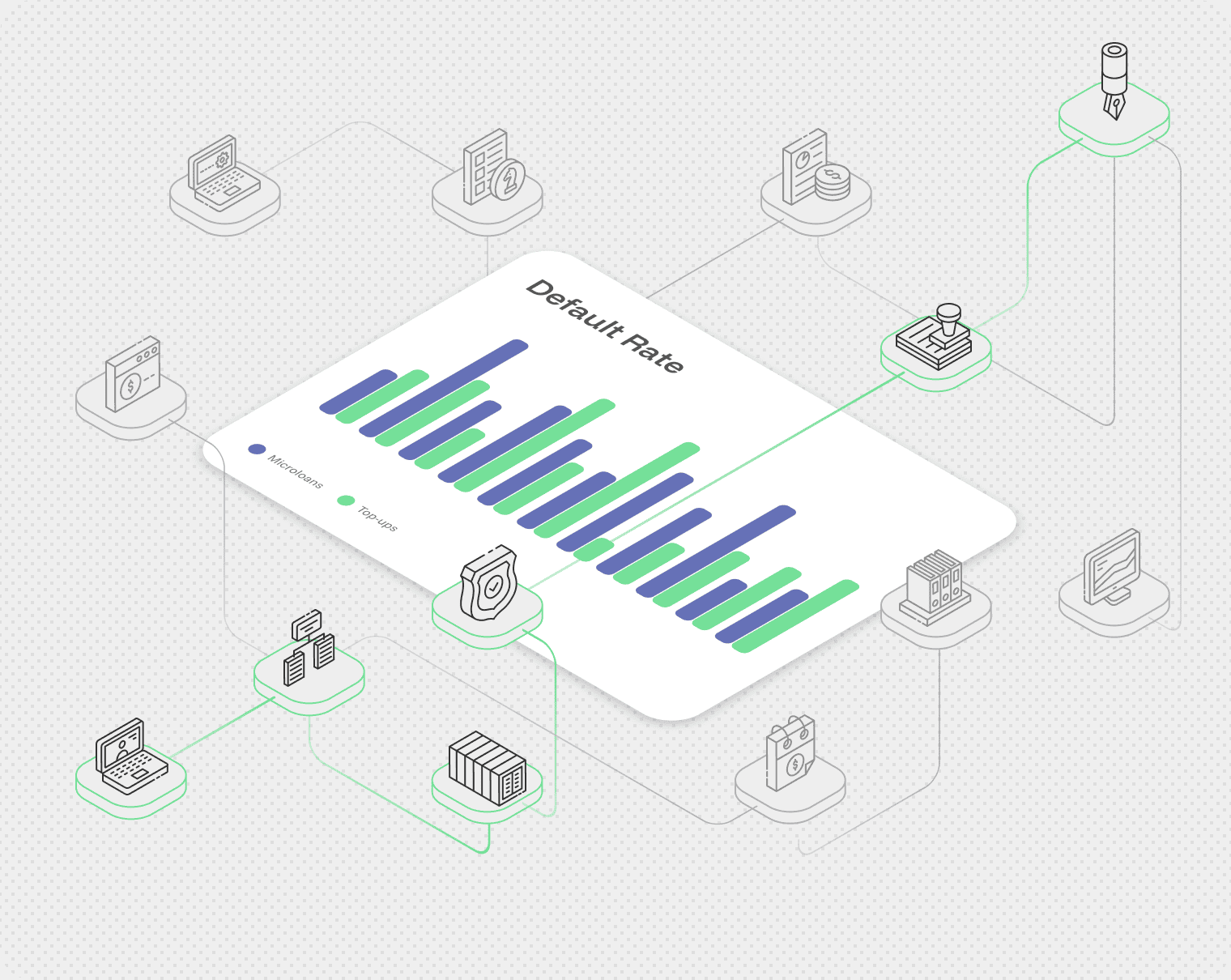

PAR30/90 Prediction and Cure Probability

Surfaces the borrowers most likely to slip into delinquency and the ones most likely to respond to outreach, hardship terms, or restructuring before charge-off.

-

Top-Up Eligibility and Portfolio Growth

Governed top-up offers based on repayment behaviour, exposure limits, and policy code. Accelerates responsible portfolio growth without lifting PAR. See full XAI scoring and portfolio analytics for runtime decisioning detail.

4 Reasons MFIs and Digital Lenders Choose timveroOS

-

Explainable Thin-File Scoring You Can Audit

Alternative-data pipelines feed a transparent scoring engine. Affordability, exposure limits, and segmentation waterfalls live as policy code with version history. Reason codes on every approval and decline. Governed override paths logged for credit committee and regulator review. Not a black box your risk team has to trust.

-

Offline-First Agent Operations

Field agents work in low-bandwidth environments with store-and-forward sync, multilingual UX, and built-in stips capture. Workflow guardrails enforce KYC, role-scoped approvals, and cash reconciliation in offline mode. Sync on reconnect. No off-process activity, no paper drift, no unreconciled month-end.

-

Wallet Disbursement and Clean Reconciliation

Native integrations across mobile money rails and regional payment systems. Cash-in and cash-out flows automate, settlement calendars enforce, and wallet provider files reconcile to your general ledger on schedule. Finance teams cut leakage and audit prep time across the portfolio.

-

Policies-as-Code for Hardship, Top-Ups, and Collections

Posting logic, fee structures, hardship workflows, dunning sequences, and top-up eligibility live as versioned policy code on the Building Platform. Change one rule, see who approved it, when, and why. Run shadow mode before production rollout.

Your Microfinance Stack, Integrated as Building Blocks

Mobile money rails, MNO data feeds, KYC and AML providers, credit bureaus where they exist, alternative-data sources where they do not, payment rails, and your core systems connect natively to timveroOS. Implemented during deployment, owned in your code. New vendors get composed by timveroAI in days via the Open SDK. No marketplace dependency, no per-call surcharges, no integration partner gatekeeping.

-

Wallets and Mobile Money

Whether your wallet rail is M-Pesa, MTN MoMo, Airtel Money, or a regional EMI, cash-in and cash-out tokenize and reconcile to the same general ledger as bank disbursements. New rails compose in days through the Open SDK.

-

MNO and Telco Data

USSD shortcode integration and SIM-based borrower identification feed the same onboarding flow as the mobile app. Telco usage signals feed alternative scoring where the regulatory framework permits.

-

KYC, Biometrics, and AML

Whether your identity vendor is Smile ID, Onfido, or a regional provider, liveness checks, document OCR, sanctions, and PEP screening run as first-class building blocks alongside biometric capture.

-

Bureaus and Alternative Data

Where bureaus exist, native connectors. Where they do not, alternative-data pipelines from telco, wallet, and device signals feed the same affordability and default-risk logic.

-

Payment Rails and Banks

Local ACH, instant payment systems, agent network APIs, and core banking adapters via the Open SDK. Bank file reconciliation automates against the same data model as wallet settlements.

-

Core, BI, and CRM

Salesforce, HubSpot, Tableau, Power BI, Looker, GL platforms, and custom data warehouses connect through architectural integrations, not marketplace permissions. Add a regional or niche provider through the SDK in days.

Trusted by Microfinance Lenders Worldwide

MFIs, digital lenders, and credit unions running thin-file portfolios at scale. Different operating models, same architectural primitives on the Building Platform.

-

Microfinance Institutions (MFIs)

Launch and scale individual, group, and guarantor lending on a Building Platform built for thin-file borrowers. Offline-first agent onboarding. Alternative-data scoring with reason codes. Wallet disbursement and clean reconciliation. Versioned policy code your regulator can audit and your credit committee can defend.

-

Digital Lenders and Microfinance Fintechs

Run instant pre-qualification, device and fraud checks, and low-touch servicing while keeping code, data, and release control. timveroOS gives microfinance fintechs a compliant Building Platform foundation to scale on portfolio-tiered pricing, not per-loan or per-seat fees. Unit economics stay intact at scale.

-

Credit Unions (Member Microloans)

Launch member microloan products on the Building Platform admin panel. timveroAI handles the heavy configuration. Your IT team focuses on credit-union-specific extensions through the SDK. Member-focused affordability logic. Portfolio-tiered pricing scales with assets, not with logins. Private-cloud or on-premise deployment keeps member data in your environment.

AMIO Bank: Complex Guarantor Lending in 6 Months After 3 Failed Attempts

- 80% ready-to-use lending infrastructure supplied

Finom

timveroOS partners with a fast-growing European fintech to launch a multi-country proactive credit product for SMEs delivering full automation, regulatory compliance, and rapid market rollout at a fraction of the cost and time of traditional banking systems.

Read now - 90% cost reduction compare to the previous solution

Cartiga

timveroOS enables a US-based litigation finance company to launch complex working capital products for law firms while achieving full automation, faster time to market, and significantly lowering costs compared to their previous enterprise platform.

Read now - 100% bespoke origination requirements coverage

AMIO Bank

timveroOS enabled a leading Armenian bank to transform a complex lending concept with guarantor support into a fully automated, production-ready solution. The platform ensured full compliance and rapid deployment - bringing the new product to market in just six months.

Read now

SaaS vs Building Platform vs Custom Development for Microfinance Software

SaaS microfinance platforms launch quickly but trap your credit model in vendor schema. Custom builds give you full control at the cost of 9 to 18 months and a long maintenance tail. The Building Platform delivers SaaS speed with custom-level control: faster deployment, predictable TCO, full governance. Policies-as-code for posting, fees, hardship, and collections, running in your own environment.

SaaS solutions

Pros

- Fast initial go-live

- Lower upfront cost

- Prebuilt workflows for vanilla products

Cons

- Schema lock-in on non-standard microfinance structures

- Per-seat and per-loan fees escalate TCO at scale

- Limited flexibility for agent ops, group lending, alt-data

timveroOS

Features

- Modules and SDK in your environment

- Policies-as-code: posting, fees, hardship, collections

- Open APIs to core, GL, rails, bureaus

- Immutable log: explainable changes and reversals

- Portfolio-tiered pricing (no per-seat or per-loan traps)

- From signing to first disbursement in 3 to 6 weeks with timveroAI

Custom Development

Pros

- Full control of code and UX

- Tailored integrations and data model

- No vendor lock-in

Cons

- 9 to 18 month delivery risk

- High build and maintenance cost

- Talent and knowledge concentration risk

SaaS solutions

Pros

- Fast initial go-live

- Lower upfront cost

- Prebuilt workflows for vanilla products

Cons

- Schema lock-in on non-standard microfinance structures

- Per-seat and per-loan fees escalate TCO at scale

- Limited flexibility for agent ops, group lending, alt-data

timveroOS

Features

- Modules and SDK in your environment

- Policies-as-code: posting, fees, hardship, collections

- Open APIs to core, GL, rails, bureaus

- Immutable log: explainable changes and reversals

- Portfolio-tiered pricing (no per-seat or per-loan traps)

- From signing to first disbursement in 3 to 6 weeks with timveroAI

Custom Development

Pros

- Full control of code and UX

- Tailored integrations and data model

- No vendor lock-in

Cons

- 9 to 18 month delivery risk

- High build and maintenance cost

- Talent and knowledge concentration risk

Frequently Asked Questions

Common questions from product, risk, and engineering leaders evaluating microfinance software on a Building Platform.

Talk to Our Team-

What is microfinance software?

Microfinance software is the platform that MFIs, digital lenders, fintechs, and credit unions use to onboard borrowers, score thin-file applicants, disburse loans to wallets or bank accounts, service repayments, and report portfolio health. It covers individual lending, group lending with guarantors, agent-led field onboarding, and digital self-service. timveroOS is microfinance software on a Building Platform with policies-as-code, alternative-data scoring, offline-first agent ops, and explainable AI. You deploy and own the environment. The same primitives power microfinance management software, micro loan management software, and digital-only microlending stacks.

-

How is timveroOS different from TurnKey Lender, Mambu, or other microfinance platforms?

Generic SaaS microfinance platforms ship a fixed schema and ask you to fit your credit model into it. timveroOS is microfinance software on a Building Platform. Building blocks for participants, policies, workflows, integrations, and ledgers compose into your specific micro loan product. You deploy in your environment with code-level access. timveroAI accelerates configuration from 3 to 6 months down to 3 to 6 weeks. Pricing is portfolio-tiered, not per-seat or per-loan.

-

What is thin-file scoring and how does timveroOS handle it?

Thin-file scoring is credit decisioning for borrowers with no bureau record, no formal payslip, and limited transaction history. timveroOS ingests alternative data (telco usage, wallet activity, device signals, employment proxies) plus open banking and bureau feeds where available. Affordability rules and exposure limits live as policy code with reason codes on every decision. The Building Platform scoring engine returns explainable outputs that pass credit committee review and regulator audit. Not a black box.

-

How long does it take to launch a micro lending software product on timveroOS?

A typical micro loan management product launches in 3 to 6 weeks on timveroOS, compared to 3 to 6 months on legacy LMS implementations or 9 to 18 months on a custom build. timveroAI composes the configuration from existing building blocks, then human-in-the-loop reviews and shadow-run testing validate before production. The first up-and-running deployment usually lands within the first week. The micro loan management system itself, with full servicing and collections, follows.

-

Can we deploy timveroOS in our own environment, and who owns the data?

Yes. timveroOS deploys in your environment: public cloud (AWS, Azure, GCP), private cloud, hybrid, or on-premise. You own the deployment, the source code your team extends, and the borrower and portfolio data. This is the Building Platform core principle, distinct from multi-tenant SaaS where data and code live with the vendor. Data sovereignty and regulator-required residency are not procurement edge cases for us, they are the default.

-

Which mobile money and wallet rails does timveroOS support for microfinance?

timveroOS integrates with the major mobile money rails through native building blocks. Whether your wallet provider is M-Pesa, MTN MoMo, Airtel Money, Orange Money, or a regional EMI, cash-in and cash-out automate and reconcile to your general ledger. Bank payment rails, agent cash networks, and new EMIs plug in via the Open SDK as additional building blocks. New rails compose in days, not quarters.

-

What regulatory and compliance frameworks does timveroOS support for MFIs?

The Building Platform surfaces every decision, policy, and configuration change as versioned code with immutable audit logs. This works across regulatory frameworks that prioritize transparency and audit trails: central bank microfinance regulations across Africa, Asia, and Latin America; data privacy regulations including GDPR, CCPA, and regional equivalents; AI governance rules requiring explainable decisioning. Compliance teams configure policy code directly. Regulators read the same versioned logic.

Related Lending Solutions

Launch Your Microfinance Product on timveroOS

$5.5B+ managed across 13+ countries. From signing to first disbursement in 3 to 6 weeks with timveroAI.

Request a Demo Explore the Architecture