Why Digital Banks Keep Taking Share and Why AI Is About to Widen the Gap

AI is rewriting one vertical after another — coding, legal work, customer support — and in each, the winners are the teams working within an AI-native platform, not the incumbents bolting AI onto old software. Lending is next, and it is one of the largest verticals of all. That is why the debate about digital banking vs traditional banking has quietly stopped being about apps and branches and become a question of unit economics: digital banks operate at a fraction of the cost per customer, launch products in weeks rather than quarters, and post returns most incumbents cannot match.

That gap was already structural before generative AI arrived; now, AI is multiplying the advantage of the side that was already ahead, while institutions still treating it as a series of pilots fall further behind. The encouraging part is that the gap is not closed by buying another point tool. It is closed by changing the foundation underneath lending — moving to a programmable, AI-native building platform, a team can build and change on at challenger speed, not a fixed application you configure, and without losing the auditability regulators require. The next two to three years will decide which side of the line a lender lands on.

Executive summary

- Digital banks are structurally more efficient. Digitally mature institutions report 30–50% lower cost-to-serve and launch products 40–60% faster than branch-heavy incumbents.

- They are already taking share and profit. The largest fintechs now make up roughly 17% of combined banking-and-fintech revenue, and leading neobanks post returns on equity (30–35%) above most incumbents.

- AI is the multiplier — and most banks are stuck. Between 78% and 88% of AI pilots in financial services never reach production; only around one in seven institutions has scaled AI into production. The blocker is rarely the model — it is the architecture and delivery model underneath it.

- The window is roughly two to three years. Legacy systems delay product launches by 6–18 months while challengers ship every few weeks. The way to close it is a programmable, AI-native platform that lets a team build and change lending products at challenger speed — AI for speed, deterministic logic for the credit decision.

How much share digital banks have already taken

For years, the comfortable story inside incumbent banks was that challengers would win the young and the unprofitable, then plateau. That story no longer holds. According to McKinsey’s Global Banking Annual Review 2026, the largest fintechs now account for roughly 17% of combined banking and fintech revenues and are growing several times faster than traditional banks (McKinsey, 2026 (opens in new tab)). This is no longer a niche at the edge of the market; it is a structural reallocation of where banking revenue is created.

The scale of individual challengers makes the point concrete. Leading neobanks now serve customer bases that rival national incumbents, and — critically — they do so profitably. McKinsey notes that several challengers have broken through the old growth-versus-profitability trade-off entirely, posting returns on equity in the 30–35% range, ahead of most established banks (McKinsey, 2026 (opens in new tab)).

The demand signal is just as clear on the customer side. Among younger US households, switching intent toward digital-first providers is markedly higher than the market average, and a majority of consumers who changed provider recently cited better online and mobile banking as the primary reason. The institutions losing those customers are not just losing a checking account — they are losing the lifetime value of the next generation of borrowers.

Digital banking vs traditional banking: why the gap is structural

It is tempting to read the shift as a user-experience story — slicker apps win. But the durable advantage is in the cost base and the speed of change, not the interface. Two structural differences explain most of it.

Cost structure

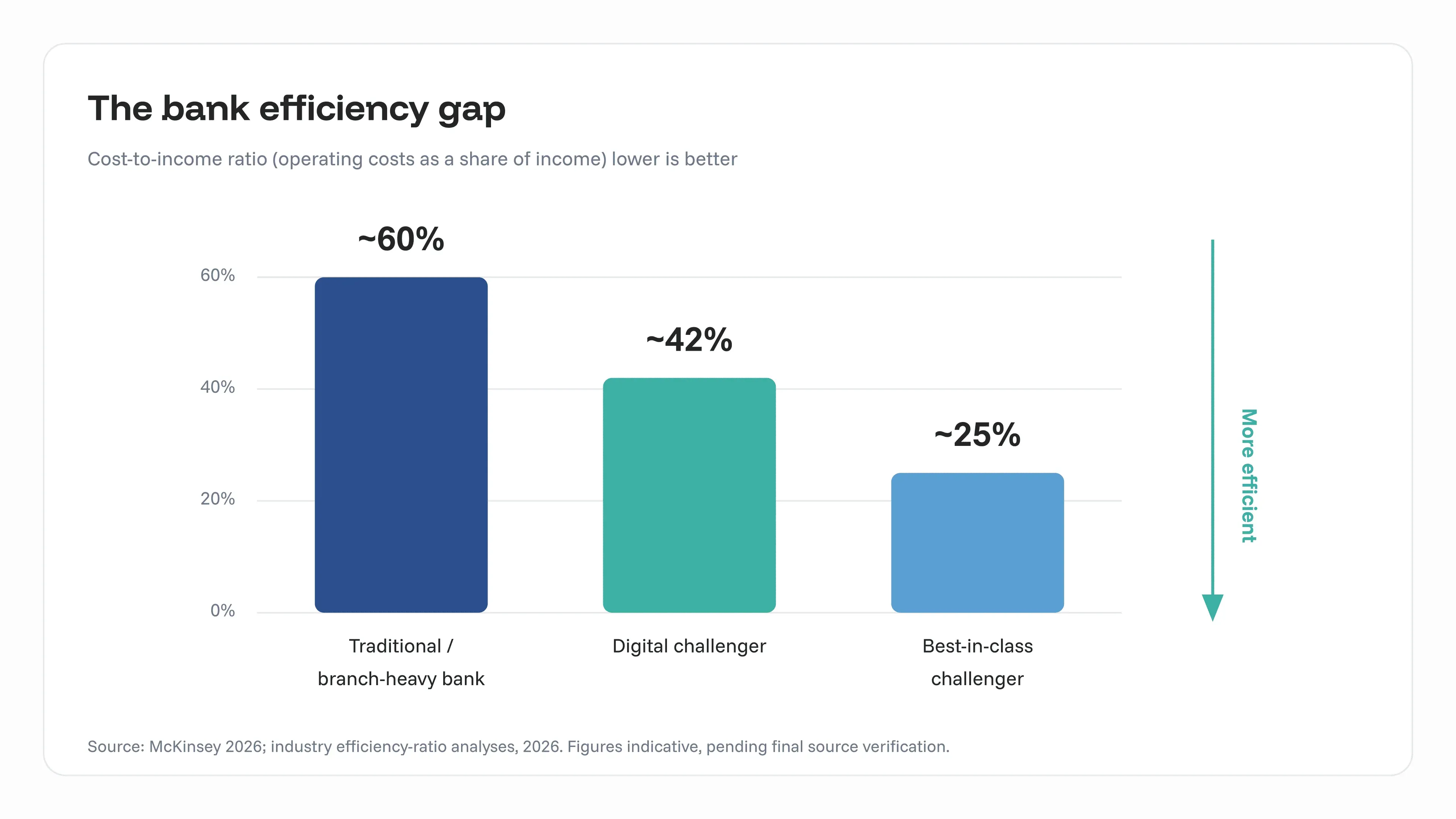

Traditional banks carry the cost of branch networks, in-person staffing, and decades of accumulated legacy systems in banking that must be maintained, patched, and worked around. Digital banks were built without most of that overhead. The result shows up directly in the bank efficiency ratio — operating expenses divided by income, where lower is better. Top-performing incumbents operate in the 50–55% range, with elite institutions dipping below 50%; digital-only banks routinely run in the 35–50% band, and the most efficient challengers post efficiency ratios in the mid-20s. Put plainly, an efficient digital bank can spend 25–35 cents to earn a dollar, where a branch-heavy incumbent spends 55–65 cents.

That difference compounds. Industry analyses put digitally mature banks at 30–50% lower cost-to-serve than their branch-heavy peers. Lower cost-to-serve means a challenger can offer better pricing, absorb thinner margins on new products, and still fund growth — while the incumbent’s cost base quietly caps how aggressive it can be.

Speed of change

The second structural gap is velocity. Challengers ship product updates every two to four weeks; many incumbents move on a four-to-six-month cycle, and net-new products can take far longer. Legacy core systems are the constraint: industry research finds that outdated infrastructure delays product launches by 6 to 18 months and consumes a disproportionate share of the IT budget just to keep the lights on. Every quarter a new credit product is stuck in implementation is a quarter the challenger is already in market, learning, and iterating.

This is the reading that matters for a lender: the digital advantage is not “a nicer app.” It is a lower cost base and a faster clock — two things that determine who can profitably launch and evolve credit products.

AI is the multiplier — and it is widening the gap

Here is the part incumbents underestimate. AI does not create the efficiency gap; it amplifies the gap that already exists. Challengers that already build fast and run lean are using AI to compress cost structures and ship products in weeks rather than years — and McKinsey is explicit that for incumbents who have not moved decisively, “the competitive gap is widening” (McKinsey, 2026 (opens in new tab)).

The uncomfortable data is about execution, not ambition. Surveys in 2026 found that between 78% and 88% of AI pilots in financial services never reach production, and that only around one in seven institutions has successfully scaled AI into production (BizTech, 2026 (opens in new tab)). A separate banking-compliance study found that while roughly 70% of banks use AI to some degree, only about 12% describe their AI strategy as well-defined and properly resourced (Wolters Kluwer, 2026 (opens in new tab)).

The most important finding is why pilots stall. As one 2026 analysis put it, banks running AI pilots are discovering that the models are not the problem — the architecture underneath them is. Most large banks run on a patchwork of legacy cores, and bolting machine learning onto that patchwork requires middleware, API layers, and integration work that turns every model into a project. The gap is a delivery-and-architecture problem disguised as a technology problem.

That is why AI widens rather than narrows the gap. A challenger built on modern architecture turns a new model into a feature in weeks. An incumbent on legacy cores turns the same model into an 18-month integration program — if it reaches production at all. Same model, opposite outcome, because the foundation is different.

Where the gap gets monetized: lending

Efficiency and speed are abstract until they hit the line of business where banks actually make money. For digital banks, that line is increasingly lending. Payments and checking accounts bring users in, but net interest income — lending, credit cards, overdrafts, BNPL — is where the profit and the durable relationship live. Industry coverage is consistent that for most profitable digital banks, net interest income forms the bulk of operating revenue, and that credit products offer the best monetization and retention (PYMNTS, 2025 (opens in new tab); Bain, 2025 (opens in new tab)).

This sets up two mirror-image pressures on the same product line. Most neobanks are not yet profitable; the ones that are share a single trait — a real lending engine generating net interest margin, because interchange-only models do not get there. So for a digital bank the imperative is offensive: launch credit products fast and start earning NIM, since the faster it launches and iterates, the sooner it turns profitable and wins its cohort. For an incumbent the same battleground is defensive: challengers are aiming their efficiency advantage squarely at the most profitable product line, yet lending is precisely where an incumbent’s data, balance sheet, and regulatory standing are strongest — if the lending stack can move fast enough to use them. Either way, the institutions that can launch, price, and adjust credit products at challenger speed are the ones that capture the margin; the rest cede it.

The two-to-three-year window: the cost of waiting

None of this is a distant scenario. The cost of inaction is already measurable. Industry research finds that 64% of banks admit slow digital transformation has cost them new customers, and that banks lose a meaningful share of customers to better-equipped competitors each year. Legacy delays of 6–18 months on product launches translate directly into ceded ground, and McKinsey’s framing is that the gap widens specifically for those who do not move.

Compounded over two to three years, that is the difference between defending a franchise and managing a decline. The challengers are not standing still during that window — they are using AI to pull further ahead. The uncomfortable reframe is that hand-built, vendor-locked lending — slow to change, dependent on a roadmap you do not control — has itself become a competitive liability, not just a cost center. “Wait and see” is not a neutral position; it is a decision to let the gap compound. The realistic question for a lender is not whether to modernize, but how to do it fast enough to matter, without taking on risk the institution cannot defend to a regulator.

What actually closes the gap: speed without losing control

The instinct, when the gap becomes obvious, is to buy another AI feature. That instinct is part of the trap — it adds one more model to a patchwork that already cannot ship, and a smarter assistant that still only helps you pick from a vendor’s pre-built menu. Most lending platforms are configurable: you set parameters inside a fixed model the vendor built, and even their AI just helps you choose from that fixed set of options. What actually closes the gap is a platform that is programmable rather than configurable — where the building blocks themselves compose into whatever lending product, risk model, or workflow a team needs. It is the difference between a menu and an open kitchen.

This is what timveroOS is built to be: the default AI for lending teams — a programmable, AI-native platform that automates lending operations end-to-end, at a bespoke level, compliantly. AI accelerates the two things that used to be slow — building new processes and adjusting existing ones — so a vendor change request and weeks of waiting become a same-day change the lending team makes itself. timveroAI is the AI layer driving that build-and-change work: grounded on the bank’s own policies, operating with human-in-the-loop approval gates, and able to run in shadow-run mode that tests changes against live conditions before anything ships. Crucially, the credit decision itself does not run on a language model that can guess wrong — it runs on deterministic, explainable logic, so the same inputs always produce the same auditable output. That is the whole point: AI for speed, deterministic logic for the decision — speed with the reproducibility a regulated lender requires, not speed instead of control.

The payoff is competitive and operational at once. A lender moving at challenger speed launches the products its customers want before rivals do, and because the same team composes and operates products without waiting on engineering or a vendor roadmap, it runs a far larger book with sharply lower effort per loan. Speed, leverage, and trust — together.

The proof that this is achievable rather than aspirational is in production. Working on timveroOS, Finom reached up to 98% automation of its lending processes — challenger-grade efficiency on a platform built to evolve. The proof in the room is simple: change a rule or a product parameter and watch it run the same day.

Digital banking vs traditional banking: side-by-side

| Dimension | Traditional / branch-heavy | Digital / challenger |

|---|---|---|

| Cost base | Branches, in-person staffing, legacy maintenance | Lean, digital-first; minimal physical overhead |

| Bank efficiency ratio | ~55–65% typical | ~35–50%, best-in-class mid-20s |

| Cost-to-serve | Baseline | 30–50% lower |

| Product launch cycle | Quarters; net-new delayed 6–18 months | Updates every 2–4 weeks |

| AI delivery | Model becomes a multi-quarter integration | Model becomes a feature in weeks |

| Primary profit engine | Spread + fees, broad portfolio | Net interest income / lending, optimized |

| Regulatory standing | Strong (charter, balance sheet, data) | Often partner-dependent |

Data snapshot: the efficiency gap in numbers

| Metric | Figure | Source |

|---|---|---|

| Fintech share of banking + fintech revenue | ~17% | McKinsey 2026 |

| Leading neobank ROE | ~30–35% | McKinsey 2026 |

| Digital bank cost-to-serve advantage | 30–50% lower | Industry analyses 2026 |

| Faster product launches (digitally mature) | 40–60% | Industry analyses 2026 |

| AI pilots that never reach production | 78–88% | 2026 industry surveys |

| Banks with a well-defined, resourced AI strategy | ~12% | Wolters Kluwer 2026 |

| Legacy-driven product launch delay | 6–18 months | Industry research 2026 |

| Banks saying slow digitization cost them customers | 64% | Industry research |

Frequently asked questions

How are digital banks different from traditional banks?

Digital banks operate without branch networks and most legacy infrastructure, which gives them a lower cost base, a better bank efficiency ratio, and a far faster product cycle. Traditional banks offer physical presence, a broad service range, and strong regulatory standing, but carry higher overhead and slower change cycles.

Why are digital banks more efficient?

The advantage is structural, not cosmetic. No branches and modern architecture mean a lower cost-to-serve (30–50% below branch-heavy peers) and efficiency ratios in the 35–50% range versus 55–65% for many incumbents.

Is AI helping banks catch up to challengers?

Only where it reaches production. Most AI pilots in banking (78–88%) never get there, because the obstacle is the legacy architecture underneath the models, not the models themselves. AI tends to widen the gap, because challengers can ship models as features while incumbents turn them into long integration projects.

Which products are most at risk?

Lending. Net interest income is the main profit engine for most profitable digital banks, so credit products are exactly where challengers aim their efficiency advantage — and where incumbents have the most to defend.

How long do incumbent banks have to respond?

Realistically two to three years. Legacy delays of 6–18 months per launch compound while challengers ship every few weeks, so the gap widens for institutions that wait.

How can a traditional bank move at challenger speed without losing control?

By changing the foundation rather than adding tools. A programmable platform — the difference between an open kitchen and a vendor’s fixed menu — lets a team compose and change lending products itself, while the credit decision runs on deterministic, explainable logic rather than a language model that can guess. That is timveroOS, the default AI for lending teams: AI for speed, deterministic logic for the decision, and a full audit trail

See how a Building Platform lets your institution launch and evolve credit products at challenger speed — without losing auditability. Request a demo (opens in new tab).

-rsbxq-400x250.webp)

CEO at TIMVERO

Dmitriy Wolkenstein is the CEO of TIMVERO, leading the team building timveroOS and timveroAI. He writes about why the next generation of lending will be won at the infrastructure layer — and what it takes to get there.

LinkedinLatest News

Digital Transformation in Lending: What Actually Works

“We’ll Build Our Own LMS”: Why That Decision Might Cost You More Than You Think

Embedded Lending Platform: APIs and Technical Requirements

Boxed LMS vs SDK-Based Platform: What Will Growing Fintechs Choose in 2025?

How to Build Composable Loan Management Software Using an SDK: A Step-by-Step Guide for Fintech Teams

How FinTechs Build Loyalty via Design, Speed & Transparency

BNPL Software in 2026: Build, Buy, or Composable Infrastructure?

The Race to Real-Time Lending: Why Static Loan Systems Are Holding You Back

Ethics in Automated Lending: Can AI Make Fair Credit Decisions?