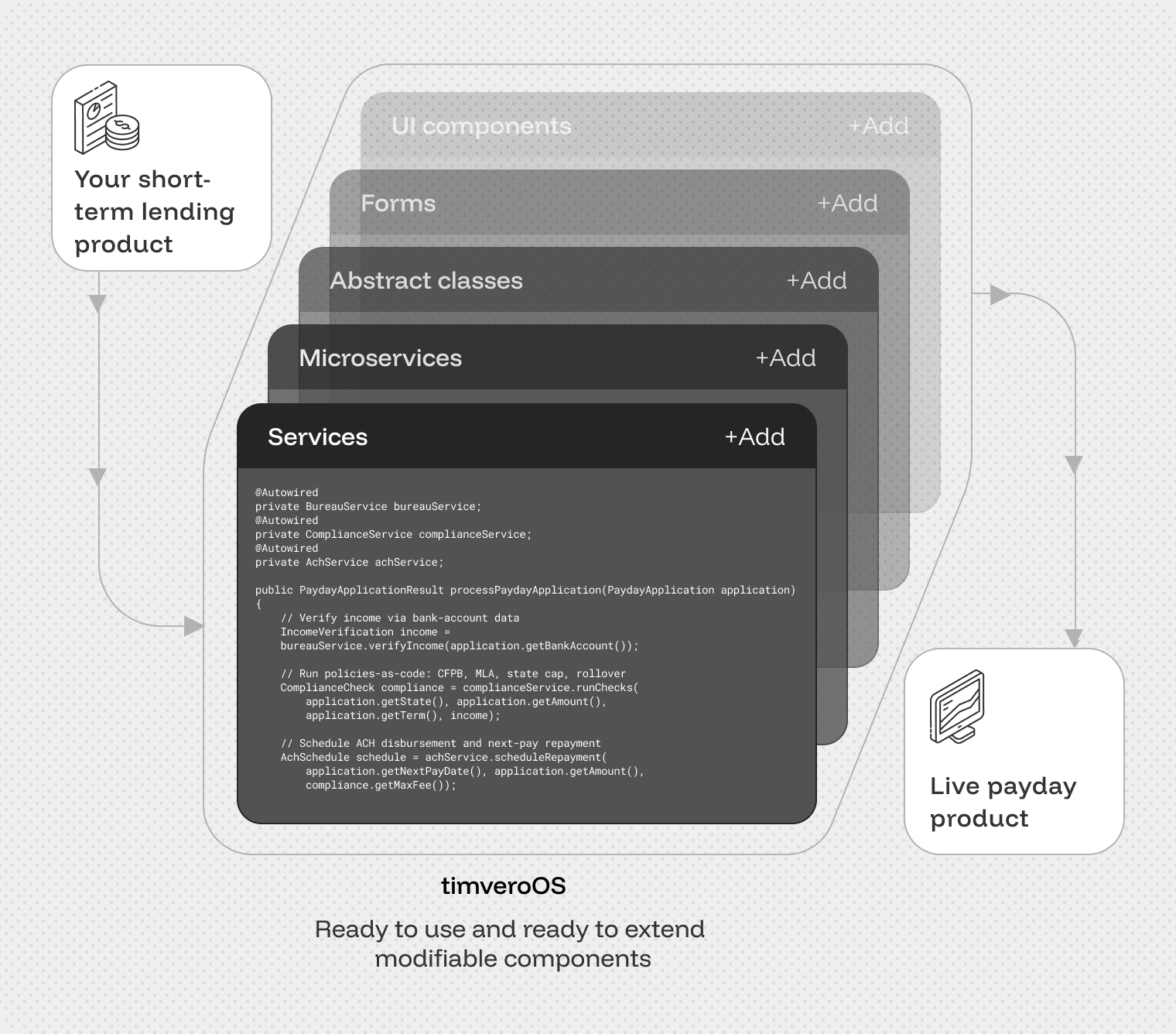

Payday, cash advance, and PAL products run on cycles measured in days, not months. Generic loan management software treats them as installment edge cases — forcing workarounds, hidden compliance risk, and slow product launches across state-by-state rule fragmentation.

-

State-by-State Rule Changes Break the Roadmap

Each rate-cap update, MLA test, or CFPB rule lands in vendor backlog. Your launches stall behind 50 other tickets.

-

PALs Program Economics Don’t Fit Per-User SaaS Pricing

NCUA-compliant short-term lending should match member-to-staff ratios — not seat-count licensing models.

-

Audit Trails Depend on Vendor Configuration

CFPB and state examiners want explainable decisioning. Most LMS platforms hide the logic behind a vendor permission gate.

-

Cycle Automation Requires Workarounds

ACH disbursement, rollover detection, rate disclosures, and collections sequencing get bolted onto installment-loan schemas, not built natively.