AI Agent vs Credit Scoring: The Two Layers of Lending AI

In lending, “AI agent” has come to mean two completely different products. One is an AI that builds and changes the lending system itself; the other is an AI that makes the credit decision on each application. They run at different moments, produce different outputs, and answer to different regulators — which is exactly why treating them as one thing creates both product and compliance problems. This article separates the two layers, explains why each is governed differently, and shows how a build-time implementation agent and a deterministic credit-scoring engine work together on a Building Platform like timveroOS.

At the end of our last piece on the AI banking efficiency gap (opens in new tab), we promised to treat one distinction on its own, because it is doing more damage than any other piece of loose language in the market right now: the difference between an AI agent that builds a lending system and an AI that makes a credit decision. They get called the same thing — “AI in lending,” or lately “an agent” — and they are not the same thing. One operates while you are designing and changing the product. The other operates every time a borrower applies. They produce different outputs, demand different controls, and fall under different regulators. Treating them as one product is how a lender ends up either letting a language model improvise credit decisions, or waiting on a scoring engine to do a job it was never built for. This is a question about the programmable Building Platform underneath the lending business — specifically, about keeping two kinds of AI on it cleanly separated. The rule we hold to across this series is simple: AI for speed, deterministic logic for the decision.

Executive summary

- “AI agent” in lending now means two different products. One is a build-time agent that assembles and changes the lending system; the other is run-time credit AI — scoring and decisioning — that evaluates each borrower. Different jobs, different risk, different governance.

- The decision layer is governed as a model. AI used to assess creditworthiness is high-risk under the EU AI Act (Annex III), is squarely in scope of the Federal Reserve’s SR 11–7 model risk guidance, and must produce specific, accurate reasons for denial under ECOA — the CFPB has said plainly that a “black box” is not an excuse.

- The build layer is governed as software change. An implementation agent configures a pre-validated framework, not credit outcomes — so the right controls are divergence testing, shadow runs and human approval gates, not the model-risk validation a scoring model requires.

- Conflating the two is the expensive mistake. Give a free-roaming agent the credit decision and you have a compliance incident waiting to happen; expect a scoring engine to redesign your product and you are still standing in the vendor queue. The fix is to keep them separate: an agent to build, a deterministic engine to decide.

Why “AI agent” now means two different products

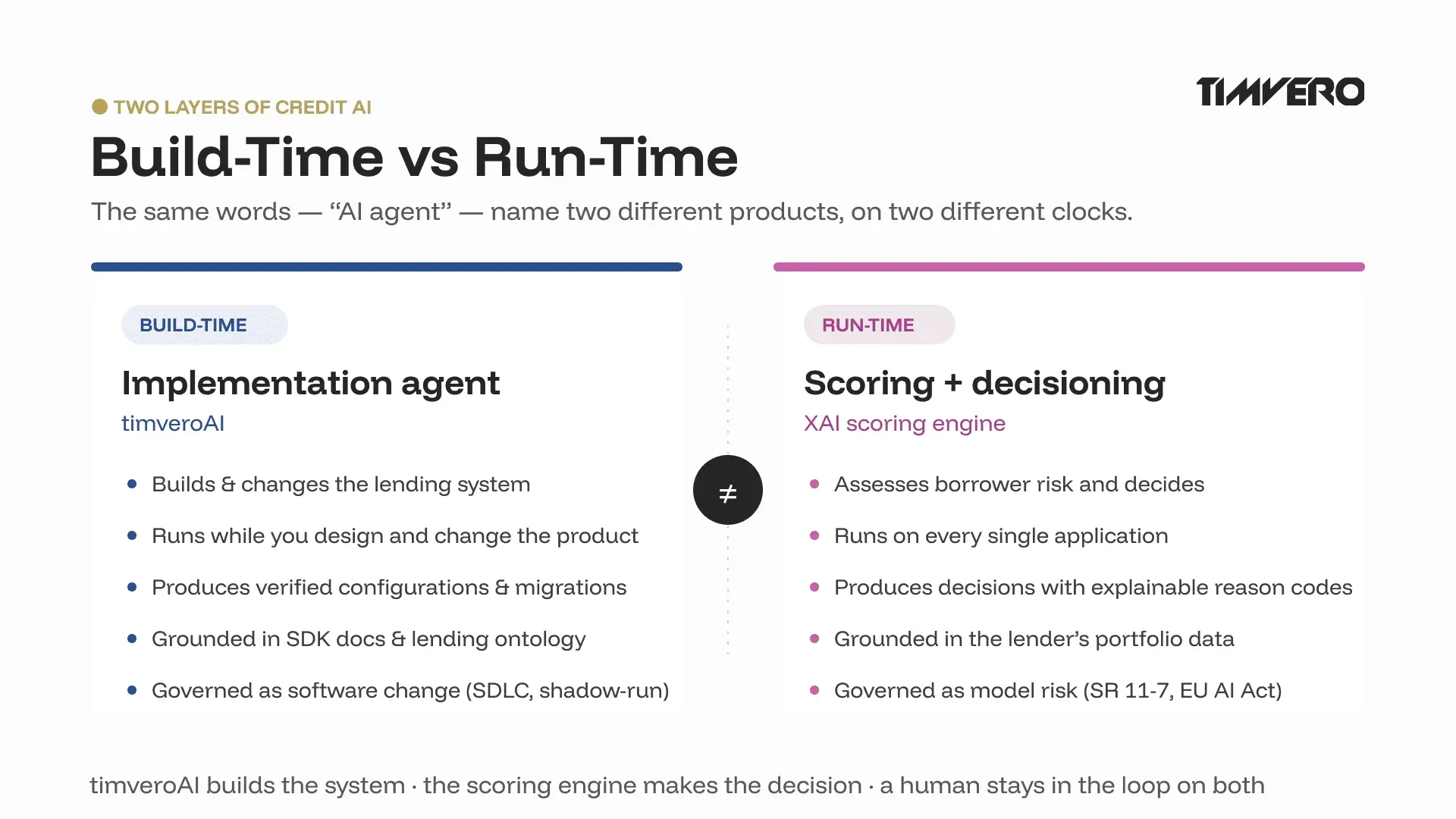

Walk through the lending-technology content of the last year and you will find “agent” used almost exclusively for one thing: an autonomous worker that reads a borrower’s data and reaches a credit decision. There is even a tidy stack diagram doing the rounds — data agents, verification agents, decisioning agents, coordination agents — and notice where the word “decision” sits. In that telling, an AI agent in lending is the underwriter.

That framing quietly erases an entire category of AI, and it happens to be the category that moves the economics. Because there are two distinct moments when AI can act on a lending business, and they are not interchangeable.

The first is run-time: the instant a borrower applies, when something has to score the risk and decide what to do about it. The second is build-time: the weeks before any borrower applies, when a team is assembling the product, encoding the policy, wiring the integrations and — later — changing all of it as the market shifts.

The distinction in one line. Build-time AI changes the lending system. Run-time AI makes the lending decision. They are different products, under different risk regimes, and conflating them is the costly mistake.

The reason this matters is not pedantic. The two layers have opposite requirements. The decision layer needs to be conservative, deterministic and explainable, because a regulator can ask it to justify any single output. The build layer needs to be fast and generative, because its whole value is compressing months of implementation into weeks. Ask one layer to behave like the other and you break it. The rest of this article takes each layer in turn, then shows what goes wrong when they are merged.

Layer 1: the credit decision (scoring and decisioning)

The run-time layer is the one most people already picture when they hear “AI in lending.” It is worth being precise about what lives inside it, because even here two things get blurred together.

Scoring is not decisioning

A credit score and a credit decision are different objects. Scoring answers one question — how risky is this applicant — by turning data into a number or a probability of default. Decisioning is the larger process that acts on that number: applying policy, checking affordability, assigning a limit, pricing the loan, running compliance checks and routing the file. A score tells you how risky someone looks; it does not tell you what to do, and decisioning is where the doing happens.

AI has genuinely improved the scoring half. Models that read broader and alternative data can separate good and bad risk more sharply than a fixed scorecard, and lenders deploying AI in credit decisioning have reported meaningful reductions in credit losses. But “better scoring” is precisely why the temptation arrives: if the model is this good, why not let it run the whole decision, end to end, on its own? The answer is not about model quality. It is about who has to answer for the output.

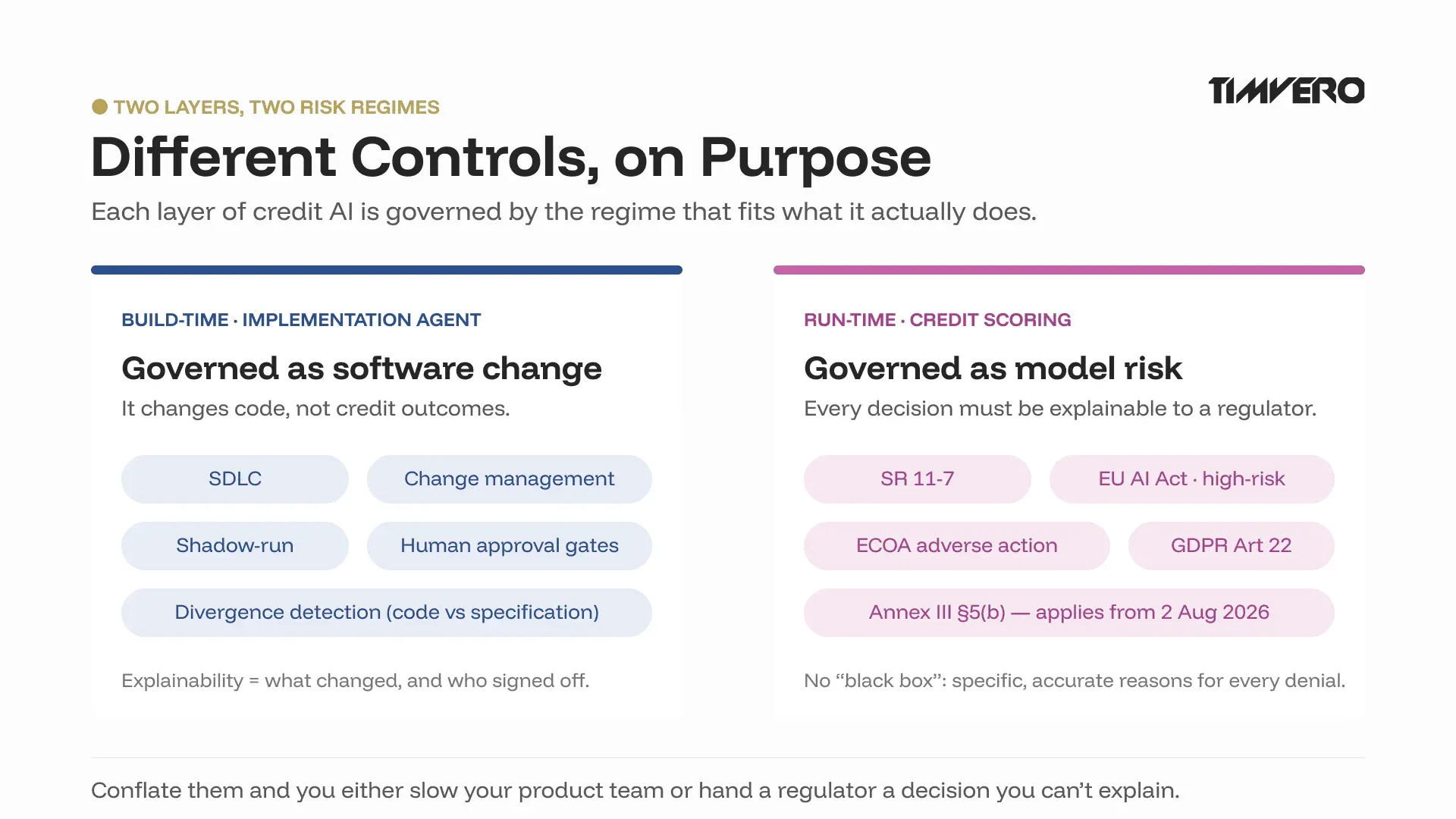

Why this layer is governed as a model

The moment AI assesses a person’s creditworthiness, it enters one of the most heavily supervised corners of financial technology — and the supervision is converging across jurisdictions.

In the United States, the Federal Reserve’s SR 11–7 has governed model risk since 2011, requiring institutions to validate models, understand their limitations and document the reasoning behind them; regulators have confirmed that AI and machine-learning credit models sit squarely within its scope (Federal Reserve, SR 11–7 (opens in new tab)). On top of that sits fair-lending law: under ECOA and Regulation B, a denied applicant is owed the specific, accurate principal reasons for the decision. The CFPB closed the obvious loophole in Circular 2023–03, stating that creditors “may not rely on” generic checklist reasons that don’t reflect the actual basis for denial, and that the complexity of an algorithm is no defense — a lender “cannot justify noncompliance with ECOA” on the grounds that its own technology is too complicated to explain (CFPB, 2023 (opens in new tab)).

In the European Union, the direction is the same and the label is explicit. The EU AI Act classifies AI used to evaluate the creditworthiness of natural persons or establish their credit score as high-risk (Annex III, point 5(b)), with the associated obligations — risk management, technical documentation, human oversight, bias testing — applying from 2 August 2026 (EU AI Act, Annex III (opens in new tab)). And the Court of Justice’s Schufa ruling already treats credit scoring as an automated decision under Article 22 of the GDPR, carrying a right to explanation and human review (CJEU, C-634/21 (opens in new tab)).

Put together, these are not compatible with a free-roaming agent improvising decisions. They demand a decision layer that is deterministic, explainable and reviewable by a human. That is exactly the design constraint behind a transparent, explainable AI scoring engine (opens in new tab): it produces a decision with reason codes, on logic a model-risk team can validate and a regulator can interrogate. The intelligence is real, but it is fenced — and the fence is the point.

Layer 2: the implementation agent (building and changing the system)

Now the layer the market keeps forgetting. There is a second place AI can act in lending, and it has nothing to do with deciding who gets a loan.

What an implementation agent actually does

An implementation agent operates on the system, not the borrower. It does not write a lending platform from scratch. It operates on system configuration, entity mapping and architecture orchestration within a pre-validated framework — turning a business requirement (“a 12-month installment product with a 30-day grace period and a floating rate”) into the assembled, working pieces of that framework: the entities, the state machines, the product configuration, the policies as code, the integrations. The base codebase is stable and already proven; the agent automates the assembly work on top of it. That is what compresses the gap between what a business analyst describes and what runs in production.

This is what timveroAI (opens in new tab) is. It is a RAG-grounded implementation agent: grounded in 33 chapters of SDK documentation, a feature ontology that encodes lending domain knowledge, and a library of working reference applications it can match and adapt. Its measurable effect is on the build, not the decision — implementation timelines moving from three-to-six months down to two-to-six weeks, and the share of engineer time spent on repetitive assembly work dropping from 60–70% to under 20%, with generated specifications landing above 85% accuracy (timveroAI overview (opens in new tab)).

That 85% figure is worth reading correctly, because to a risk officer “15% inaccurate” can sound like 15% defective. It is not. It means that in roughly 85% of cases the agent assembles the product configuration correctly on the first pass; in the remainder, an engineer opens the interface and adjusts a parameter or a relationship before deployment. That is a normal, iterative build loop with a human refining the last mile — not a defect rate, and not a system shipping broken. The crucial sentence: it does not issue credit decisions — it builds the system that issues them.

Why this layer is governed as software change, not model risk

Because the implementation agent changes system configuration rather than credit outcomes, the right control regime is the one software engineering already uses: change management, not model validation of every output. A configuration change to a pre-validated framework is governed the way any software change is — tested, reviewed and approved before it ships — not put through the model-risk validation that a credit-scoring model demands.

That is why the controls on this layer look different — and why the real risk is not the one people instinctively fear. Because the agent works inside a proven framework rather than writing novel code, the failure mode is not a hallucinated function or a syntax error. It is a logical one: the agent could misread a business requirement and wire up the wrong trigger for a floating rate, or misalign a product parameter. The controls are built for exactly that risk.

So a generated configuration passes through three gates before it goes live. First, divergence detection checks the assembled configuration automatically against the specification, flagging any place it drifts from what the analyst actually asked for. Second, it runs in shadow mode, exercised against historical data flows so its behaviour is observed before it ever touches a live borrower. Only then, third, does it reach a human-in-the-loop approval gate for sign-off. Explainability here means something concrete and different from the decision layer: not “why was this borrower declined,” but “what exactly did this configuration change, and who approved it.” Speed is the goal, and it is safe to pursue because a credit decision is never the output.

There is a compliance dividend in this design that technical buyers will recognise. An agent that configures a pre-validated framework is far easier to defend than one generating financial software from scratch: the underlying credit algorithms stay deterministic and auditable, and the provenance of every building block is known. That keeps the system on the right side of software-supply-chain-security expectations and simplifies the audit — there is no opaque, machine-written core to validate, only a known framework, configured.

Why conflating the two layers is the expensive mistake

Collapse the two layers into one “AI agent” and you can fail in two opposite directions, both costly.

Push the build layer’s autonomy onto the decision and you get the nightmare the regulators wrote their rules for: a system that approves and declines on logic no one can fully reconstruct. The first adverse-action notice it cannot specifically justify is an ECOA problem; under the EU AI Act it is an unmanaged high-risk system. “The model said so” is not a defense the CFPB accepts.

Push the other way — expect your scoring or decisioning engine to redesign the product, add a new repayment structure, wire in a new data source — and nothing happens, because that was never its function. The change goes back into the vendor or engineering queue, and every month it waits is a month a faster competitor is already live with it.

The rule that keeps both safe. You don’t want the model that approves loans rewriting the rules it approves them by — and you don’t want your scoring engine to be your product team.

The clean separation looks like this:

| Dimension | Implementation agent — build-time (timveroAI) | Credit scoring + decisioning — run-time (XAI scoring engine) |

|---|---|---|

| What it does | Builds and changes the lending system: products, policies, entities, integrations | Assesses borrower risk and approves, prices or routes the application |

| When it runs | During build, implementation and change | At every credit decision |

| Who uses it | Engineers and analysts configuring the platform | The lending product itself, on every application |

| What it produces | Verified configurations, entity graphs, automated migrations and specifications within the SDK | Decisions with explainable reason codes |

| What it’s grounded in | SDK docs, lending ontology, reference application library | The lender’s portfolio data and credit features |

| Risk regime | Software change: SDLC, change management, shadow testing | Model risk: SR 11–7, EU AI Act high-risk, ECOA adverse action |

| Failure mode | Logical misconfiguration (e.g. misaligned product parameters) — caught by automated divergence testing and shadow run | Opaque decision — adverse-action breach, regulatory exposure |

| Human’s role | Approval gate on changes before production | Explanation and review of contested decisions |

How the two layers work together on a Building Platform

Keeping the layers separate is not a constraint you tolerate; it is the design that lets you move fast without losing control. It only works, though, on a foundation that can host both cleanly — which is the role of the Building Platform underneath timveroOS.

On that platform the division of labour is explicit. timveroAI works at build-time, compressing the assembly and change of the lending product. The explainable scoring engine works at run-time, producing deterministic, auditable credit decisions. A human stays in the loop on both — approving system changes on one layer, reviewing contested decisions on the other. Speed comes from the agent that builds; trust comes from the engine that decides; neither borrows the other’s job.

“The temptation is to point one clever model at the whole problem. We deliberately don’t. The agent that helps you build and change the system is a different thing from the logic that approves a loan — and the moment you blur them, you’ve either slowed your product team down or handed a regulator a decision you can’t explain. Speed belongs in the build. The decision stays deterministic.”

— Dmitriy Wolkenstein, CEO, TIMVERO

The proof that the split holds up in production is in the speed it unlocks without softening the decision. At European fintech Finom, timveroOS underpinned a banking-grade lending operation that reached 98% process automation and launched in four months — a build-time pace the implementation layer makes possible, on a system whose credit decisions stay deterministic and explainable (Finom case study (opens in new tab)).

“What impressed me most was their ability to work at our pace, absorbing requirements on the fly, proposing solutions proactively, and adapting as our needs evolved. Today, we’re running proactive credit campaigns and sophisticated servicing operations on a single platform. timveroOS delivered a competitive advantage under impossible deadlines.”

— Alex Goncharenko, Head of Credit, Finom

The shape of the advantage is the same one running through this whole series. For an incumbent, the two-layer model is how you adopt AI without surrendering auditability — the regulators’ favourite question, “explain this decision,” still has an answer. For a digital lender, it is how you launch and re-launch products at speed while the credit decision stays defensible. Either way, the formula holds: AI for speed, deterministic logic for the decision. How the build layer changes a live system safely — shadow-run mode — and how its decisions stay grounded rather than hallucinated are distinctions worth their own articles, and we will take them next. Lenders weighing where each layer fits can start with the platform view for banks (opens in new tab) or fintechs (opens in new tab).

Frequently asked questions

What is the difference between an AI agent and a credit scoring model in lending?

A credit scoring model is a run-time tool: it evaluates a borrower’s risk to inform a decision. An AI implementation agent is a build-time tool: it helps assemble and change the lending system itself. One acts on every application; the other acts while you are building the product. They are different products under different controls.

Does an implementation agent like timveroAI make credit decisions?

No. timveroAI is a build-time implementation agent — it assembles and configures the lending system within a pre-validated framework: entities, products, policies and integrations. The credit decision is made at run-time by a separate, explainable scoring engine that produces deterministic outcomes with reason codes. The two are intentionally kept apart.

Can an AI agent approve loans on its own?

It should not approve loans without a human-reviewable, explainable basis. Under ECOA a lender must give specific reasons for denial, and the CFPB has stated that algorithmic complexity is no excuse. A fully autonomous “black box” approval creates compliance and fair-lending exposure, which is why the decision layer stays deterministic and supervised.

Is AI credit scoring regulated?

Yes. In the US, AI credit models fall under the Federal Reserve’s SR 11–7 model risk guidance and ECOA adverse-action requirements. In the EU, creditworthiness assessment is classified as high-risk under the AI Act (Annex III, point 5(b)), with obligations applying from August 2026, and credit scoring is treated as an automated decision under GDPR Article 22.

What is explainable AI in credit decisioning?

Explainable AI in credit decisioning means the system can produce the specific reasons behind each approval, decline or price — not just an opaque score. It lets a model-risk team validate the logic and a lender satisfy adverse-action requirements, which is why explainability is a baseline requirement for the decision layer, not an optional feature.

How can a lender use AI to build a system without it touching credit decisions?

By separating the layers. A build-time implementation agent works on entities, products, policies and integrations, with shadow testing and human approval before changes go live. The run-time decision is handled by a distinct, deterministic scoring engine. The agent builds the system; it never issues the credit decision.

See both layers on one platform

If your “AI strategy” is really two strategies — one for building faster, one for deciding safely — it helps to see them running on a single foundation, cleanly separated. That is what the Building Platform underneath timveroOS is built to do.

-rsbxq-400x250.webp)

CEO at TIMVERO

Dmitriy Wolkenstein is the CEO of TIMVERO, leading the team building timveroOS and timveroAI. He writes about why the next generation of lending will be won at the infrastructure layer — and what it takes to get there.

LinkedinLatest News

Generative AI in Banking: Where It Works and Where It Can’t

The AI Banking Efficiency Gap: Why It Compounds and Who Wins

AI in Banking: A 2026 Guide to Value, Risk, and Scale

AI Hallucinations in Lending Software: How to Stop Them

The 2–3 Year Window: What Banks Lose by Waiting on AI

How AI Is Transforming Lending in 2026: Platforms, Automation, and What Actually Works

Fraud Prevention in Digital Lending: How AI Is Reshaping the Battle in 2025–2026

Best AI-Powered Lending Platforms in 2026: A Buyer’s Guide

How to Implement AI in Lending and Pass a Regulatory Audit