Best AI-Powered Lending Platforms in 2026: A Buyer’s Guide

In 2026, picking an AI lending platform is no longer a question of which vendor has the smartest credit model — it is a question of which architecture that AI sits inside. Banks and credit unions consistently say they want operational efficiency, cleaner integration with existing systems, a better digital experience, and the ability to launch new credit products without a multi-quarter implementation.

Most of today’s AI lending tools are point solutions — scoring in one system, document AI in another, decisioning somewhere else — and the integration glue between them has become the most expensive part of the stack. This guide compares the ten AI-powered lending platforms most often shortlisted by banks, credit unions, and fintech lenders, and explains why the timveroOS Building Platform sits in its own category: an AI-native lending architecture for institutions whose products do not fit a standard mold and who want fintech-speed launches without changing the business around the software.

What banks and credit unions actually want from AI lending in 2026

The surveys are unambiguous about buyer priorities, and almost none of them name “customization” as the headline want.

Operational efficiency is the top tech objective for the second year running. Bank Director’s 2025 Technology Survey (141 US FIs under $100B in assets) puts improving operational efficiency at the top for 65% of respondents, followed at distance by customer acquisition and retention at 25% (PCBB, 2025 (opens in new tab)). Jack Henry’s 2025 Strategy Benchmark of 149 C-level executives shows the same pattern: operational efficiency sits in the top three for both banks and credit unions (Jack Henry, 2025 (opens in new tab)).

Spend is climbing, scrutiny too. 71% of banks raised tech budgets in 2025, median $2.5MM — but only 18% track ROI on those investments. Boards now demand outcome-anchored selection criteria for any platform decision.

The right reading of the market is not that banks are searching for “AI customization.” They are searching for a platform that delivers efficiency, integration, digital uplift, and faster change — and AI is the mechanism, not the product. Buyers across the financial sector now expect measurable improvements, not just AI branding.

Why standard AI lending stacks keep falling short

If efficiency and integration are what buyers want, the next question is why so many AI lending projects under-deliver. The Bank Director survey is direct about it.

The most-cited technology challenge in 2025 was legacy-systems integration at 51%, with rising costs at 44%, ineffective data use at 33%, and obsolete technology requiring workarounds at 25%. 41% of institutions admit recent tech initiatives fell short of objectives — mainly due to insufficient vendor support, employee adoption, and longer-than-expected timelines (PCBB, 2025 (opens in new tab)).

Translated into the way buyers actually phrase it inside their organizations:

- “Our current system can’t fit how we actually work.”

- “Every change becomes a mini-project.”

- “We keep adding workarounds instead of fixing the platform.”

- “Integration with our core and our data is painful.”

- “The vendor cannot support our edge cases.”

- “We need digital speed without forcing the bank to change its business around the software.”

A platform that addresses these six sentences — and produces an auditable, regulator-defensible AI decision flow that supports regulatory compliance, a common gap across financial institutions and other financial organizations — is what the 2026 buyer is shopping for. A vendor that leads with “highly customizable” without translating to those outcomes is selling a mechanism, not a result.

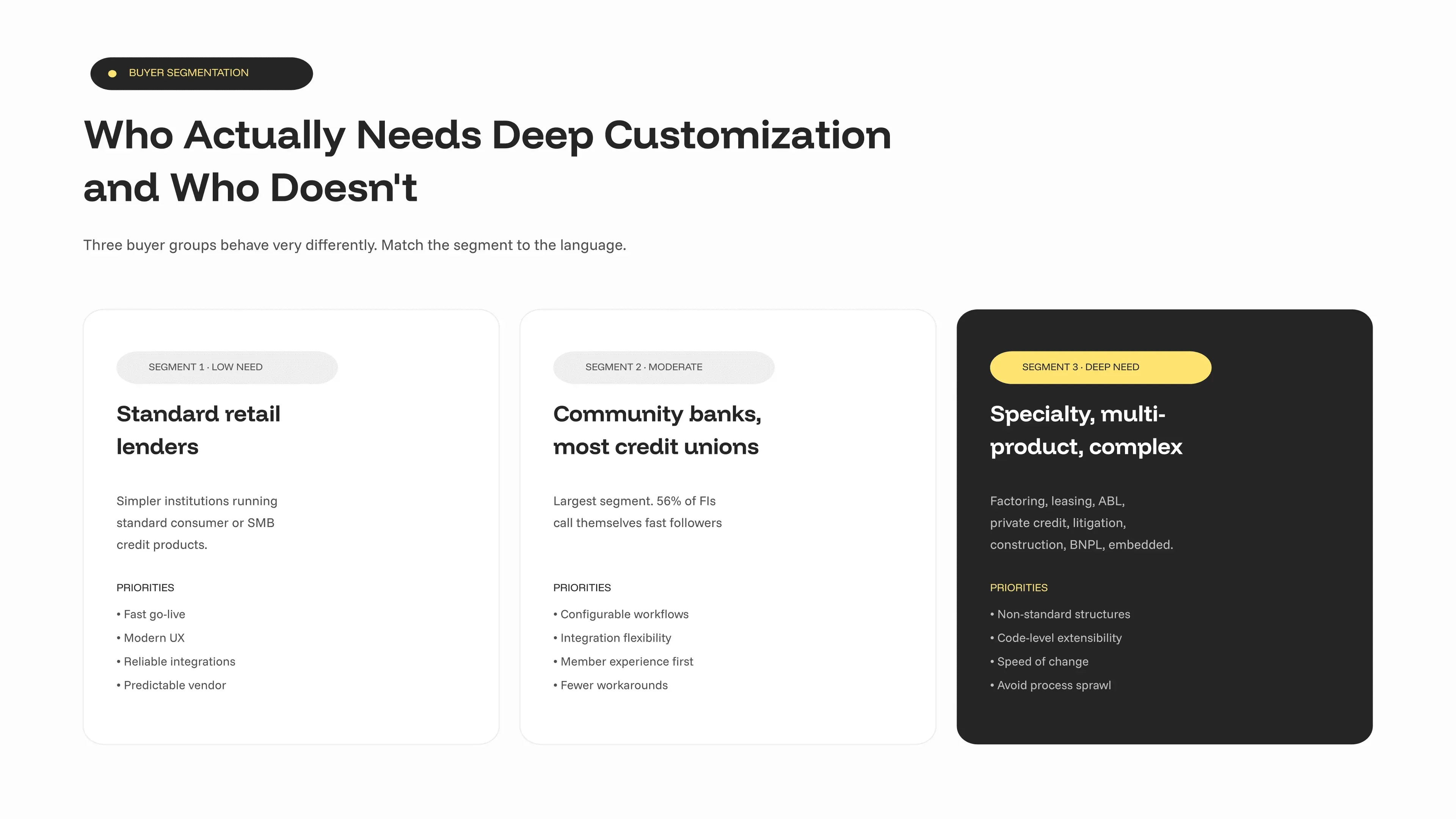

Who actually needs a deeply customizable AI lending platform — and who doesn’t

Not every institution should buy the same thing. Three buyer groups behave very differently.

Standard retail lenders — out-of-the-box may be enough

Simpler institutions running mostly standard consumer or SMB credit do well with strong SaaS plus one or two specialty AI vendors. They care about fast go-live, low implementation burden, modern UX, reliable integrations, and a predictable vendor relationship. For this segment, leading with “deep customization” backfires — it sounds like complexity, long decision cycles, and a heavy implementation team.

Community banks, regional lenders, and most credit unions — moderate flexibility

The middle segment is the largest in the US market and the most often misread. Many credit unions (opens in new tab)and community banks describe themselves as “fast followers” — Bank Director’s 2025 survey finds 56% of FIs use exactly that label, only 12% call themselves innovators. What they need is configurable workflows, integration flexibility, the ability to evolve products, room for policy exceptions, and support for both digital and human-in-the-loop processes. The right language is adaptability, future-proofing, fewer workarounds — not “architectural rebuild.” For credit unions specifically, member experience and operational efficiency should sit first, with configurability as the supporting layer.

Specialty, multi-product, and complex lenders — deep adaptability

This is where deep customization stops being a nice-to-have and starts being the only way to avoid process sprawl. Specialty lenders (factoring, leasing, asset-based, private credit, litigation finance, construction draws, BNPL), embedded-finance providers, and partner-led models, which often depend on digital lending workflows that standard SaaS cannot represent well, hit the same wall with standard SaaS: it demos cleanly, then breaks in production on a payment schedule, a covenant, or a participant model the vendor never planned for. For this segment, the right question is not “how customizable” but “how quickly can the platform evolve when the business does?” This is the segment timveroOS is built for first, with a deep understanding of bespoke lending workflows.

How we evaluated these platforms

We assessed thirty-plus AI lending platforms used by US, EU, and UK lenders across the financial services industry in 2025–2026, then narrowed to ten meeting a real production threshold — paying customers, observable case data, and a roadmap visible beyond the next funding round. Each was scored on seven criteria, weighted toward what buyers actually prioritize.

| Criterion | Weight | Buyer outcome serves |

|---|---|---|

| AI capability depth | 25% | Underwriting, document AI, decisioning, agentic orchestration |

| Integration & fit with existing systems | 20% | Closes the 51% legacy-integration gap |

| Compliance & explainability | 15% | FCRA, ECOA, Reg B/Z, BSA/AML, EU AI Act, SR 11–7, and alignment with current regulatory frameworks |

| Production maturity & vendor support | 15% | Closes the 56% “insufficient vendor support” gap |

| Speed of implementation & change | 10% | Closes the 41% “longer-than-expected timeline” gap |

| Architectural control | 10% | Configuration only vs. code-level access |

| Vendor lock-in risk | 5% | Model ownership, data export, exit terms |

TIMVERO appears in this guide because the Building Platform approach is structurally different from the point AI tools that fill the rest of the list — and our editorial position is disclosed openly, with the evaluation intended to reflect the broader financial services landscape.

The 10 best AI-powered lending platforms in 2026

We list timveroOS first because the Building Platform approach is a distinct category from the rest of the platforms in this guide. The other nine are listed inside the categories they best occupy, not ranked against each other. This category reflects how AI is reshaping the fintech industry and the wider fintech market.

. timveroOS — Best for institutions whose lending model doesn’t fit standard SaaS

timveroOS lets banks (opens in new tab), fintech companies (opens in new tab), and credit unions (opens in new tab) fit the loan management software (opens in new tab) to their operating model — automate more of the process, reduce workarounds, integrate cleanly with the core, and keep evolving products without replatforming. It is a Building Platform: a working lending system on day one, with code-level access through a Java/Spring Boot SDK to every entity, state machine, service, and integration. On top sits timveroAI (opens in new tab), an implementation agent trained exclusively on the timveroOS framework, which deploys, configures, and evolves the platform in shadow mode under human approval.

Best for: banks and credit unions that want operational efficiency, integration depth, and fintech-speed product launches without changing the business around the software; specialty and multi-product lenders whose structures no SaaS schema covers.

Key capabilities: SDK extensibility, timveroAI compressing 4–6 months into 3–6 weeks, explicit compliance building blocks (IFRS 9, CECL, audit trails, jurisdiction modules), self-hosted or private-cloud deployment, explainable AI scoring engine separate from timveroAI, shadow-run mode with human approval gates, and seamless integration with existing cores and data environments.

Strengths: the only platform on this list where AI lives inside the lending architecture rather than next to it, helping enable financial institutions to retain precise control over product logic and change management—multi-jurisdiction — $5.5B+ AUM across 13+ countries, 7,000+ daily loan applications in production.

Limitations: overkill for institutions running fully standard retail products — the value of code-level access shows up only when the roadmap demands non-standard structures.

Real-world use case: Finom (opens in new tab), a European EMI serving 200K+ SMB customers across five EU countries, launched a proactive credit-line product with dynamic limits — origination in four months, full servicing in three, 98% automation in production.

“What impressed me most was their ability to work at our pace, absorbing requirements on the fly, proposing solutions proactively, and adapting as our needs evolved. Today, we’re running proactive credit campaigns and sophisticated servicing operations on a single platform. timveroOS delivered a competitive advantage under impossible deadlines.”

— Alex Goncharenko, Head of Credit, Finom

2. Explainable AI underwriting — Zest AI

Zest AI applies ML to credit underwriting with explicit focus on explainability, including AI-driven credit scoring that generates reason codes mapping to adverse-action requirements. Most often deployed by US banks and credit unions, it expands approvals to thin-file applicants without raising loss rates, improving credit risk assessment for those borrowers.

Best for: US credit unions and community banks modernizing consumer underwriting.

Strengths: strong explainability; published fair-lending tooling; mature US compliance.

Limitations: point solution — underwriting only; no document, servicing, or orchestration.

3. Real-time multi-product decisioning — Provenir

Provenir runs real-time risk decisioning to help lenders manage credit risk in real time across consumer credit, BNPL, auto, and SMB lending with a visual workflow canvas. One of the few decisioning platforms designed from day one to operate across product types within a single lender.

Best for: multi-product lenders running consumer, SMB, and BNPL portfolios in parallel.

Strengths: product-agnostic canvas; broad bureau and alt-data integrations, where machine learning algorithms can analyze data from multiple sources inside the decisioning flow.

Limitations: decisioning layer only — origination, document, servicing come from elsewhere.

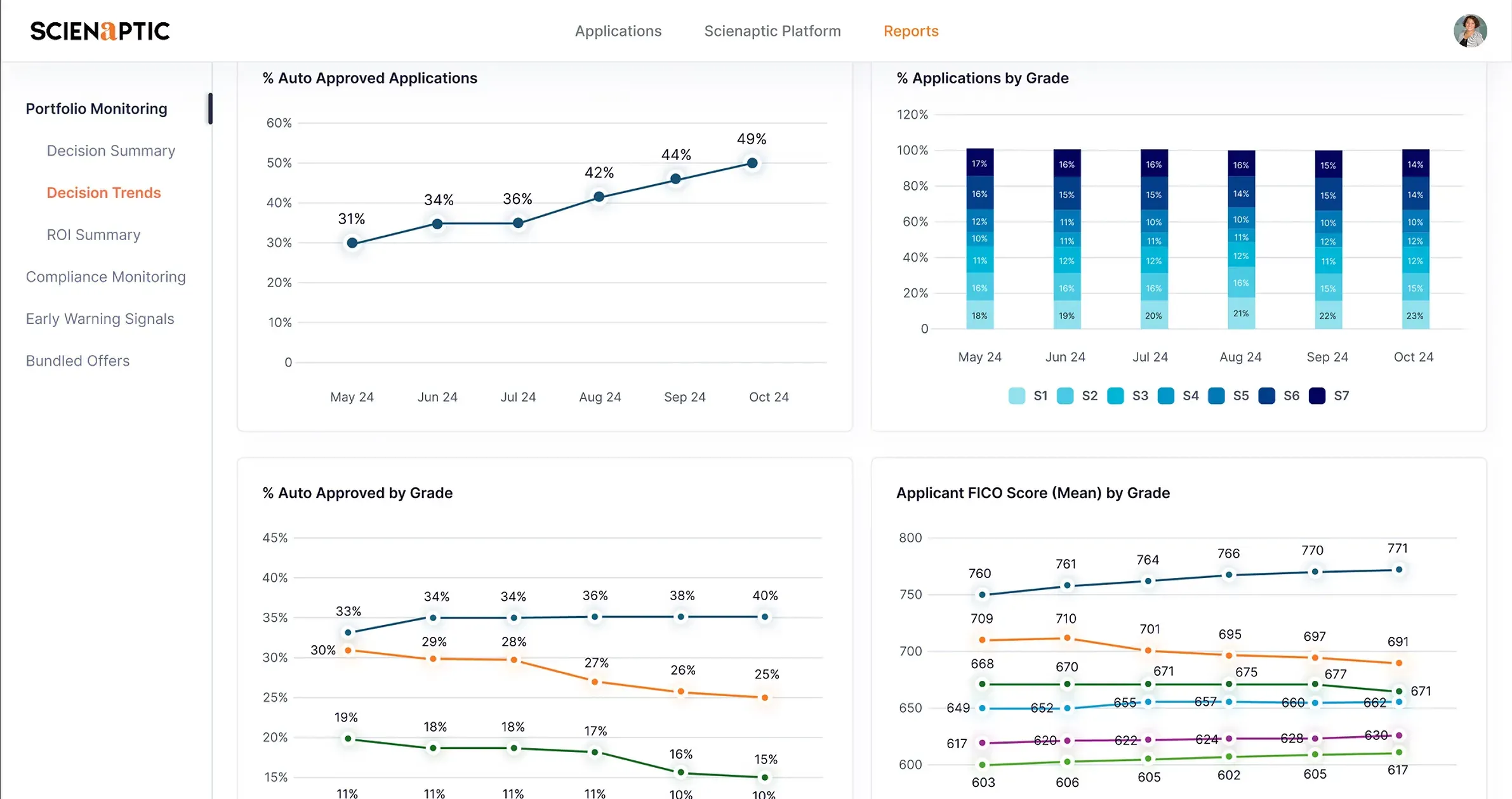

4. Mid-market AI credit decisioning — Scienaptic AI

Scienaptic specializes in real-time AI credit decisioning for mid-sized US banks and credit unions, using predictive analytics to support real-time decisioning and emphasizing quick deployment alongside existing cores. Public reporting includes automated decisioning rate shifts from 28% to 75% at mid-market CUs (Multimodal, 2026 (opens in new tab), gains banks can use to make more informed decisions at scale.

Best for: mid-market US banks and credit unions automating consumer decisioning.

Strengths: fast deployment alongside legacy LOS; named CU customer base.

Limitations: US-focused; not built for multi-jurisdiction or non-consumer.

5. Document AI with human verification — Ocrolus

Ocrolus combines AI document understanding with a human-in-the-loop verification layer for income, asset, and identity documents, supporting fraud detection when manipulation risk is high. Widely used where document manipulation risk is non-trivial.

Best for: mortgage and SMB lenders with high-stakes document verification needs.

Strengths: near-perfect accuracy on structured loan documents; integrated signals for fraud prevention.

Limitations: document layer only — feeds downstream systems, does not orchestrate.

6. Enterprise document intelligence — ABBYY Vantage

ABBYY Vantage is a configurable IDP platform with pre-trained models for common loan documents and the ability to train custom extractors. Chosen by commercial and cross-border lenders whose document mix includes contracts that no off-the-shelf model has seen.

Best for: commercial lenders with high-complexity, non-standard document types.

Strengths: trainable extractors for unusual documents; cloud or on-premise.

Limitations: document processing only; workflow and decisioning come from elsewhere.

7. Borrower-facing AI origination — Blend

Blend modernizes the front of the lending funnel for consumer and mortgage products, automating asset, income, and employment verification, including borrower data such as employment history, through direct primary-source connections with borrower consent.

Best for: mortgage and consumer lenders focused on borrower experience, customer experience, and completion.

Strengths: strong primary-source verification, which can also support customer satisfaction; deep integrations with major US LOS.

Limitations: point-of-sale layer only; no underwriting, servicing, or decisioning.

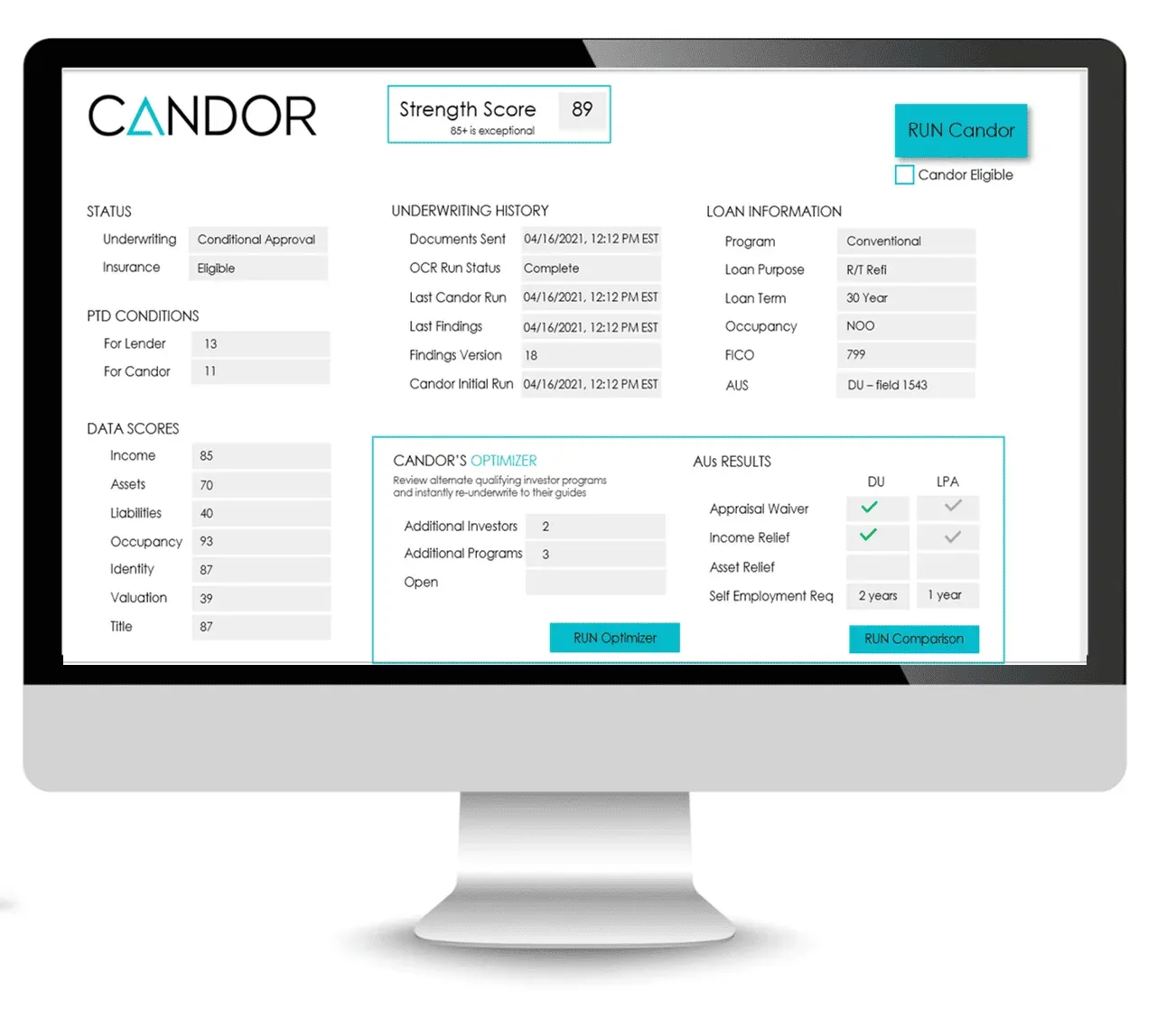

8. AI mortgage underwriting — Candor Technology

Candor automates underwriting decisions on conforming mortgages, generating credit and collateral conclusions with documented reasoning. Lenders report meaningful reductions in time-to-conditional-approval.

Best for: US mortgage lenders scaling conforming-loan origination.

Strengths: mortgage-specific automation; documented underwriting reasoning.

Limitations: mortgage-only; not built for consumer, SMB, or commercial.

9. Agentic AI for commercial lending — MightyBot

MightyBot positions itself as an agent platform for commercial and CRE lending, with ai agents handling repetitive commercial-lending tasks inside the stack and helping reduce human error in multi-step workflows, combining document intelligence, a policy engine, and FCRA/ECOA/Reg Z audit trails in one stack instead of stitching them across separate vendors.

Best for: commercial and CRE lenders consolidating point AI tools into one agentic platform.

Strengths: integrated policy engine and audit trails.

Limitations: commercial/CRE focus; less suited to consumer or multi-jurisdiction retail.

10. End-to-end SMB lending automation — TurnKey Lender

TurnKey Lender covers origination, decisioning, servicing, collections, and compliance automation for SMB lenders and alternative finance in one suite. Value proposition is breadth — most workflows handled inside one product rather than across integrations.

Best for: SMB and alternative finance lenders seeking suite breadth over architectural depth.

Strengths: end-to-end coverage; faster initial deployment than multi-vendor stacks, which can help reduce operational costs.

Limitations: SaaS configuration model — architectural changes depend on vendor roadmap.

Honorable mentions: Numerated (Moody’s) for SMB origination, Tavant for enterprise mortgage operations, AgentFlow from Multimodal for credit union AI automation, FundMore.ai for mortgage underwriting, Biz2X for SMB and SBA lending, Casca for AI-native SMB origination, Parlay for SBA readiness, and Fuse Finance for AI-native LOS replacement.

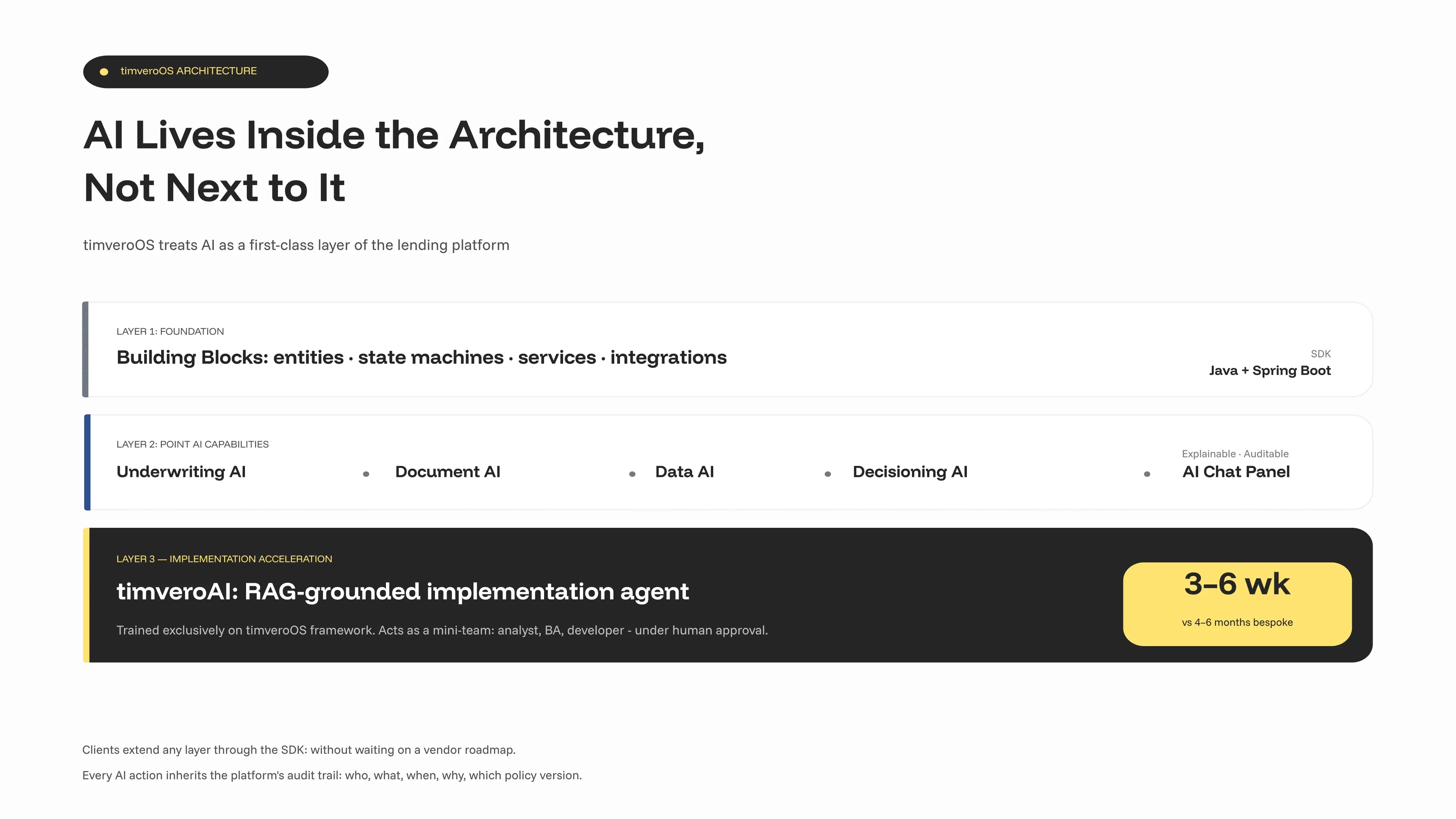

How timveroOS turns AI from a feature into the architecture

This is where the Building Platform diverges most sharply from the rest of the list. Most platforms in this guide treat AI as a feature plugged into an otherwise conventional lending core. timveroOS treats AI as a first-class layer of the architecture, with two distinct components: timveroAI as the implementation agent that ships and evolves the platform, and ai systems that sit inside the lending core itself, which matters across the financial industry, not just for one product line.

AI lives in the architectural layer, not next to it

A point AI vendor connects to a stable LOS through an API and acts on whatever data that LOS sends — the surface is fixed, rather than designed around scalable architecture. The Building Platform inverts that assumption: the lending core itself is composed of building blocks (entities, state machines, services, integrations) that a client engineering team can extend through the SDK. When a credit policy needs a new data signal, the policy is modified in code and deployed without a vendor change request. When a new product requires a non-standard payment schedule (litigation balloon, BNPL split, leasing residual, MCA factor rate), the schedule becomes a new building block. AI features deployed on top inherit the same surfaces — which is why explainability, audit, compliance, and data protection can be built in once, not glued on at every integration.

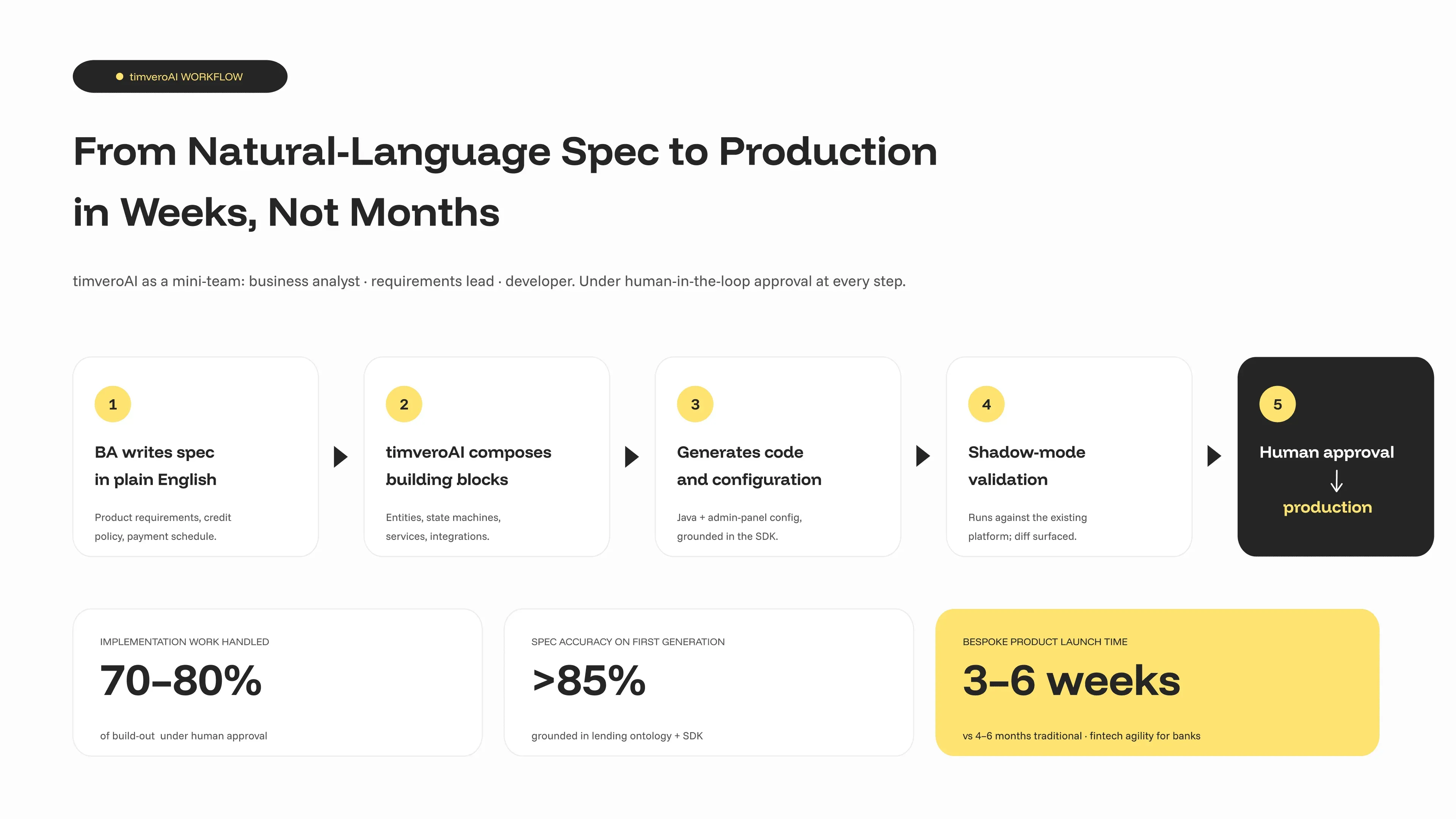

timveroAI is a mini-team that ships credit products

timveroAI (opens in new tab) is an implementation agent trained exclusively on the timveroOS framework, the lending ontology, and the skeleton library of pre-built blocks. It functions like a compressed product team — business analyst, requirements lead, and developer — operating against the SDK under human supervision. A BA writes a product specification in natural language, which advanced natural language processing helps interpret; timveroAI proposes the building-block composition, generates configuration and Java code, runs the proposal in shadow mode, and surfaces the changes for human approval. In production deployments the agent handles 70–80% of the implementation work, compresses 4–6 months of bespoke build-out into 3–6 weeks, and reaches >85% spec accuracy on first generation.

The outcome buyers care about: banks gain fintech-speed launches for new credit products without replacing the core or hiring a fintech-sized engineering team. That is what “fintech agility for banks” means in practice, and the added operational speed supports faster product launches.

Point AI capabilities the platform ships — and the ones clients add themselves

Because AI is a first-class layer, the platform ships point AI capabilities natively, and the same SDK surfaces let clients add their own without vendor lock-in.

- Underwriting AI — explainable credit scoring with reason codes mapped to adverse-action requirements; models retrained on the lender’s portfolio under SR 11–7-style governance.

- Document AI — built-in document management with classification, extraction, and signature workflows tied to the entity model, so extracted data lands in the right block with full audit history.

- Data AI — embedded BI dashboards (Apache Superset) and pattern surfacing that turn complex data into actionable insights for portfolio and exception monitoring, plus early-warning signals.

- Decisioning AI — hybrid policy-plus-ML logic where credit policy is expressed as code and ML applied transparently; every decision links to its policy version and source data.

- AI Chat Panel — an LLM-powered assistant embedded in editor pages with document upload, configurable providers, and the same audit trail as every other platform action, with support for customer interactions when configured for service workflows.

Clients add their own AI features — custom scoring, domain-specific classifiers, regional fraud signals — through the same SDK, without waiting on a vendor roadmap. When AI sits inside the architecture, the cost of adding the next AI feature drops by an order of magnitude.

Explainability and compliance are built in, not bolted on

Every AI action inherits the audit infrastructure that protects sensitive financial data in the lending core: who made the change, what the data looked like before and after, why it happened, and which policy version was active. Adverse-action reason codes are generated alongside the decision, not reconstructed afterwards. timveroAI changes run in shadow mode by default — proposing, validating, surfacing the diff — and ship only after human approval. A generic copilot writes code; timveroAI writes code grounded in the lending ontology, traceable to a policy version, and defensible to a regulator in support of responsible lending.

AI lending compliance baseline in 2026

Buyers should treat regulatory compliance as a first-order selection criterion, not a post-purchase audit task. The regulatory perimeter has shifted materially in the last twelve months.

United States. The CFPB requires specific, accurate adverse-action reasons regardless of model complexity (CFPB Circular 2023–03 (opens in new tab)). ECOA and Reg B prohibit disparate impact regardless of intent. Examiners now apply SR 11–7 model-risk expectations to AI/ML credit models (Federal Reserve, 2011 (opens in new tab)). FCRA covers any model output used in credit decisions; BSA/AML covers the fraud and onboarding layers, and lenders increasingly expect compliance automation in those controls.

European Union. EU AI Act high-risk obligations — risk management, data governance, data protection, technical documentation, human oversight, post-market monitoring — apply from August 2, 2026 (EU AI Act overview (opens in new tab)). Creditworthiness evaluation is named explicitly in Annex III as a high-risk use case.

United Kingdom. The FCA’s Consumer Duty applies to lending decisions, including those driven by AI, under an outcomes-based, principles-led approach (FCA Consumer Duty (opens in new tab)).

Three questions to ask every vendor: where does the audit trail live; how are model changes governed and validated; and what happens to the model — and its training data — if the contract ends.

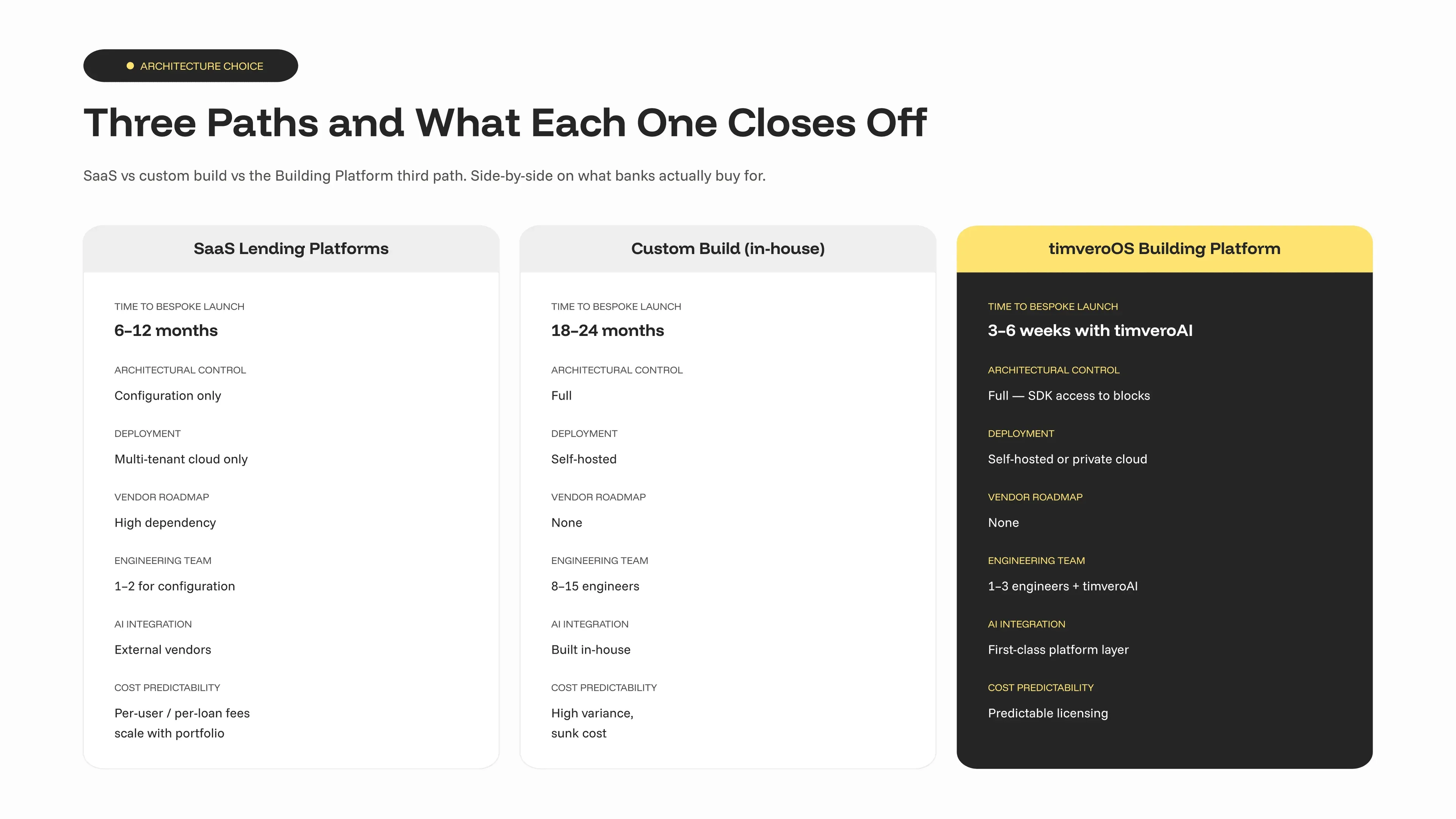

SaaS vs custom build vs Building Platform

The buying decision in 2026 is not “which AI vendor” — it is which architecture to commit to, because that choice affects operational costs over time. Three paths are now visible, and each closes a different set of future options.

| Criterion | SaaS lending platforms | Custom build (in-house) | timveroOS Building Platform |

|---|---|---|---|

| Time to launch a bespoke product | 6–12 months on the vendor roadmap | 18–24 months from scratch | 3–6 weeks with timveroAI |

| Integration with existing systems | Limited to vendor connectors | Build everything | SDK surfaces, code-level extensibility |

| Architectural control | Configuration only | Full | Full — SDK access to building blocks |

| Deployment | Multi-tenant cloud only | Self-hosted | Self-hosted or private cloud |

| Vendor roadmap dependency | High | None | None |

| Engineering team required | 1–2 for configuration | 8–15 engineers | 1–3 engineers plus timveroAI |

| Cost predictability | Per-user or per-loan fees scale with portfolio | High variance, sunk cost | Predictable licensing |

| Compliance modules | Opaque, vendor-controlled | Built from scratch | Explicit building blocks per jurisdiction |

| AI integration model | One or more external vendors | Build the AI stack in-house | AI as a first-class platform layer |

The Building Platform is the third path between SaaS and custom build (opens in new tab) — a working lending system on day one, with the architectural surface area custom-build buyers wanted and the readiness SaaS buyers were promised. That a Building Platform is also where the most ambitious AI capabilities can be deployed with full audit traceability is not a coincidence — it is the consequence of an architecture that exposes the right surfaces to the right tools.

Real outcomes that make the case

Three deployments on timveroOS demonstrate what the architecture produces — read through the outcomes buyers actually buy for, with measurable improvements in speed, cost, and launch execution.

Cartiga — a litigation finance lender — replaced Salesforce with timveroOS at ~10–12% of the original cost (efficiency), shipped its MVP in eight weeks (speed of change), and now manages $1.6B+ in deployed capital. The product — working capital for law firms collateralized by case proceeds, with non-standard amortization and a balloon without a fixed date — was a fit no SaaS could absorb.

“timveroOS has become the core engine behind our law firm lending business. Its framework allowed us to build sophisticated workflows, pricing, and collateral logic per our bespoke structures — something no SaaS or traditional LMS could offer.”

— Noah Cutler, Senior Vice President, Cartiga

AMIO Bank, a Tier-3 regional bank, launched a guarantor-supported consumer lending product as a four-month MVP after three prior attempts with two other vendors had failed (vendor support, timeline). The bank reports 8× faster time-to-yes and 60% lower cost-per-loan, gains that helped finance teams plan around lower process overhead, with two local payment rails (no REST APIs), earlier vendors had cited as blockers — handled by extending the platform’s integration building blocks.

Finom launched proactive credit lines for 200K+ SMB customers across five EU countries in four months at 98% automation in production — fintech-speed product launches inside an EMI-regulated environment.

What’s changing in AI lending in 2026–2027

Three shifts will drive most platform replacements over the next eighteen months.

Agentic AI moves from pilot to production. Multi-step, tool-using, evidence-collecting underwriting agents are now running against real loan packets at scale, increasingly using natural language processing to evaluate loan packets and supporting evidence. Lenders without an architecture that supports tool-using agents with auditable traces will be recoding their stack in 2027.

EU AI Act enforcement begins. The August 2, 2026, milestone makes the AI Act a buying criterion in real time. Platforms unable to produce technical documentation, risk-management evidence, and post-market monitoring data on demand will be removed from EU shortlists.

Alternative data becomes the underwriting default. Open-banking transaction data (CFPB §1033 Final Rule, 2024 (opens in new tab)), telco and utility signals, and verified employer feeds are now mainstream. Platforms must analyze transaction patterns and spending habits alongside other alternative data, and wider credit access depends on explaining these signals clearly. Platforms that cannot ingest, govern, and explain these signals at the policy level will lose ground.

Frequently Asked Questions

What is an AI-powered lending platform?

An AI-powered lending platform is software, widely used by financial institutions across the financial services industry, that applies machine learning and generative AI to the loan lifecycle — origination, document processing, underwriting, decisioning, servicing, compliance — and produces auditable decisions linked to source data, while supporting digital lending workflows. In 2026 the term covers point tools and full platforms; buyers should distinguish the two before shortlisting.

Do we actually need a deeply customizable AI lending platform?

Probably not, if your products are standard retail consumer or SMB credit — a strong SaaS plus a specialty AI vendor can be enough. You do need deeper adaptability if you run non-standard credit policy, multi-product portfolios, or specialty structures, or if integration with your core repeatedly produces workarounds.

How is timveroAI different from generic AI copilots and from explainable scoring tools?

timveroAI is an implementation agent trained exclusively on the timveroOS framework and lending ontology — letting non-technical users start from natural-language specifications, while it deploys, configures, and evolves the platform under human approval. The explainable AI scoring engine is a separate runtime component. A generic copilot writes code; timveroAI writes code grounded in the lending architecture and traceable to a policy version.

How does AI improve loan approval?

AI improves loan approval by analyzing many more borrower attributes than rules-based scoring, including employment history and transaction patterns, extracting data directly from source documents, applying credit policy consistently, and producing reason codes for adverse actions to strengthen credit risk assessment and broaden credit access. McKinsey reports 20–60% targeted operating-cost reductions when AI moves past pilot into production, which lenders use to make more informed decisions (McKinsey, 2024 (opens in new tab)).

Is AI lending compliant with FCRA and ECOA?

AI lending meets regulatory compliance expectations only when adverse-action notices state specific principal reasons, model risk management follows SR 11–7-style controls and aligns with applicable regulatory frameworks, and disparate-impact testing is documented. The CFPB has clarified that algorithmic complexity is not a defense for vague denial reasons (CFPB, 2023 (opens in new tab)

How long does it take to launch a new credit product on timveroOS?

Point AI vendors plug into existing systems in weeks but require integration work. Full SaaS replacements typically take 6–12 months. timveroOS with timveroAI has launched bespoke lending products in 3–6 weeks; standard consumer or SMB products even faster, which improves operational speed and can reduce operational costs.

Ready to Launch Your AI Lending Product Faster?

If your shortlist is a stack of point AI tools and a SaaS that almost fits, the architecture beneath is the decision worth scrutinizing — not which vendor’s underwriting model ranks highest this quarter. It is designed for fintech companies and other financial organizations that need a scalable architecture. A Building Platform briefing walks through how timveroOS and timveroAI compose into a working lending system that absorbs the AI capabilities described above, in your own environment, on a timeline your CFO will sign off on in the fast-moving fintech sector.

Head of Marketing

Ivan Halynkin leads Growth & Marketing at TIMVERO, the company behind timveroOS and timveroAI. He works across the seam between product and demand — translating composable lending infrastructure into positioning, content, and demos that resonate with banks, credit unions, and fintechs. His writing focuses on what actually moves the needle for digital lenders: origination economics, AI in credit decisioning, and the trade-offs between SaaS lending boxes and building-platform thinking.

LinkedinLatest News

Bank Efficiency Ratio: What It Is and How to Improve It

Embedded Lending for Vertical SaaS: Monetize & Own It

How U.S. Banks Should Rethink Credit Card Strategy in a Potential 10% APR Cap Environment

What Is Embedded Lending? How It Works and Why It Matters

Best Loan Origination Software in 2026: 10 Systems Compared

Lending Software Beyond SaaS vs Build: The Third Path

Open Banking Is Quietly Rewriting How Loans Work

Automated Loan Origination: How Lenders Cut Abandonment Rates and Speed Up Approvals

AI Agent vs Credit Scoring: The Two Layers of Lending AI