What Is Embedded Lending? How It Works and Why It Matters

Embedded lending is the integration of credit products — loans, lines of credit, point-of-sale financing — directly into the software, marketplace, or app a customer is already using, so they never have to leave to apply, get approved, or receive funds. It is the fastest-growing slice of embedded finance, and it is quietly redrawing where loans get originated. The question for most banks, fintechs, and software platforms is no longer whether to participate, but how — as a distributor of someone else’s credit, or as the owner of a lending product they control on a Building Platform like timveroOS.

This guide explains what embedded lending is, how the flow works end to end, who benefits, how the money is made, what the risks are, and how to stand up a program without spending 18 months building from scratch or surrendering your product to a rigid vendor. Wherever credit logic, compliance, and customer experience need to be yours, the architecture you choose matters more than the integration.

What Is Embedded Lending?

Embedded lending means a credit product is offered inside a non-lending context — at the checkout of an e-commerce store, inside an accounting or invoicing tool, on a B2B marketplace, or within a banking app — at the exact moment the borrower needs it. Instead of redirecting the customer to a separate lender, the platform presents an offer, captures the application, runs a decision, and disburses funds in the same workflow.

The mechanism that makes this possible is data. Because the host platform already holds rich, real-time signals — sales volume, invoices, transaction history, fulfilment rates — underwriting can use those signals instead of relying solely on traditional credit files. According to McKinsey (2024), this is precisely why embedded-finance volumes in Europe grew roughly three times as fast as directly distributed loans over the past decade.

Embedded lending vs embedded finance vs BNPL

These terms are often used interchangeably, which causes confusion. Embedded finance is the umbrella: any financial product — payments, insurance, banking, investment, or lending — delivered by a non-financial company inside its own experience. Embedded lending is the credit-specific subset of that umbrella.

Buy now, pay later (BNPL) is one product type within embedded lending, typically a short-term, point-of-sale installment plan. Other embedded lending products include revolving lines of credit, term loans, merchant cash advances, and invoice-based financing. In other words, BNPL is embedded lending, but embedded lending is much broader than BNPL. For a deeper look at one of these product types, see our guide to BNPL software (opens in new tab).

A definition you can reuse

Embedded lending is the practice of offering credit products inside a non-financial platform’s own workflow — at the point of need — using the platform’s data to power instant underwriting and funding. It turns software companies, marketplaces, and merchants into distribution channels (or owners) of lending products without forcing the customer to leave.

How Embedded Lending Works

Embedded lending looks seamless to the borrower, but underneath it is a coordinated flow between three parties and several systems. Understanding that flow is the first step in deciding how much of it you want to own.

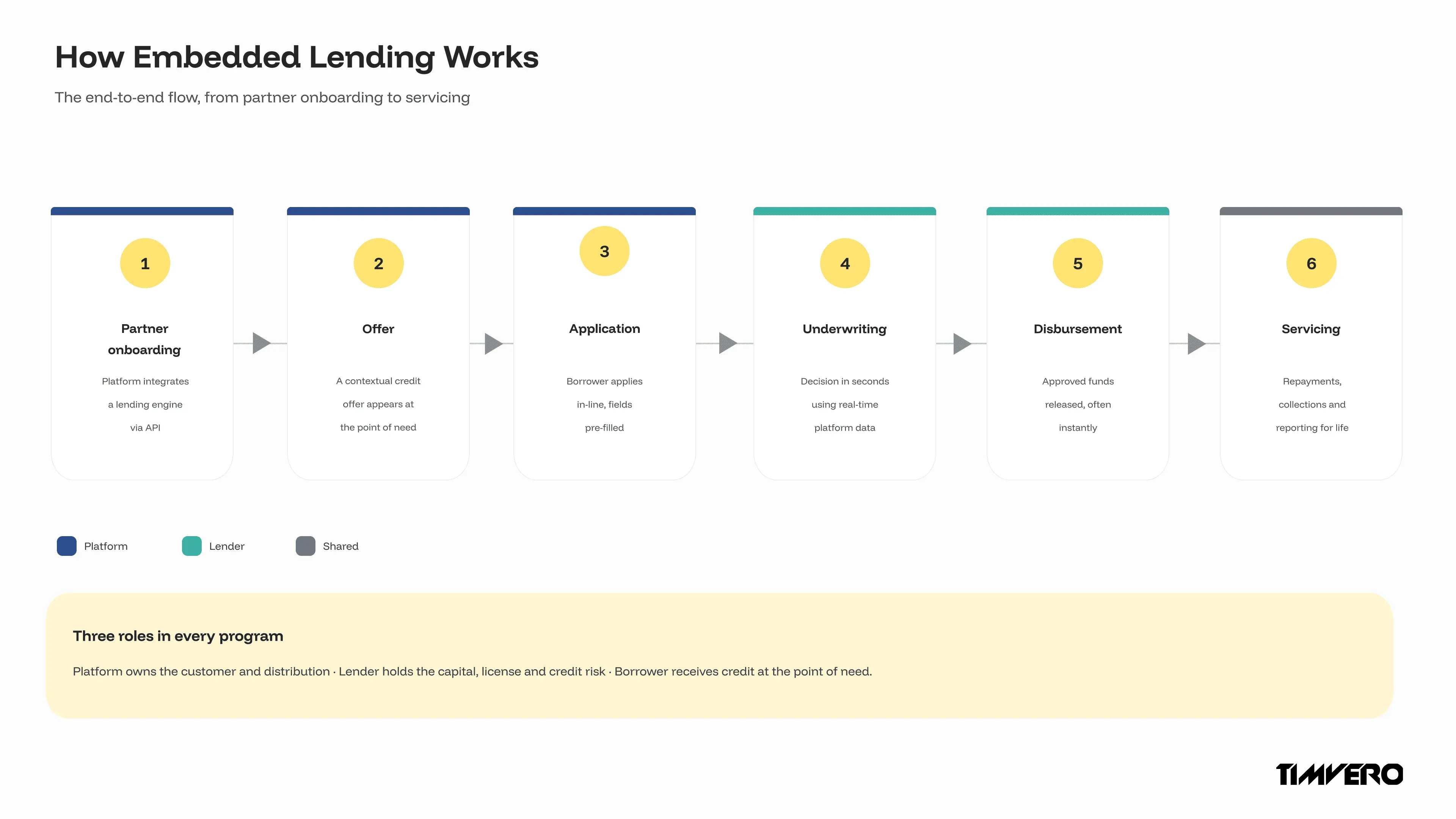

The end-to-end flow: from partner onboarding to servicing

A typical program moves through six stages. First, partner onboarding: the platform integrates with a lending system, usually through APIs, and configures the products it will offer. Second, offer presentation: eligible customers see a contextual credit offer inside the platform. Third, application: the borrower applies in-line, with most fields pre-filled from existing platform data.

Fourth, underwriting and decisioning: the lending engine evaluates the application using both traditional data and the platform’s real-time signals, returning a decision in seconds. Fifth, disbursement: approved funds are released, often instantly. Sixth — and most underrated — servicing: repayments, restructuring, collections, and reporting run for the entire life of the loan. Origination gets the attention, but servicing is where most of the operational complexity and cost live, which is why a strong loan servicing software (opens in new tab) layer matters as much as origination.

The three roles: platform, lender, borrower

Every embedded lending program has three roles. The platform (or merchant, or marketplace) owns the customer relationship and the distribution surface. The lender holds the capital, the credit license, and the regulatory obligations. The borrower is the end customer who receives credit at the point of need.

The strategic decision is how these roles map onto your business. You can be the platform and let a third party be the lender, or you can be both — owning the customer experience and the credit product on infrastructure you control. That choice determines your economics, your compliance exposure, and how much of the product you can shape. We return to it in the build-buy-embed section below.

Who Benefits — and Why Now

Embedded lending is not a niche convenience feature. It changes unit economics for the platform, opens a new distribution channel for the lender, and removes friction for the borrower. That three-way benefit is what is driving the growth curve.

Vertical SaaS, marketplaces, and B2B platforms

For software platforms — especially vertical SaaS serving a single industry — embedded lending is a revenue and retention lever. These platforms sit on industry-specific data (payments, invoicing, inventory, usage) that makes underwriting sharper than a generic credit pull. Offering credit at the point of need deepens engagement: borrowers interact with the platform more often during repayment, which improves retention.

It also diversifies revenue beyond subscriptions. Because monetizing a vertical SaaS platform with embedded lending is its own deep topic — covering revenue share, fees, net interest margin, and ROI — we cover it in a dedicated guide on embedded lending for vertical SaaS. The short version: credit can become one of the highest-margin lines a platform offers.

Banks and lenders as the credit provider

For banks, credit unions, and specialty lenders, embedded channels are a customer-acquisition engine. McKinsey (2024) found that in one major European market, the cost of acquiring a qualified SME lending lead through an embedded-finance channel was 15 to 20 times lower than a traditional lead. That is a structural advantage in a business where acquisition cost often determines profitability.

This is why lenders increasingly want to be more than a balance sheet behind someone else’s app. Owning the product — the pricing, the workflows, the servicing logic — lets a lender capture margin and data rather than renting distribution. Whether you serve banks, fintechs, or member-owned institutions, the same architecture question applies; our pages on lending software for banks (opens in new tab) and lending software for fintechs (opens in new tab) outline the ICP-specific angles.

Market trajectory: why now

The timing is not arbitrary. Three forces converged: APIs made integration cheap, real-time data made instant underwriting possible at near-zero marginal cost, and customers came to expect credit at the point of need. McKinsey (2024) projects that by 2030, embedded finance could account for 10 to 15 percent of banking revenue pools in Europe and 20 to 25 percent of retail and SME lending revenues, up from 5 to 10 percent today.

Market-sizing estimates vary widely by methodology, but all point the same direction: steep growth. Grand View Research (2024) sizes the broader global embedded finance market at USD 588 billion by 2030 (32.8% CAGR), with lending as one of its fastest-expanding segments.

Embedded Lending Business Models and Monetization

Embedded lending only matters if it pays. The revenue mechanics depend on how much of the value chain you own — which is the same axis as the control-versus-convenience trade-off.

Revenue models

There are four common ways to monetize an embedded lending program. Revenue share: the platform earns a cut of interest or fees generated by a partner lender. Per-transaction or referral fees: the platform is paid for each funded loan it originates. Net interest margin (NIM): when the platform or lender holds the loan on its own balance sheet, it captures the full spread between funding cost and lending rate. Retention and lifetime value: harder to put on an invoice, but real — embedded credit deepens engagement and reduces churn.

The pattern is simple: the more of the product you own, the more economics you capture — and the more capability and compliance you take on. That trade-off is the whole game.

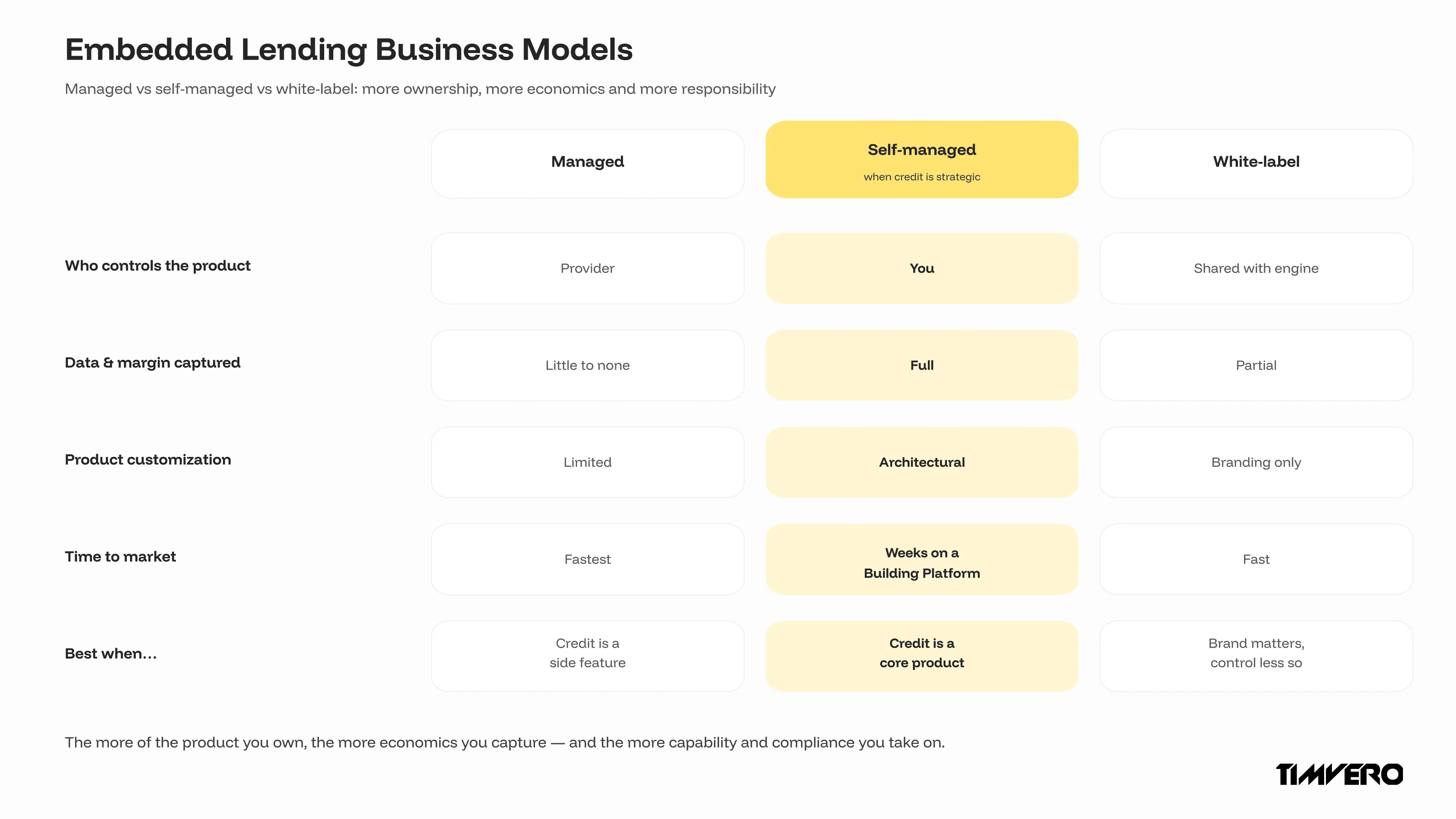

Managed vs self-managed vs white-label

Programs fall into three operating models. In a managed program, a provider runs the lending, the credit terms, and the capital; the platform is purely a distribution channel with little control over data, pricing, or margin. In a self-managed program, the platform (or lender) configures and operates the lending product itself, keeping control of logic, data, and economics. A white-label program sits in between: a branded experience on top of someone else’s engine.

Choosing among them depends on how strategic credit is to your business. If lending is a side feature, managed is fastest. If lending is — or will become — a core product with non-standard structures, self-managed on infrastructure you control is the only model that won’t cap you later. That decision leads directly into build, buy, or embed.

Build, Buy, or Embed: How to Stand Up an Embedded Lending Program

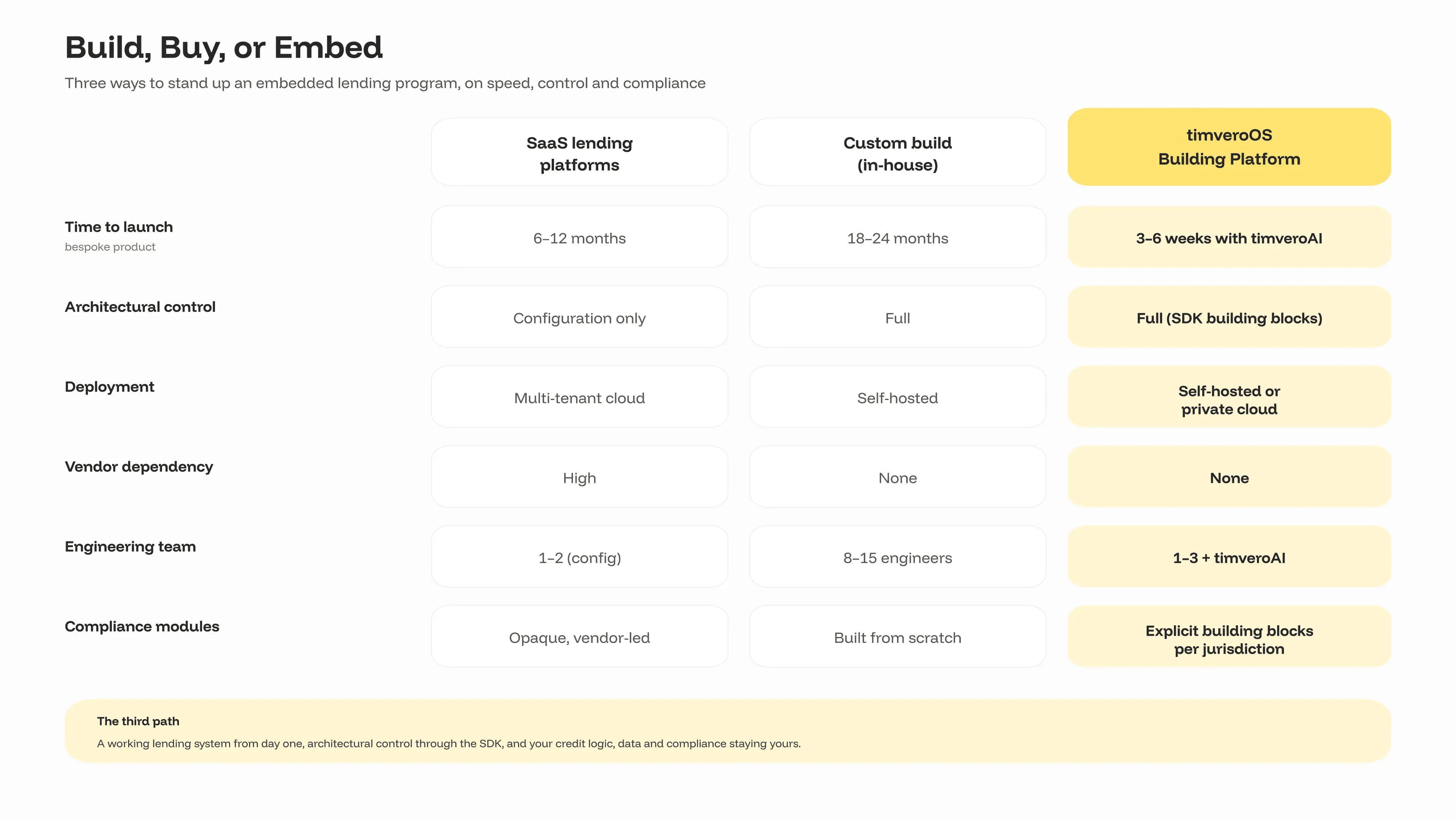

Once a platform or lender decides credit is strategic, it faces the same fork that every lending product faces: buy a SaaS solution, build from scratch, or take a third path. Each has a distinct cost, speed, and control profile.

| Criterion | SaaS lending platforms | Custom build (in-house) | timveroOS Building Platform |

|---|---|---|---|

| Time to launch (bespoke product) | 6–12 months on vendor roadmap | 18–24 months from scratch | 3–6 weeks with timveroAI |

| Architectural control | Configuration only | Full | Full (SDK access to building blocks) |

| Deployment | Multi-tenant cloud only | Self-hosted | Self-hosted or private cloud |

| Vendor roadmap dependency | High | None | None |

| Engineering team required | 1–2 (config) | 8–15 engineers | 1–3 engineers + timveroAI |

| Cost predictability | Per-user / per-loan fees scale with portfolio | High variance, sunk cost | Predictable licensing |

| Compliance modules | Opaque, vendor-controlled | Built from scratch | Explicit building blocks per jurisdiction |

Why SaaS hits a ceiling

SaaS lending products get you live quickly, but they trade speed for control. You configure what the vendor exposes and nothing more. The moment your embedded product needs a non-standard structure — a dynamic credit line, a marketplace-specific repayment schedule, a co-borrower flow — you hit an architectural ceiling and join a vendor roadmap queue measured in quarters. For a credit product meant to differentiate your platform, configuration-only is a hard limit.

Why custom build is too slow

Building from scratch removes the ceiling but reintroduces cost and risk. A ground-up lending system means 18–24 months, an engineering team of eight to fifteen, and the obligation to build origination, servicing, accounting, and compliance modules before originating a single loan. For most platforms and lenders, that time-to-market is incompatible with the opportunity window embedded lending is opening right now.

The third path: a Building Platform

There is a third path between renting a rigid SaaS product and building for two years. A Building Platform like timveroOS ships a working lending system from day one — origination, servicing, accounting, analytics — while giving your engineers code-level access to the underlying building blocks through an SDK (Java/Spring Boot). You start from a running system and shape it at the architectural level, rather than configuring within a vendor’s limits or assembling everything yourself.

This is the same model TIMVERO has argued for across the lending stack; we lay out the full case in our analysis of the third path beyond SaaS vs build (opens in new tab). For embedded lending specifically, it means the credit product, its data, and its compliance logic stay yours.

“Most embedded lending offers ask you to choose between speed and ownership — rent a rigid product fast, or spend two years building one you control. A Building Platform removes that choice. You launch a working lending product in weeks and still own the credit logic, the data, and the compliance, because you’re shaping building blocks at the architectural level, not configuring around someone else’s limits.”

— Dmitriy Wolkenstein, CEO, TIMVERO

Risks, Licensing, and Compliance

Embedded lending puts credit in front of more people, faster — which raises the stakes on getting risk and compliance right. Two questions decide most of the exposure.

Who holds the license and the credit risk

In a partner (managed) model, a platform can offer regulated credit without holding a lending license itself: the partner lender is the licensed institution and carries the regulatory obligations, while the platform supplies the experience and distribution. That lowers the barrier to entry — but it also means you don’t control the credit product, the data, or the margin.

In a self-managed or balance-sheet model, the platform or lender holds the license and the credit risk, and captures the corresponding economics and control. There is no universally correct answer; the right structure depends on whether credit is a convenience feature or a strategic product. What matters is making the choice deliberately, with eyes open to the compliance load each model carries.

Compliance as building blocks

However you structure licensing, the lending product must satisfy real obligations — IFRS 9 and CECL provisioning, audit trails, KYC/AML, and jurisdiction-specific regulatory reporting. On many platforms these are opaque, bundled into a vendor’s black box. On a Building Platform, compliance is implemented as explicit, modifiable building blocks per jurisdiction — so an auditor can see how a rule is applied, and your team can adapt it when regulations change. For embedded programs that span multiple markets, that transparency is the difference between scaling and stalling. (For the adjacent obligations, see our guidance on KYC and AML compliance for digital lenders (opens in new tab).)

How to Launch Fast Without Losing Control

The recurring objection to owning your embedded lending product is time. Building credit infrastructure sounds like the 18–24-month route. On a Building Platform, it isn’t — because most of the work is already done, and an implementation agent compresses the rest.

timveroAI is a RAG-grounded implementation agent: it is grounded in the Building Platform’s source code, lending ontology, and skeleton library, and it generates the specs, configurations, and code that adapt the platform to your product. It handles 70–80 percent of implementation work, while engineers keep human-in-the-loop approval. Critically, timveroAI-generated changes run in shadow-run mode — validated against real flows before going live — so speed never comes at the cost of control. (timveroAI is an implementation accelerator; it is distinct from the explainable AI scoring engine that makes runtime credit decisions — the two are separate building blocks.) You can see the agent in depth in our timveroAI overview (opens in new tab).

The result shows up in real deployments. With timveroAI, bespoke lending launches that traditionally take four to six months compress to three to six weeks. Finom, a European financial platform serving 200,000+ customers across five EU markets, used timveroOS loan management (opens in new tab) to launch a proactive embedded SME credit line — reaching banking-grade origination in four months, full servicing in three, and 98 percent process automation, with ROI from day one.

“What impressed me most was their ability to work at our pace, absorbing requirements on the fly, proposing solutions proactively, and adapting as our needs evolved. Today, we’re running proactive credit campaigns and sophisticated servicing operations on a single platform. timveroOS delivered a competitive advantage under impossible deadlines.”

— Alex Goncharenko, Head of Credit, Finom

Across its client base, the platform supports $5.5B+ in assets under management, 13+ countries, and 7,000+ daily loan applications — evidence that an owned, embedded credit product can run at scale. Read the full Finom case study (opens in new tab) for the implementation detail.

Frequently Asked Questions

What is embedded lending?

Embedded lending is the integration of credit products — loans, lines of credit, or point-of-sale financing — directly into a non-financial platform’s workflow. Customers apply, get approved, and receive funds without leaving the app or marketplace they’re already using, with underwriting powered by the platform’s own real-time data.

What is the difference between embedded lending and embedded?

Embedded finance is the umbrella term for any financial product — payments, insurance, banking, or lending — offered by a non-financial company inside its own experience. Embedded lending is the credit-specific subset: only the loan and credit products. BNPL is one type of embedded lending, not the whole category.

How does embedded lending work?

A platform integrates a lending engine, usually via API, and presents credit offers at the point of need. The borrower applies in-line, the engine underwrites using traditional plus real-time platform data, and approved funds are disbursed — often in seconds. Servicing, repayments, and reporting then run for the life of the loan.

How do platforms make money from embedded lending?

Four models dominate: revenue share on a partner lender’s interest and fees, per-transaction or referral fees per funded loan, net interest margin when the loan sits on your own balance sheet, and indirect gains from higher retention and lifetime value. The more of the product you own, the more economics you capture.

Who holds the credit license and the risk in an embedded lending program?

It depends on the model. In a managed or partner program, the licensed lender holds the license and credit risk, and the platform is a distribution channel. In a self-managed or balance-sheet program, the platform or lender holds the license and risk itself — and captures the corresponding margin, data, and control.

How long does it take to launch an embedded lending product?

With a rigid SaaS product, a bespoke launch can take 6–12 months on a vendor roadmap; a ground-up build takes 18–24 months. On a Building Platform like timveroOS, bespoke launches compress to 3–6 weeks with timveroAI. Finom reached banking-grade origination in four months and full servicing in three.

Ready to Launch an Embedded Lending Product You Actually Own?

Embedded lending rewards the platforms and lenders that control their credit product, not just the ones that rent distribution. See how timveroOS can stand up your embedded program in weeks, with the architecture, compliance, and data staying yours.

Head of Marketing

Ivan Halynkin leads Growth & Marketing at TIMVERO, the company behind timveroOS and timveroAI. He works across the seam between product and demand — translating composable lending infrastructure into positioning, content, and demos that resonate with banks, credit unions, and fintechs. His writing focuses on what actually moves the needle for digital lenders: origination economics, AI in credit decisioning, and the trade-offs between SaaS lending boxes and building-platform thinking.

LinkedinLatest News

Bank Efficiency Ratio: What It Is and How to Improve It

Embedded Lending for Vertical SaaS: Monetize & Own It

Best Loan Origination Software in 2026: 10 Systems Compared

Best AI-Powered Lending Platforms in 2026: A Buyer’s Guide

Lending Software Beyond SaaS vs Build: The Third Path

How U.S. Banks Should Rethink Credit Card Strategy in a Potential 10% APR Cap Environment

Open Banking Is Quietly Rewriting How Loans Work

Automated Loan Origination: How Lenders Cut Abandonment Rates and Speed Up Approvals

Generative AI in Banking: Where It Works and Where It Can’t