Best Loan Origination Software in 2026: 10 Systems Compared

If you search “best loan origination software,” you get dozens of lists that rarely agree, and for a structural reason. The market is crowded with very different products that all call themselves a loan origination system (LOS). Some are mortgage-only platforms. Some are decisioning engines. Some are front-end application builders. Others are full-lifecycle systems that take a loan from application through servicing.

They solve different problems, yet compete for the same search result. This guide compares 10 loan origination software vendors shaping the market in 2026, scored against eight criteria that actually predict fit. We start with timveroOS, a complete loan management platform (opens in new tab) built on a Building Platform, the third path between rigid SaaS and a custom build because we built it. But the goal is to help you choose well, even if that choice isn’t us. Every vendor below gets an honest treatment: what it’s good at, and where it falls short.

How We Evaluated These Loan Origination Systems

We assessed each platform the way a buyer should — across the dimensions that decide total cost and speed over a five-year horizon, not a feature checklist.

Eight evaluation criteria

- Product scope — origination-only versus full lifecycle (origination, servicing, collections, analytics).

- Architecture and configurability — how much you can change, and whether change requires the vendor.

- Speed of change — how fast a business team can launch a product or adjust a rule once the system is live.

- Integration depth — APIs and prebuilt connectors to credit bureaus, verification, pricing and core banking.

- Compliance and model governance — TRID, HMDA, RESPA, IFRS 9/CECL, SR 11–7 and EU AI Act readiness.

- Deployment — cloud, on-premise, hybrid, and who owns the data.

- Target segment — banks, credit unions, fintechs, mortgage, specialty and commercial.

- Proven scalability — real volume, not marketing claims.

Data sources

Our inputs were public customer reviews on G2, Capterra and Gartner Peer Insights, published case studies, vendor documentation, and regulator publications for the compliance criteria.

Bias disclosure

TIMVERO publishes this comparison and includes its own platform, timveroOS, at number one. We’ve stated our criteria openly so you can re-weight them for your own situation — and we describe every other vendor on its own merits.

What to Look for in Loan Origination Software

Before comparing vendors, get clear on the capabilities that matter. A modern loan origination system should cover most of the following:

- Application intake — digital, multi-channel applications that capture borrower data with minimal manual entry and validate it automatically.

- Credit scoring and underwriting — integration with credit bureaus and the ability to assess risk consistently, through rules, models, or both, with explainable, reproducible logic.

- Compliance tooling — built-in support for the regulations that apply to you (TRID, HMDA, RESPA for mortgage; IFRS 9 provisioning and audit trails for institutional lenders), with reporting that holds up to examination.

- Document management — secure capture, storage, e-signature, and tracking across the loan file.

- Integrations — connectivity to bureaus, appraisal and title vendors, income and asset verification, pricing engines, and your core system.

- Reporting and analytics — pipeline visibility, portfolio insight, and the data you need to manage risk and performance.

For mortgage lenders, add closing and funding workflows and investor delivery. The capability most buyers underrate is speed of change: once the system is live, how fast can your own team adjust a rule or launch a product — and who has to be involved? Hold that question as you read the list.

The 10 Best Loan Origination Systems at a Glance

| Vendor | Best for | Deployment | Target segment | AI layer | Pricing model |

|---|---|---|---|---|---|

| timveroOS | Business-led change & fast iteration | Cloud / on-prem / hybrid | Banks, fintechs, CUs, specialty | timveroAI implementation agent + explainable scoring | Portfolio-tiered licensing |

| Encompass | Mortgage at industry-standard scale | Cloud | Mortgage lenders, banks, IMBs | Add-on tooling | Enterprise / quote |

| nCino | Salesforce-native banks | Cloud (Salesforce) | Banks, commercial, SMB | Salesforce AI ecosystem | Enterprise / quote |

| MeridianLink | Credit unions & community banks | Cloud | CUs, community banks | Decisioning add-ons | Quote |

| Finastra | Large banks needing a broad suite | Cloud | Large/global banks, CUs | Suite-level tooling | Enterprise / quote |

| TurnKey Lender | Automated, AI-driven decisioning | Cloud | Non-bank lenders, fintechs | AI credit decisioning | Quote |

| DigiFi | API-first embedded lending | Cloud / API | Fintechs, embedded finance | AI decisioning components | Quote |

| LendingPad | Cloud-native mortgage origination | Cloud | Mortgage lenders, brokers | Limited | From ~$50/user/mo |

| Blend | Front-end borrower experience | Cloud | Mortgage & consumer front ends | Borrower-facing tooling | Quote |

| Abrigo | Community banks, commercial + risk | Cloud | Community banks, CUs | Risk analytics | Quote |

AI capabilities differ in kind, not just degree. Some platforms apply AI to the credit decision; others, like timveroOS, also apply it to building and maintaining the system itself. We unpack that distinction below — and it matters more than any single feature.

The 10 Best Loan Origination Systems in 2026

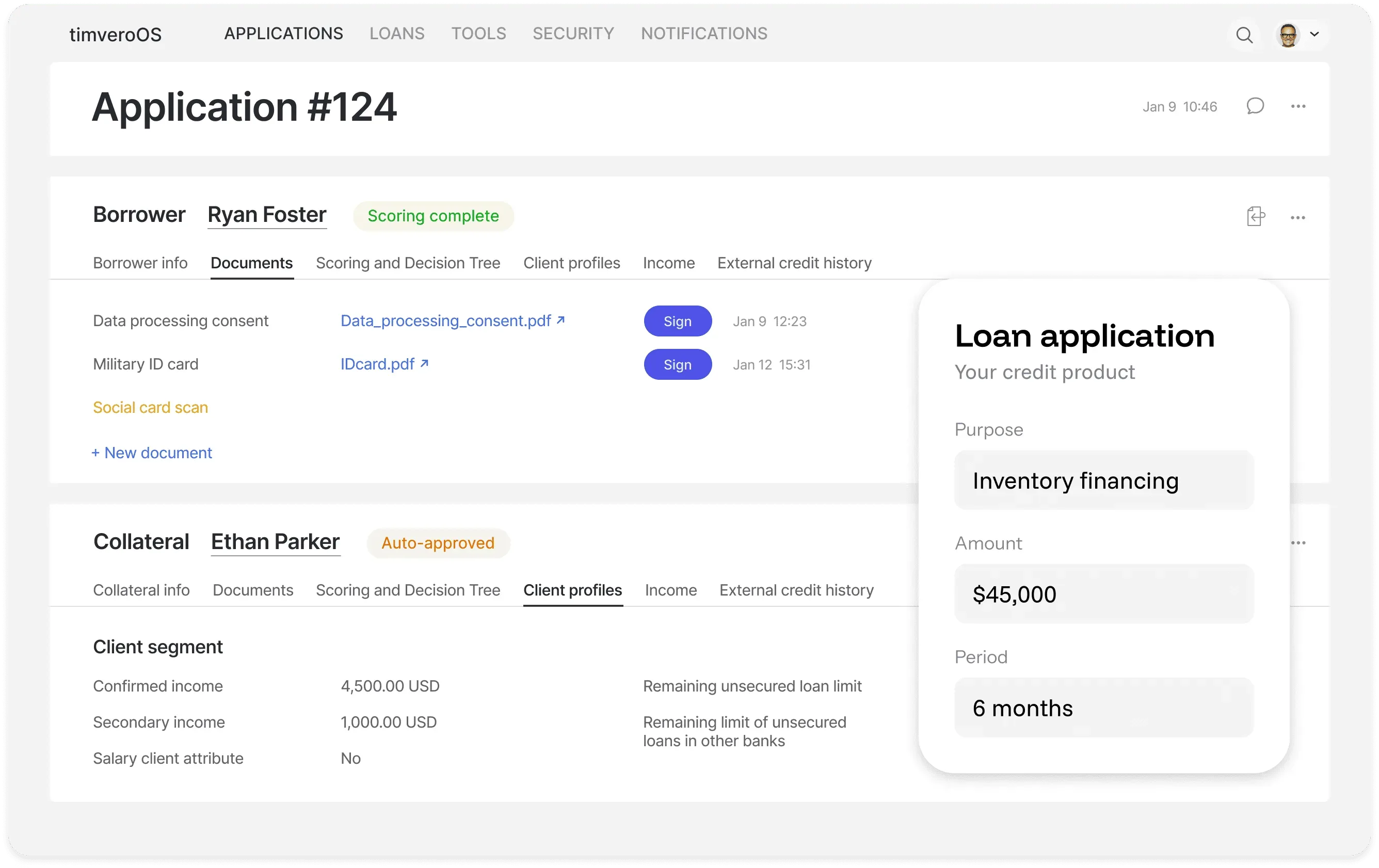

1. timveroOS: best overall for business-led configuration and fast iteration

timveroOS is a complete, end-to-end loan origination (opens in new tab) and loan servicing software (opens in new tab) platform built on a Building Platform: pre-built building blocks for origination, servicing, collections and advanced loan analytics (opens in new tab) that run on a single data, policy and compliance layer. It’s designed for lenders who want the speed of SaaS and the ownership of a custom build at the same time.

Two distinct AI components — kept separate by design. Most platforms treat AI as a credit-decision feature. timveroOS does that too, with an explainable scoring engine that produces transparent reason codes for every decision. But its bigger lever is timveroAI (opens in new tab), a RAG-grounded implementation agent that builds and adjusts the system itself. The two never overlap: the scoring engine decides loans at runtime; timveroAI accelerates how the platform is built and changed.

What that unlocks, anchored on the differentiators that separate a Building Platform from configurable SaaS:

- Code-level access. Your engineers extend the building blocks directly through an open SDK (Java/Spring Boot) — not just toggle settings, the vendor pre-built.

- 3–6 week bespoke launches. Pre-built blocks plus timveroAI compress what is normally a multi-quarter roadmap negotiation into weeks; timveroAI handles 70–80% of the implementation work, with human approval gates intact.

- Explicit compliance building blocks. IFRS 9, CECL, audit trails, and per-jurisdiction regulatory modules are transparent, versioned blocks — not opaque “compliance included” claims.

- Shadow-run mode. AI-generated changes run in shadow mode before going live; nothing reaches production without human review.

- Deploy in your own environment. Cloud, on-premise, or hybrid — you own the codebase, the data, and the version cadence, with no multi-tenant co-mingling and no vendor lock-in.

Proof points: $5.5B+ in loan portfolios managed, 7,000+ applications processed daily, 13+ countries. See how Finom (opens in new tab) (banking-grade lending in 4 months, 98% automation), Cartiga (opens in new tab) (litigation finance, replaced Salesforce at ~10% of its cost, 8-week MVP), and AMIO Bank (opens in new tab) (4-month MVP after three failed attempts, 60% lower cost-per-loan) run in production.

Best fit for banks (opens in new tab), fintech lenders (opens in new tab), credit unions (opens in new tab) and specialty / private-credit lenders (opens in new tab) that need SaaS speed without surrendering control. Less ideal for a very small, single-product operation that will never touch the custom logic beyond the pre-built modules.

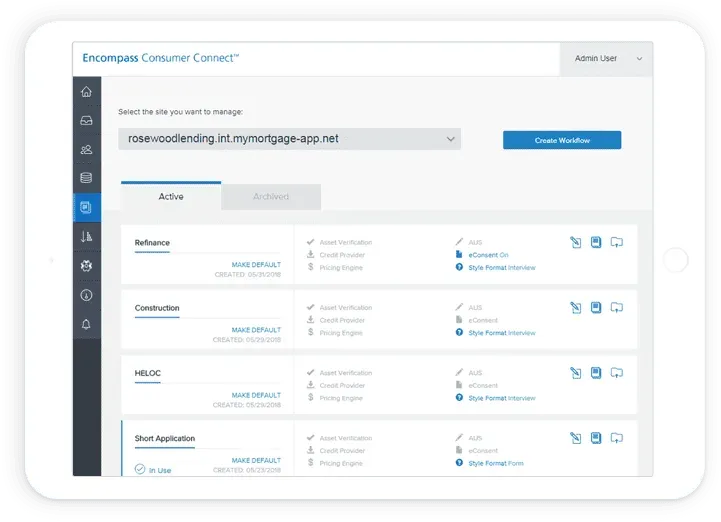

2. Encompass (ICE Mortgage Technology): best for mortgage at industry-standard scale

Encompass is the default choice for a large share of U.S. mortgage lenders, with deep functionality across the mortgage lifecycle from application to closing and investor delivery. It integrates tightly with ICE’s ecosystem, including its pricing engine and eClose tooling.

Strengths: widely considered the U.S. mortgage software (opens in new tab) standard; deep TRID, HMDA and RESPA support; a large integration marketplace.

Trade-offs: built for mortgage and doesn’t serve multi-product lenders well; a legacy architecture and UI many users describe as dated; costly and resource-intensive to implement.

3. nCino: best for Salesforce-native bank operations

nCino is a cloud banking platform built on Salesforce that supports commercial, small-business, and mortgage lending. For institutions already invested in Salesforce, it offers strong pipeline visibility and workflow automation inside a familiar ecosystem.

Strengths: native integration with the Salesforce CRM ecosystem; strong commercial and small-business capabilities; built for regulated institutions.

Trade-offs: heavy reliance on Salesforce raises cost and complexity; customization usually needs Salesforce expertise; implementation timelines can be long.

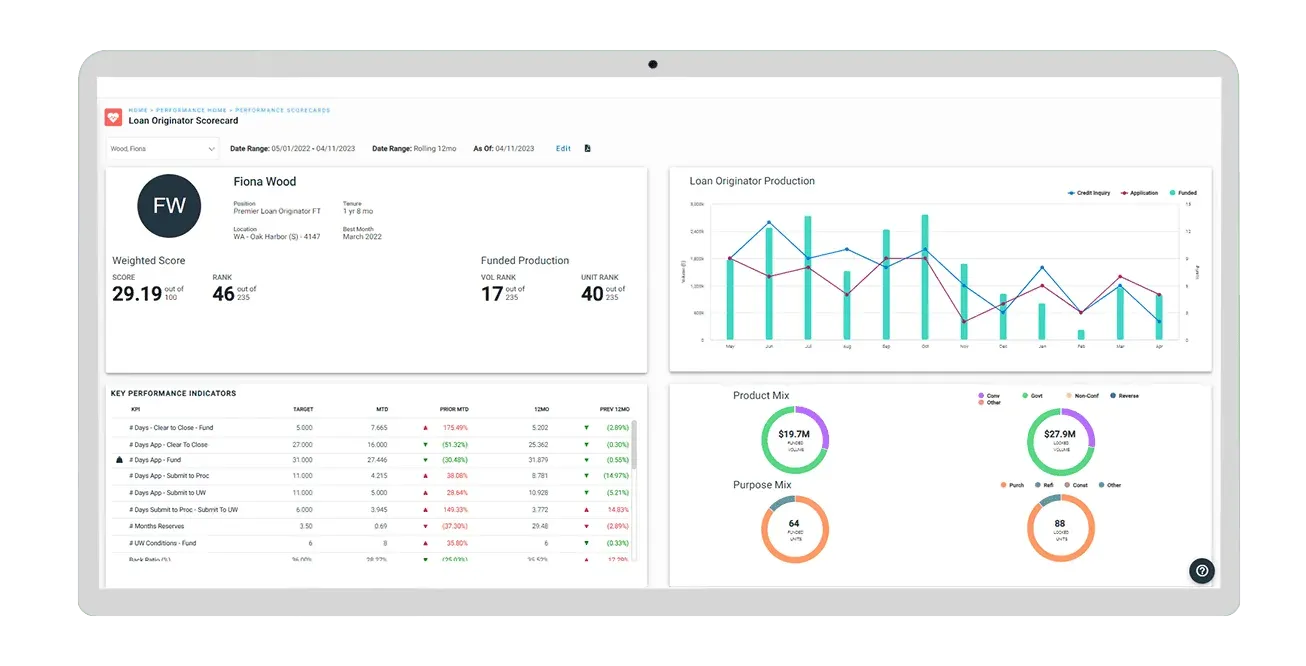

4. MeridianLink: best for credit unions and community banks

MeridianLink is widely used across the credit union and community-bank market, supporting consumer, mortgage, and indirect lending with integrated decisioning and a configurable process engine.

Strengths: strong fit for consumer and indirect lending at community institutions; solid compliance automation and prebuilt bureau/vendor integrations; reasonable timelines for mid-sized lenders. Trade-offs: limited flexibility for highly customized products; a UI that can feel dated; less suited to large-scale or unusually complex lenders.

5. Finastra: best for large banks needing a broad suite

Finastra offers loan origination as part of a much larger banking-technology portfolio, including its Originate and Mortgagebot platforms. It fits large and global institutions that want lending to sit inside a wider, deeply integrated stack.

Strengths: a comprehensive suite spanning many banking functions and geographies; a strong position in commercial and syndicated lending; deep core-banking integration.

Trade-offs: origination is one piece of a much larger ecosystem; implementation is complex and services-heavy; slower to innovate than newer platforms.

6. TurnKey Lender: best for automated, AI-driven decisioning

TurnKey Lender is a cloud lending platform focused on automation and AI-driven credit decisioning, covering origination through servicing and collections for consumer, commercial and SME products.

Strengths: AI and rules-based decisioning with built-in scoring; quicker deployment than most legacy systems; a broad end-to-end feature set with multi-currency support.

Trade-offs: customization is more limited than API-first platforms; lighter adoption among large U.S. institutions; decisioning models can raise explainability questions in tightly regulated settings.

7. DigiFi: best for API-first, embedded lending

DigiFi provides an API-first lending infrastructure aimed at embedded finance and fintech use cases, with real-time decisioning components and flexible integration into existing platforms.

Strengths: strong API-first architecture for embedded lending; support for multiple credit products and workflows; built for digital-first lenders.

Trade-offs: less brand recognition and proven enterprise scale than incumbents; may require meaningful development resources; lighter default UI and reporting out of the gate.

8. LendingPad: best for cloud-native mortgage origination

LendingPad is a cloud-native mortgage LOS built for lenders, brokers, and financial institutions that want a modern interface and real-time collaboration, with multiple team members working in the same loan file simultaneously.

Strengths: a modern, intuitive interface and real-time multi-user collaboration; affordable, with an integrated CRM and standard mortgage integrations; automated compliance reviews (QM, TRID).

Trade-offs: some disclosures still require manual steps; advanced automation is still maturing; mortgage-focused, so not a fit for multi-product lenders.

9. Blend: best for front-end borrower experience

Blend focuses on the borrower-facing application experience, helping lenders streamline digital onboarding for mortgage and consumer lending. It’s a polished front end rather than a complete origination system.

Strengths: modern borrower UX and fast front-end deployment; built-in income and asset verification integrations; continuous improvement of application flows.

Trade-offs: not a full end-to-end LOS or servicing platform; requires an LOS and servicing systems behind it; limited back-end workflow capability.

10. Abrigo: best for community banks focused on commercial lending and risk

Abrigo provides lending and credit-risk software aimed at community banks and credit unions, with a strong emphasis on compliance, reporting, and commercial lending workflows.

Strengths: designed for community banks and smaller institutions; strong compliance, reporting and risk-management focus; solid commercial lending software (opens in new tab) support.

Trade-offs: not positioned as a modern, full-stack origination platform; a steeper learning curve for the full feature set; less suited to digital-first or high-volume consumer lending.

SaaS vs Custom Build vs Building Platform: the three ways to own a LOS

Here’s the uncomfortable truth behind most LOS marketing in 2026: everyone now has AI. Nearly every vendor on this list will tell you about their AI capabilities, so AI on its own is no longer a differentiator. What matters is whether the architecture lets that AI actually change how fast you operate. That comes down to three ways of owning a loan origination system.

Configurable SaaS lets you toggle settings inside a fixed model the vendor pre-built. It’s fast to start but caps you at the vendor’s roadmap, and a multi-tenant deployment can complicate compliance. A custom build gives total control but buries you in an 18–24 month delivery, an engineering team of 8–15, and an ever-growing backlog. A Building Platform is the third path: a working system from day one, code-level control through an SDK, deployment in your own environment, and timveroAI to compress bespoke launches to weeks.

| Criterion | SaaS lending platforms | Custom build (in-house) | timveroOS Building Platform |

|---|---|---|---|

| Time to launch a bespoke product | 6–12 months on vendor roadmap | 18–24 months from scratch | 3–6 weeks with timveroAI |

| Architectural control | Configuration only | Full | Full (SDK access to building blocks) |

| Deployment | Multi-tenant cloud only | Self-hosted | Cloud, on-prem or hybrid |

| Vendor roadmap dependency | High | None | None |

| Engineering team required | 1–2 (config) | 8–15 engineers | 1–3 engineers + timveroAI |

| Cost predictability | Per-user / per-loan fees scale with portfolio | High variance, sunk cost | Predictable licensing |

| Compliance modules | Opaque, vendor-controlled | Built from scratch | Explicit blocks per jurisdiction |

For more on the economics behind this choice, see our deep dive on lending software beyond SaaS vs build (opens in new tab).

Deployment options: cloud, on-premise, hybrid

Many buyers search specifically for “cloud-based” or “web-based loan origination software” because deployment dictates data ownership and compliance posture. Most platforms on this list are multi-tenant cloud only. A Building Platform supports cloud, private-cloud, on-premise and hybrid deployment, so a regulated bank can keep borrower data inside its own environment while a digital lender runs fully in the cloud. Loan officers and borrowers reach the same system through responsive web applications, and origination workflows are accessible on mobile without a separate product.

What loan origination software costs in 2026

Pricing models vary widely, and the headline licence is rarely the real number. Some mortgage tools charge per loan file (from a few dollars to roughly $100–$200 per closed loan); enterprise platforms can start in the five-figures-per-month range. Per-user and per-loan models look simple but scale faster than your portfolio, which is why high-volume lenders increasingly evaluate cost per decision and three-year total cost of ownership rather than sticker price.

A custom build’s three-year TCO commonly runs $2–5M — often 60–80% higher than an equivalent subscription once delivery and maintenance risk are priced in. Portfolio-tiered licensing, the model timveroOS uses, keeps spend forecastable for finance while letting volume grow without a per-seat penalty. Always confirm implementation and integration costs separately — they’re where “cheap” platforms get expensive.

Migrating from a legacy LOS without a re-platform

The fear that keeps lenders on aging systems is the migration itself. A Building Platform approach turns a rip-and-replace into a staged 12-week motion: weeks 1–2 to map the existing product and data model, weeks 3–6 to assemble the origination flow from pre-built blocks and connect bureaus and your core via prebuilt integrations, weeks 7–10 to run the new flow in shadow mode against live volume, and weeks 11–12 to cut over one product line. Because timveroAI generates and tests the configuration against your existing system, you integrate with — rather than replace — your current loan management stack first, then expand product by product.

Compliance and model governance across the US, UK and EU

A loan origination system is only as good as the audit trail behind its decisions. For U.S. mortgage that means TRID, HMDA and RESPA; for institutional lenders, IFRS 9 or CECL provisioning. For any AI used in credit, model governance is now the deciding factor: U.S. supervisors expect SR 11–7-style model risk management, and the EU AI Act’s high-risk obligations for creditworthiness models phase in from August 2026.

The architectural answer is to make the credit decision deterministic and explainable rather than a black box. timveroOS keeps its explainable scoring engine separate from timveroAI, so every decision produces reproducible reason codes a risk officer can defend, while AI-generated configuration changes pass through shadow-run mode and human approval before they touch production. That separation is what lets a lender adopt AI for speed without inheriting an unsupervisable decision process. For the underlying mechanics, see our explainer on how AI and automation are transforming lending (opens in new tab).

Measurable outcomes: three lenders in production

The Building Platform model is proven across very different lenders on the same architecture.

“What impressed me most was their ability to work at our pace, absorbing requirements on the fly, proposing solutions proactively, and adapting as our needs evolved. Today, we’re running proactive credit campaigns and sophisticated servicing operations on a single platform. timveroOS delivered a competitive advantage under impossible deadlines.”

— Alex Goncharenko, Head of Credit, Finom

Finom, a European EMI serving 200,000+ business customers across five countries, launched banking-grade lending in four months with 98% process automation and Day 1 ROI. In specialty finance, Cartiga describes the experience in their own words:

“timveroOS has become the core engine behind our law firm lending business. Its framework allowed us to build sophisticated workflows, pricing, and collateral logic per our bespoke structures — something no SaaS or traditional LMS could offer.”

— Noah Cutler, Senior Vice President, Cartiga

Cartiga deployed $1.6B+ in litigation finance, replaced a Salesforce-based setup at roughly 10–12% of its cost, and reached an MVP in eight weeks. On the bank side, AMIO Bank (opens in new tab) delivered a bespoke product MVP in four months after three failed attempts elsewhere, with 8x faster time-to-yes and a 60% reduction in cost-per-loan.

How to choose the right loan origination system for your model

The right system depends on your model, not on which vendor markets hardest. Map your use cases first: a platform built for residential mortgage may not fit commercial, BNPL or private credit, so buy for where you’re going. Check compliance fit for your jurisdictions; assess how few manual handoffs the integrations leave; and treat a multi-year rollout as a red flag.

The fit also varies by institution type. Banks (opens in new tab) weigh core-banking integration and regulatory depth. Fintechs (opens in new tab) need product structures that don’t fit generic SaaS schemas and pricing that doesn’t punish growth. Credit unions (opens in new tab) need transparent thin-file decisioning on a small IT team. And requirements differ by market — see our country guides for the United States (opens in new tab), United Kingdom (opens in new tab), Netherlands (opens in new tab), Canada (opens in new tab) and Spain (opens in new tab). Across all of them, the deciding question is the same: how fast can your own team change the system, and who has to be involved?

Frequently Asked Questions

What is loan origination software?

Loan origination software (an LOS) is a platform that automates and manages the loan lifecycle from application through approval and funding. Core capabilities include application intake, credit decisioning, document management, compliance, and reporting. More advanced platforms extend into servicing, collections, and analytics on a single connected layer.

Should you build or buy a loan origination system?

Buying is faster for most lenders, but the real choice in 2026 is three-way. Configurable SaaS is quick yet caps you at the vendor’s roadmap; a custom build gives control but takes 18–24 months. A Building Platform is the third path: pre-built modules cover most of the lifecycle while you keep code-level control over the logic unique to your business.

Which loan origination platform has the fastest implementation time?

Timelines range from a few weeks to over a year. Enterprise mortgage systems often need extensive configuration; a multi-year rollout is a red flag in 2026. Platforms with pre-built blocks reach a working product faster — timveroOS, for example, brings new bespoke products live in roughly 3–6 weeks using its timveroAI implementation agent, integrating with your existing systems first.

How do you avoid vendor lock-in with a loan origination system?

Lock-in comes from owning neither the code nor the data. Avoid it by choosing a platform with code-level SDK access, deployment in your own environment, and the ability to change business logic without a vendor change request. With that combination, you can support custom, team-specific workflows and still move off or extend the platform on your own terms.

What’s the difference between loan origination and loan servicing?

Origination (opens in new tab) covers everything up to funding — application, underwriting, approval and closing. Servicing (opens in new tab) begins after funding: payment processing, interest calculation, statements, collections, and account management. Some platforms specialize in one; others, like timveroOS, cover the full lifecycle on one connected platform.

How is AI used in loan origination, and is it compliant?

AI appears in two distinct roles. A scoring engine can surface explainable decision logic with reason codes for human approval at runtime, while an implementation agent like timveroAI accelerates how the system is built and changed. Kept separate and paired with shadow-run testing and audit trails, AI supports SR 11–7 and EU AI Act expectations rather than undermining them.

Ready to launch your lending product faster?

If your shortlist comes down to how fast your team can change the system once it’s live, see what a Building Platform does with a working demo on your own product line.

Head of Marketing

Ivan Halynkin leads Growth & Marketing at TIMVERO, the company behind timveroOS and timveroAI. He works across the seam between product and demand — translating composable lending infrastructure into positioning, content, and demos that resonate with banks, credit unions, and fintechs. His writing focuses on what actually moves the needle for digital lenders: origination economics, AI in credit decisioning, and the trade-offs between SaaS lending boxes and building-platform thinking.

LinkedinLatest News

Bank Efficiency Ratio: What It Is and How to Improve It

Lending Software Beyond SaaS vs Build: The Third Path

Automated Loan Origination: How Lenders Cut Abandonment Rates and Speed Up Approvals

Embedded Lending for Vertical SaaS: Monetize & Own It

What Is Embedded Lending? How It Works and Why It Matters

Best AI-Powered Lending Platforms in 2026: A Buyer’s Guide

How U.S. Banks Should Rethink Credit Card Strategy in a Potential 10% APR Cap Environment

Open Banking Is Quietly Rewriting How Loans Work

AI Hallucinations in Lending Software: How to Stop Them