Lending Software Beyond SaaS vs Build: The Third Path

Lenders evaluating SaaS lending platforms or custom builds are choosing between systems they cannot change and projects they cannot finish. A Building Platform is the third path: a working lending system on day one, with full architectural control through an SDK, deployed in your own environment. timveroOS runs $5.5B+ in loan portfolios across 13+ countries on this approach, and with timveroAI, compresses bespoke product launches from 18 months to 3–6 weeks.

Every lending team eventually hits the same wall. The SaaS platform won’t bend to the product you want to launch. The in-house build won’t ship before the market window closes. You are left choosing between a system you can’t change and a project you can’t finish — and neither path lets you operate a portfolio that is actually yours. This is the gap that the Building Platform approach was designed to close: a working lending system from day one, with full architectural control at the code level, deployed in your own environment. timveroOS has been built on this approach since the company began, and runs $5.5B+ in loan portfolios across 13+ countries today. This article walks through why the binary “buy vs build” framing fails most lenders in 2026, what a Building Platform actually is, and how it changes the math on launching new lending products.

Why Lenders Keep Picking the Wrong Tool

The global loan management software market is on a fast curve. Independent market research (opens in new tab) sized the segment at $10.22 billion in 2024 and projects $21.62 billion by 2028, driven by digitization in mid-market banking and the rise of non-bank lenders. Behind that growth is a less-discussed reality: most lenders are spending more time choosing the wrong infrastructure than running the right one.

The reason is structural. The decision is usually framed as a binary — buy a SaaS platform, or build your own — and both options are designed for the wrong problem.

The SaaS Trap

SaaS lending platforms are built to serve many tenants on one codebase. That model is efficient for the vendor and predictable for the buyer at the start. It breaks the moment you need a product the vendor did not anticipate.

When a Tier 3 bank needs a credit product with a 30-day grace period and a floating rate based on a local benchmark, the SaaS answer is “submit a roadmap request.” When a fintech needs to support a non-standard repayment structure for a BNPL pilot, the SaaS answer is “configure within the supported parameters or wait for the next release.” When a compliance officer at a credit union asks where the data lives, the SaaS answer is “in our multi-tenant cloud, with logical separation.” For regulated lenders, none of those answers are operationally acceptable.

The other problem is pricing topology. Most SaaS lending platforms charge per active loan or per user. As the portfolio grows, the variable cost scales with it — sometimes faster than revenue per loan. Deloitte’s 2024 (opens in new tab) financial services survey noted that subscription pricing models for core lending infrastructure increasingly come under scrutiny as portfolios scale beyond initial assumptions. The implicit promise — “start fast, scale later” — converts into a real ceiling somewhere between MVP and meaningful scale.

The Custom Build Trap

The opposite path is to build your own lending system. This route is taken seriously by Tier 1 banks with dedicated engineering organizations and by fintechs whose investors will fund 18 months of pre-revenue work. For everyone in between, it is a slow disaster.

What a custom team actually has to build is rarely understood at the start. A working lending platform needs a participant data model that treats borrowers, guarantors, co-signers, and corporate entities as first-class records. It needs a loan lifecycle state machine that handles origination, servicing, restructuring, and collections without breaking when products change. It needs an accrual engine that supports floating rates, day-count conventions, grace periods, and early repayment recalculations. It needs GL posting logic, regulatory reporting modules, integrations with payment rails, KYC and AML providers, credit bureaus, and core banking systems. And it needs all of that with audit trails, role-based access controls, and the ability to deploy in environments compliance teams will sign off on.

A team of eight to fifteen engineers can ship that in eighteen to twenty-four months. Few mid-market lenders have that team, that budget, or that runway. By the time the system is production-ready, the original product hypothesis has changed, the engineers who built it have moved on, and the maintenance burden has begun.

“timveroOS has become the core engine behind our law firm lending business. Its framework allowed us to build sophisticated workflows, pricing, and collateral logic per our bespoke structures — something no SaaS or traditional LMS could offer.” — Noah Cutler, Senior Vice President, Cartiga

Cartiga’s experience captures the trap from the other side. The company tried to run litigation finance — a product no SaaS vendor supports — on Salesforce. The result was a system that cost roughly ten times what the equivalent timveroOS deployment cost, and took ten times longer to reach production. Cartiga eventually replaced Salesforce with timveroOS at 10–12% of the original budget, with the MVP live in eight weeks. The lesson is not that Salesforce is bad. The lesson is that bending a horizontal CRM into a vertical lending system is, mathematically, a custom build with extra steps.

What a Building Platform Actually Is

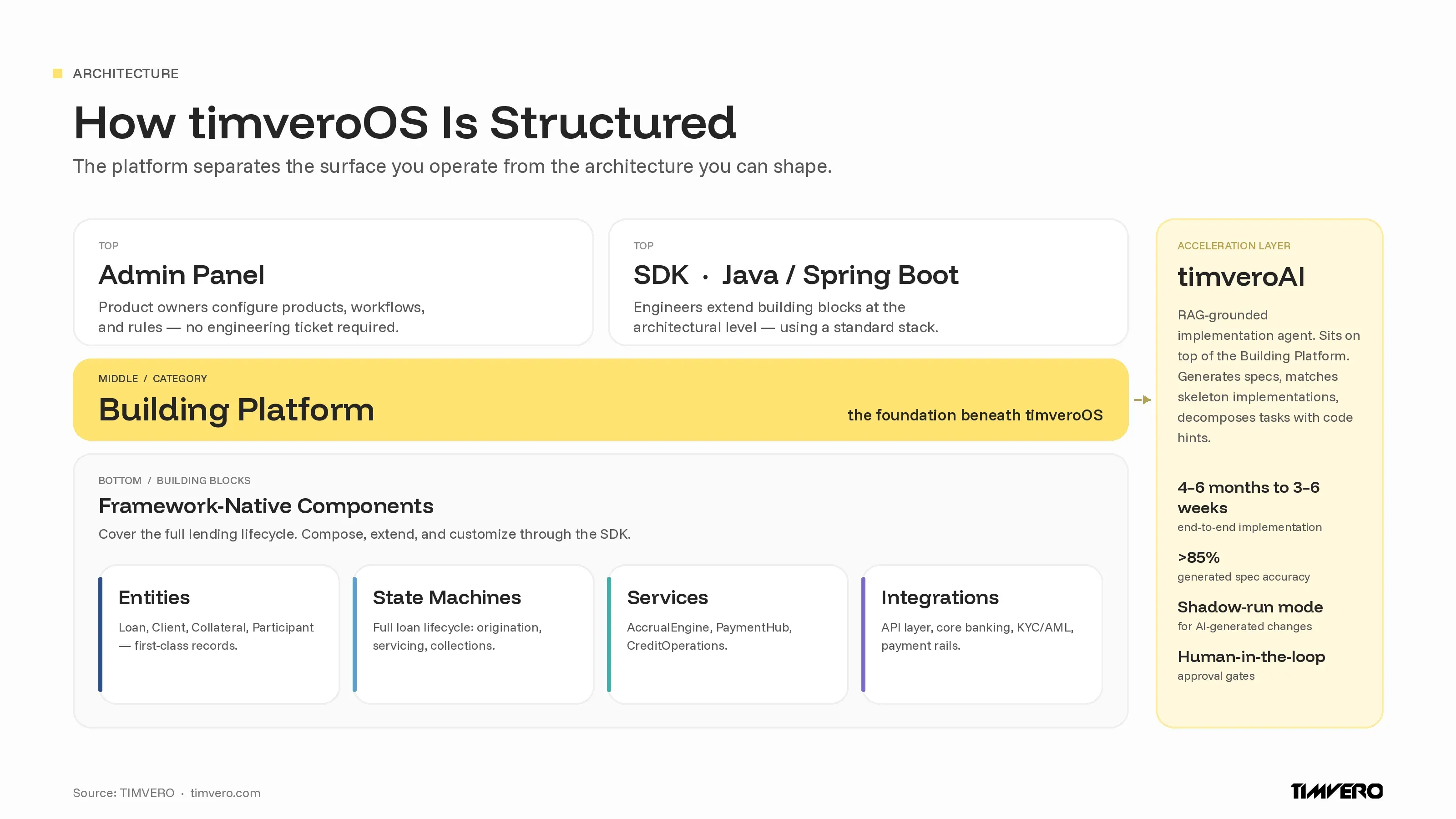

Building Platform — definition. A Building Platform is a category of lending infrastructure that combines a working system on day one with code-level architectural control. Product owners configure the system through an admin panel; engineers extend it through an SDK that gives access to the same building blocks — entities, state machines, services, and integrations. timveroOS is the first Building Platform purpose-built for lending.

A Building Platform resolves the binary between SaaS and custom build. It is a working lending system on day one — administrators can log in, configure products, set up workflows, and originate loans through an admin panel without writing code. It is also a code-level architectural foundation — engineers can extend the system at the level of entities, state machines, services, and integrations, using a standard stack rather than a proprietary toolchain.

The hierarchy is straightforward:

- timveroOS is the product the buyer adopts.

- Building Platform is the foundation beneath it, made up of framework-native building blocks.

- Building Blocks are the entities (Loan, Client, Collateral, Participant), state machines (loan lifecycle), services (AccrualEngine, PaymentHub, CreditOperations), and integrations (API layer, external providers) that cover the full lending lifecycle.

- The admin panel surfaces all configurable behaviour for product owners. The SDK, built on Java and Spring Boot, gives engineers code-level access to the same architecture.

- timveroAI sits on top of the platform as a RAG-grounded implementation agent that accelerates configuration and extension work. It is not a chatbot and not a code copilot — it is an agent with persistent project context, human-in-the-loop approval gates, and shadow-run mode for changes before they go live.

Working System From Day One

The Building Platform is not a framework you have to assemble. The admin panel ships with the full lending lifecycle wired up — origination flows, servicing operations, collections workflows, accruals, payments, accounting postings, and reporting. A product owner can launch a standard installment loan on day one without an engineering ticket.

This is the part the SaaS framing gets right and the custom-build framing forgets: you should not have to build the obvious things twice. Pre-built building blocks for participant data, state machines, accrual logic, and GL postings are not an interesting differentiator. They are the table stakes. The interesting differentiator is what happens when you need to change them.

Architectural Control at the Code Level

This is where SaaS hits a wall and where the Building Platform opens a door. The SDK gives engineers direct access to the same building blocks the admin panel exposes — but at the architectural level. A bank that needs a non-standard day-count convention can extend the AccrualEngine. A fintech adding a new product type can compose new state machines on top of the existing lifecycle. A specialty lender with a unique collateral model can extend the entity layer to represent it natively.

The work is done in standard Java and Spring Boot — the same patterns engineers already use elsewhere. Extensions surface as configurable options in the admin panel, so product owners gain the new capability without further engineering work. The configuration becomes a setting. The code stays with the client.

This is the first of the two differentiators that define the category against SaaS and against custom build: code-level access to the architectural layer of the system, not just to its configuration parameters.

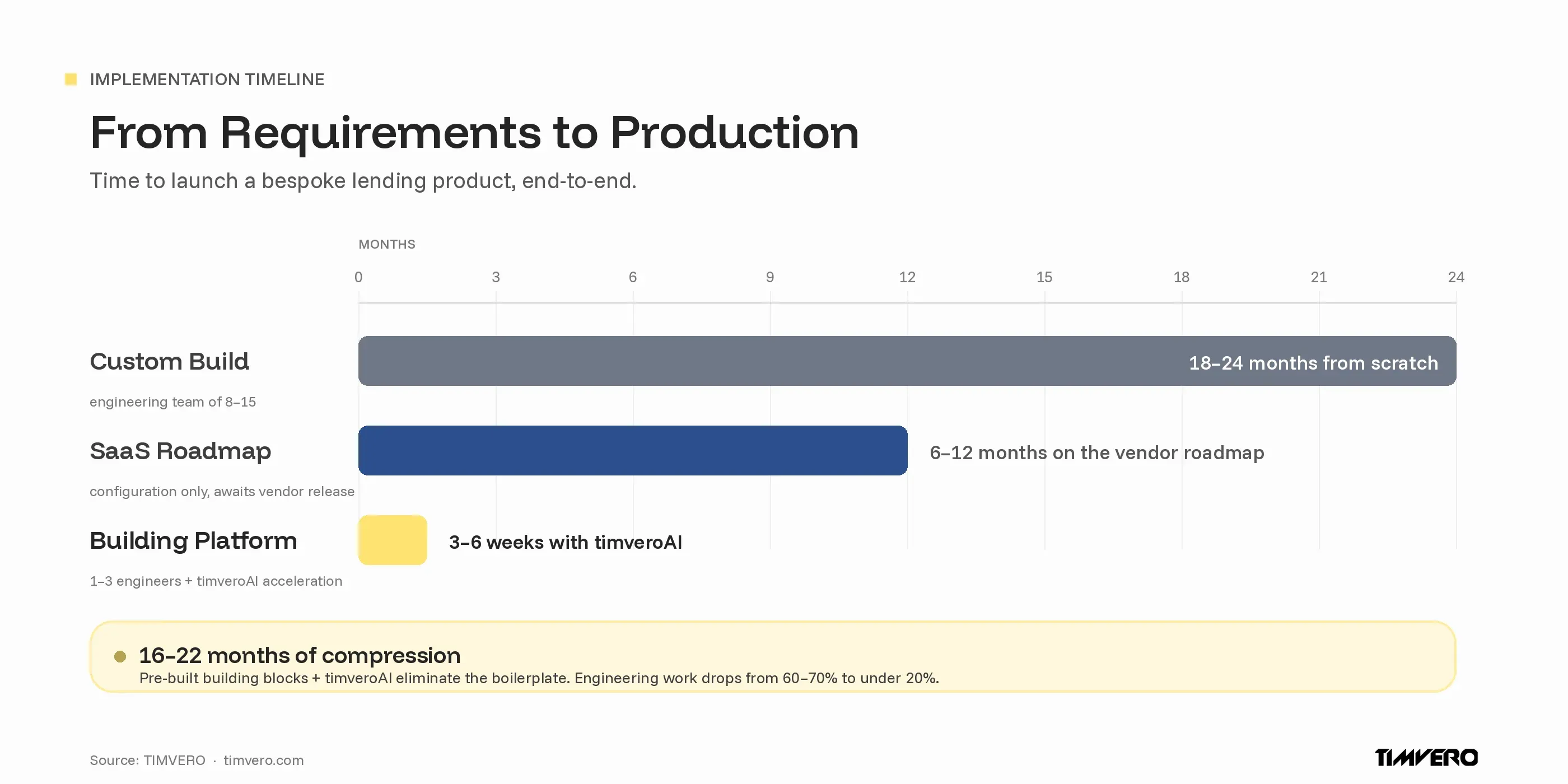

How the Third Path Compresses Bespoke Launches Into Weeks

At a glance. A bespoke product on SaaS takes 6–12 months of vendor-roadmap negotiations. A custom build from scratch takes 18–24 months and a team of 8–15 engineers. On the timveroOS Building Platform with timveroAI, the same product reaches production in 3–6 weeks with 1–3 engineers, because the building blocks are pre-built and the AI agent handles 70–80% of the implementation work.

The second differentiator is implementation speed. A bespoke lending product on a SaaS platform is typically a six-to-twelve-month negotiation with a vendor roadmap. The same product built from scratch is typically eighteen to twenty-four months of engineering work. On the Building Platform, with timveroAI handling the implementation acceleration, the same product reaches production in three to six weeks.

Pre-Built Building Blocks Cover the Lifecycle

Because the Building Platform already covers the full lending lifecycle through its building blocks, the work of launching a new product is not “build a lending system.” It is “configure the system you already have, and extend the parts that need to change.” For most products, that means the originator’s job is mostly configuration in the admin panel — eligibility rules, pricing, document templates, workflow stages — and the engineer’s job is limited to the parts where the product genuinely diverges from a standard pattern.

The TIMVERO platform processes 7,000+ daily loan applications (opens in new tab) across active deployments, which means the building blocks have been pressure-tested in production at scale. New deployments inherit that maturity. They are not starting from zero.

timveroAI as the Acceleration Layer

timveroAI is not a separate product. It is a layer that sits on top of the Building Platform and accelerates the work of configuring and extending it. The agent is grounded in the platform’s source code, in a structured ontology of lending features, and in a skeleton library of complete, production-tested reference implementations. When a business analyst describes a new product, the agent interviews them, produces a structured specification with greater than 85% accuracy, selects the closest skeleton, and decomposes the work into tasks with code hints that engineers can pick up directly in their IDE.

The agent runs as an agentic loop with plan-execute-verify behaviour, not as an autocomplete tool. It maintains a persistent project context across sessions. It detects divergence between code and specification and flags it for review. Changes it generates can run in shadow mode before going live, so compliance and engineering teams retain control. Across deployments, timveroAI (opens in new tab) compresses the engineering portion of an implementation from sixty to seventy percent of working time down to under twenty percent. The combined effect on end-to-end timelines is the move from four to six months to three to six weeks.

This is the second of the two differentiators: bespoke products in three to six weeks, not in vendor-roadmap quarters or in custom-build years.

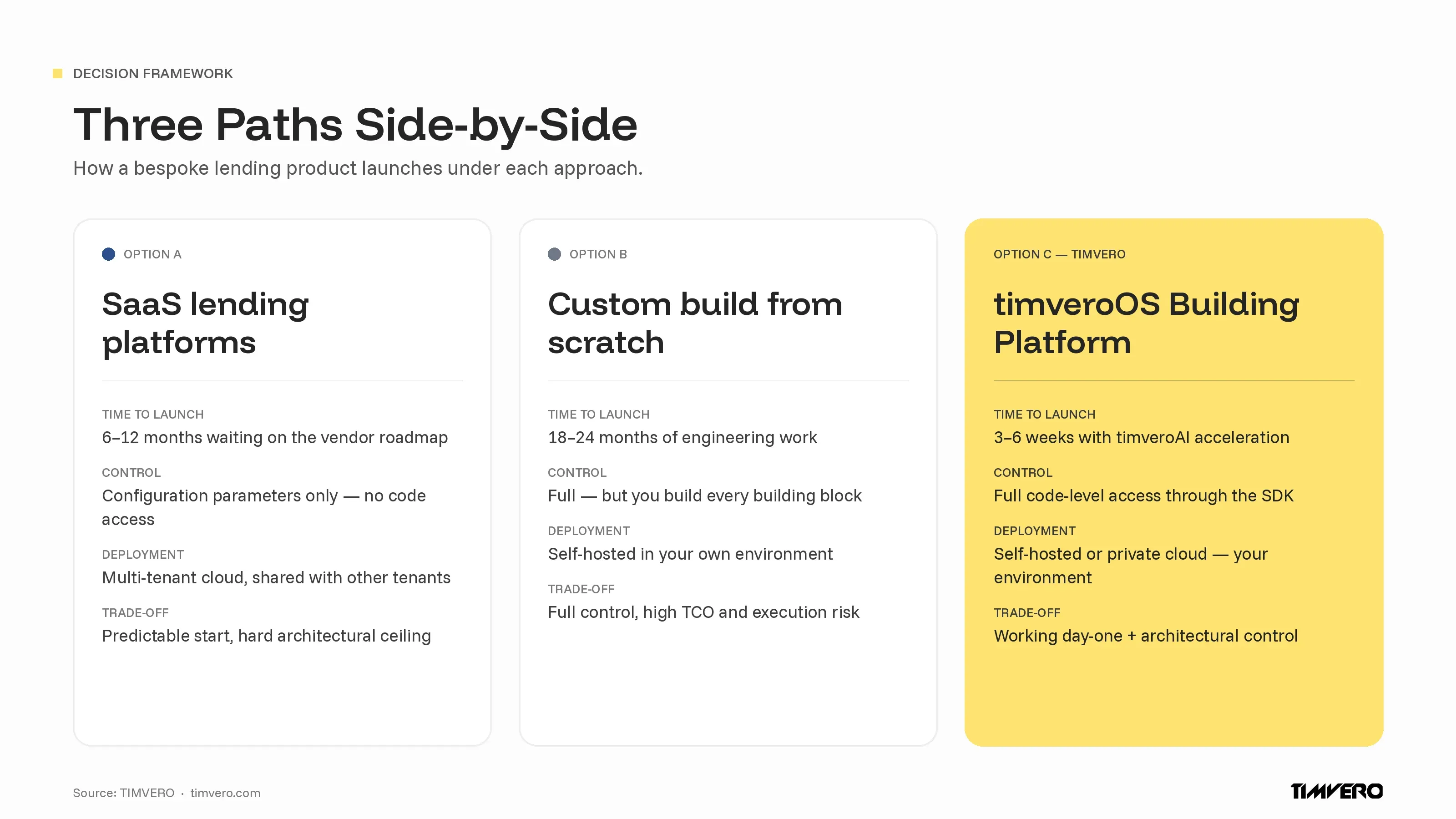

Three Paths Side-by-Side: A Decision Framework

Snapshot. Across the eight criteria that matter most for a regulated lender — time to launch, architectural control, deployment topology, vendor lock-in, engineering team size, cost predictability, compliance transparency, and source code ownership — the Building Platform either matches or exceeds both SaaS and custom build on every dimension except day-one configuration simplicity, where SaaS still leads marginally.

The choice between SaaS, custom build, and a Building Platform is not a preference. It is a structural decision that determines which products you can launch, how fast, and at what total cost of ownership. The table below summarizes how the three paths compare on the dimensions that matter most to lending teams in 2026.

| Criterion | SaaS lending platforms | Custom build (in-house) | timveroOS Building Platform |

|---|---|---|---|

| Time to launch a bespoke product | 6–12 months on vendor roadmap | 18–24 months from scratch | 3–6 weeks with timveroAI |

| Architectural control | Configuration only | Full | Full (SDK access to building blocks) |

| Deployment topology | Multi-tenant cloud only | Self-hosted | Self-hosted or private cloud |

| Vendor roadmap dependency | High | None | None |

| Engineering team required | 1–2 (configuration only) | 8–15 engineers | 1–3 engineers + timveroAI |

| Cost predictability | Per-user / per-loan fees scale with portfolio | High variance, sunk cost | Predictable licensing |

| Compliance modules | Opaque, vendor-controlled | Built from scratch | Explicit building blocks per jurisdiction |

| Source code ownership | None | Full | Full |

The pattern is consistent. SaaS optimizes for fast start and predictable initial cost; it trades away architectural control and deployment flexibility. Custom build optimizes for control; it trades away time, predictability, and most of the available implementation budget. The Building Platform optimizes for the dimensions that actually matter for a regulated lender operating a portfolio over multiple years — control, speed, predictability, and deployment topology — while preserving the day-one usability that makes SaaS attractive in the first place.

What the Building Platform Looks Like in Production

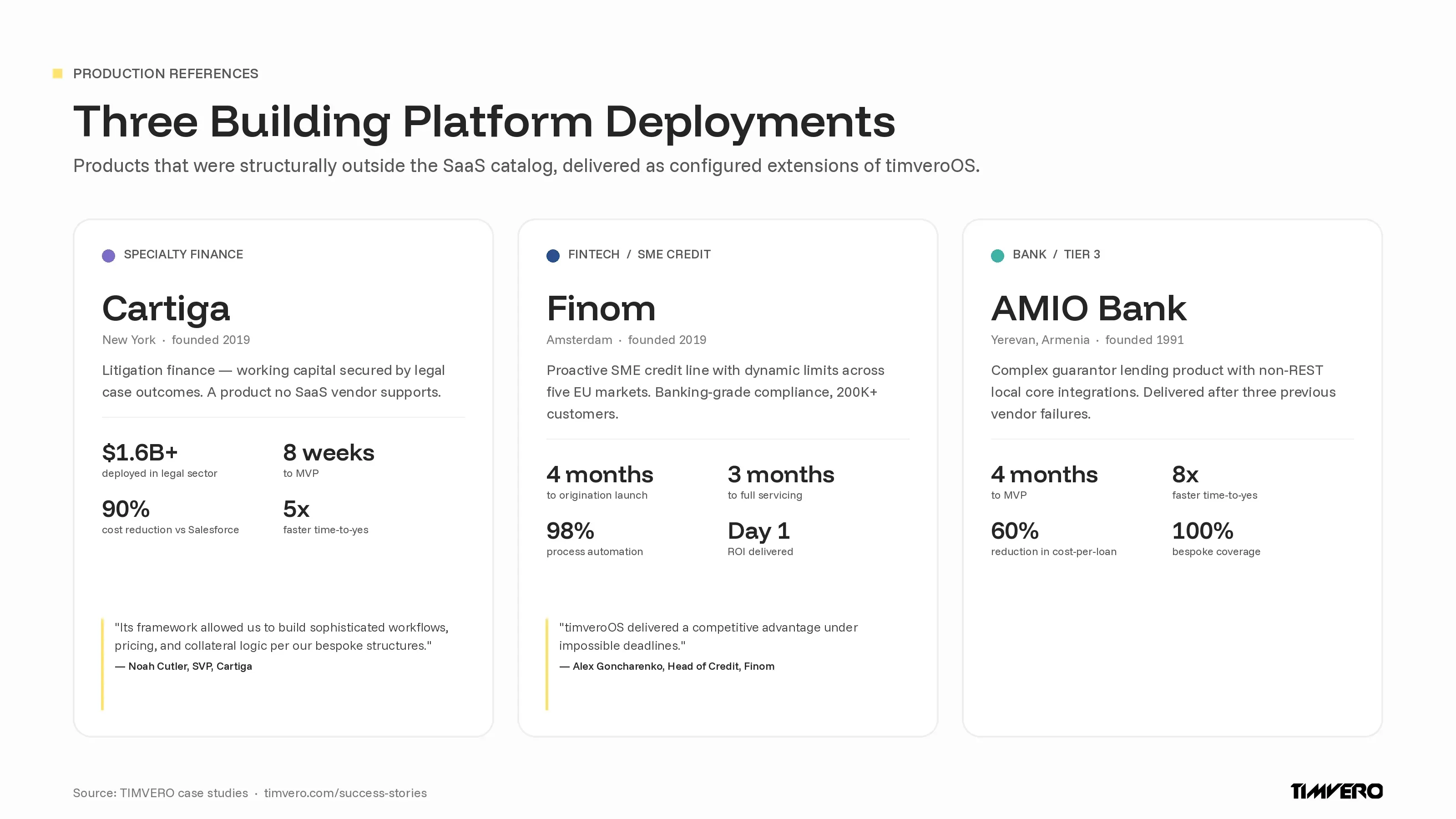

Concrete deployments make the differentiators legible. Three references, drawn from different segments, show what each path’s tradeoffs look like in practice.

Cartiga runs a litigation finance product — working capital secured by legal case outcomes — that no SaaS vendor supports. The company had previously attempted to run the product on Salesforce, an enterprise CRM bent into a lending shape. The Salesforce setup took years and cost roughly ten times what an equivalent timveroOS deployment cost. On timveroOS, Cartiga reached MVP in eight weeks and a full operational solution in ten weeks, with 100% coverage of bespoke lending flows (opens in new tab) and a 5x improvement in time-to-yes and disbursement. The deployment now supports $1.6B+ in legal sector investments.

Finom is a European fintech serving 200,000+ SME customers across Germany, France, Italy, Spain, and the Netherlands. The product is a proactive credit line with dynamic limits — a structure that requires event-driven architecture, multi-country regulatory handling, and full automation of underwriting and servicing. timveroOS delivered banking-grade origination in four months and full servicing operations in three, with 98% process automation and ROI from day one.

“What impressed me most was their ability to work at our pace, absorbing requirements on the fly, proposing solutions proactively, and adapting as our needs evolved. Today, we’re running proactive credit campaigns and sophisticated servicing operations on a single platform. timveroOS delivered a competitive advantage under impossible deadlines.” — Alex Goncharenko, Head of Credit, Finom (opens in new tab)

AMIO Bank, a regional bank in Armenia, attempted to launch a complex guarantor lending product three times with two different vendors before deploying timveroOS. The launched product covered 100% of bespoke origination requirements, achieved 95% process automation, delivered an 8x improvement in time-to-yes, and reduced cost-per-loan by 60% — including non-REST integrations with local core banking systems that previous vendors could not handle.

The pattern across the three deployments is the same: products that were structurally outside the SaaS catalog, on timelines that ruled out a custom build, delivered as configured extensions of the Building Platform.

Who This Approach Fits

The Building Platform approach is designed for lenders who need real architectural control without the runway for a full custom build. In practice, that means four segments.

For Tier 3 and Tier 4 banks, the Building Platform clears the two structural objections that disqualify multi-tenant SaaS: data residency and architectural control over compliance logic. The platform deploys in the bank’s own environment — on-premises or private cloud — and exposes regulatory modules as transparent building blocks that compliance teams can review. Lending software for banks (opens in new tab) is built around exactly this profile.

For fintechs, the question is usually whether the platform can scale from a $10M MVP portfolio to a $1B+ growth-stage portfolio without replatforming. The Building Platform preserves architectural control across that growth curve, with no per-user pricing topology that scales faster than the business. Lending software for fintechs (opens in new tab) is designed to support that arc end-to-end.

For credit unions, the central constraint is engineering capacity. A lean IT team cannot maintain a custom build, but cannot accept the multi-tenant compliance posture of most SaaS platforms either. The Building Platform gives a credit union admin-panel control over the day-to-day, with timveroAI handling the configuration work that would otherwise require an engineering ticket.

For specialty finance — factoring, leasing, asset-based lending, construction finance, private credit, litigation finance — the entire category is non-standard by definition. Generic SaaS treats specialty structures as edge cases. The Building Platform treats them as native configurations on top of the same building blocks.

When the Building Platform Is Not the Right Fit

Anti-fit. The Building Platform is the wrong choice for organizations that fall into one of three profiles: very large banks with in-house core engineering, very small lenders without any IT team, and buyers who explicitly want a no-customization workflow tool. For those three groups, a custom build or a closed SaaS is a better match than a Building Platform.

The Building Platform is built around a specific assumption: the lender wants real architectural control but does not have the runway to build everything from zero. That assumption is wrong for some organizations, and naming them is part of an honest evaluation.

Tier 1 banks with in-house core engineering capacity. Large banks that already operate dedicated core banking and lending engineering organizations have already absorbed the fixed cost of building everything in-house. For them, a Building Platform is duplicative; their build path will probably stay the right answer.

Very small lenders without any IT capacity. A micro-MFI or a one-person shop with no engineering team and no product manager will not benefit from a Building Platform’s SDK and admin-panel duality. A simple no-customization workflow tool is a better match than infrastructure that expects technical ownership.

Buyers who explicitly want no customization. Some organizations make a deliberate choice to operate strictly within a vendor’s supported configurations, with no extensions and no custom workflows. For that preference, a fully closed SaaS lending product is the architecturally honest match.

For everyone else — the four segments described in the previous section — the Building Platform sits in the gap where neither SaaS nor a custom build is the right answer.

Frequently Asked Questions

What is a Building Platform for lending software?

A Building Platform is a category of lending infrastructure that combines a working system on day one with code-level architectural control. Product owners configure the system through an admin panel; engineers extend it through an SDK that gives access to the same building blocks. timveroOS is built on this approach.

How is a Building Platform different from a SaaS lending platform?

A SaaS lending platform exposes configuration parameters but not architecture. Modifications require the vendor to ship them on a roadmap. A Building Platform exposes the architectural layer to the client’s own engineers through an SDK, so changes that would be vendor-blocked on SaaS can be made directly.

How long does it take to launch a lending product on the Building Platform?

End-to-end implementation timelines on timveroOS run from three to six weeks with timveroAI handling specification and skeleton matching. For comparison, equivalent bespoke products on SaaS typically wait six to twelve months on a vendor roadmap; a custom build from scratch takes eighteen to twenty-four months.

Where does a Building Platform get deployed — cloud or on-premises?

timveroOS deploys in the client’s own environment, either self-hosted on-premises or in a private cloud the client controls. This deployment topology is what lets the platform clear compliance bars that multi-tenant SaaS cannot — data residency, environment isolation, and platform version control on the client’s schedule.

Does the Building Platform support specialty lending products like factoring or leasing?

Yes. The Building Platform’s entities, state machines, and accrual logic are designed to be extended for non-standard product types. Active timveroOS deployments cover litigation finance, SME proactive credit lines, multi-jurisdictional retail lending, and other specialty structures.

What is timveroAI and how does it relate to the Building Platform?

timveroAI is a RAG-grounded implementation agent that sits on top of the Building Platform. It accelerates the configuration and extension work by interviewing business analysts, generating structured specifications, matching skeleton implementations, and decomposing tasks for engineers. Changes it generates run in shadow mode before going live, with human-in-the-loop approval gates.

Ready to See the Building Platform in Action?

If your team is stuck between a SaaS platform you cannot change and a custom build you cannot finish, the third path is worth a serious look. The fastest way to evaluate fit is a working session walking through your specific lending product and the building blocks it would need.

Head of Marketing

Ivan Halynkin leads Growth & Marketing at TIMVERO, the company behind timveroOS and timveroAI. He works across the seam between product and demand — translating composable lending infrastructure into positioning, content, and demos that resonate with banks, credit unions, and fintechs. His writing focuses on what actually moves the needle for digital lenders: origination economics, AI in credit decisioning, and the trade-offs between SaaS lending boxes and building-platform thinking.

LinkedinLatest News

Bank Efficiency Ratio: What It Is and How to Improve It

Best Loan Origination Software in 2026: 10 Systems Compared

Automated Loan Origination: How Lenders Cut Abandonment Rates and Speed Up Approvals

Embedded Lending for Vertical SaaS: Monetize & Own It

What Is Embedded Lending? How It Works and Why It Matters

Best AI-Powered Lending Platforms in 2026: A Buyer’s Guide

How U.S. Banks Should Rethink Credit Card Strategy in a Potential 10% APR Cap Environment

Open Banking Is Quietly Rewriting How Loans Work

Generative AI in Banking: Where It Works and Where It Can’t