Embedded Lending for Vertical SaaS: Monetize & Own It

Vertical SaaS platforms already sit on the two things a lender spends years and millions trying to acquire: a captive base of businesses and deep, real-time data about how those businesses actually operate. Embedded lending turns both into a high-margin revenue line — but only if you choose the right way to deliver it. The platforms that win treat credit as a product they own and shape on a Building Platform like timveroOS, not as a feature they rent from a third party. This guide breaks down how vertical SaaS makes money on embedded lending, what the ROI actually looks like, how to evaluate the best embedded lending solutions for vertical SaaS, and how to launch in weeks instead of quarters.

Why embedded lending is the strongest revenue lever in vertical SaaS

Subscription revenue has a ceiling: you can only charge a customer so much for software. Credit doesn’t — it scales with the customer’s own volume. That structural difference is why embedded lending has become the most-discussed expansion path for vertical SaaS platforms serving a single industry.

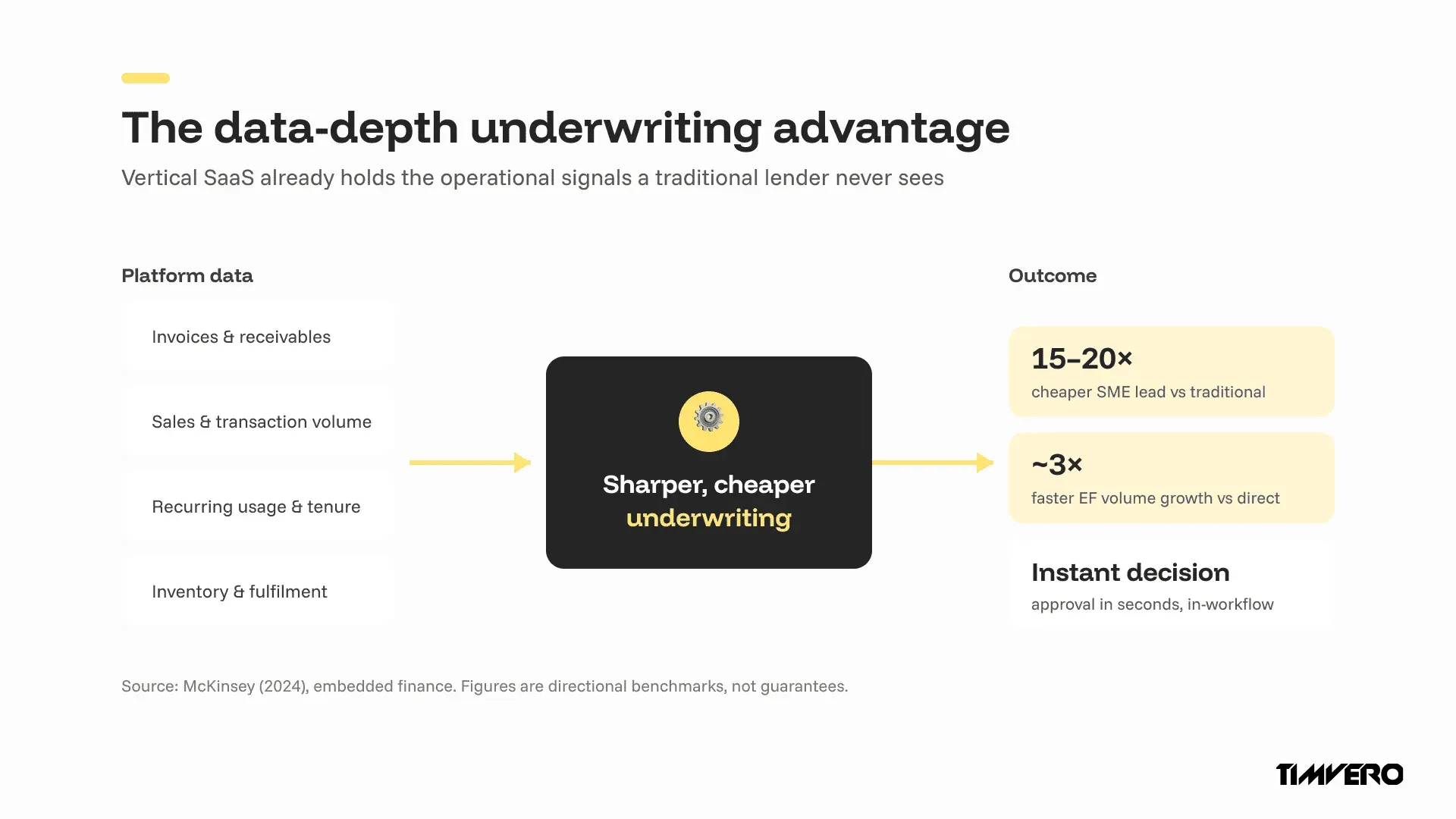

The data-depth underwriting advantage

A vertical SaaS platform sees signals a traditional lender never gets: invoices, sales volume, fulfilment rates, inventory turns, recurring usage. Those signals make underwriting sharper and cheaper than a generic credit pull. According to McKinsey (2024), this data advantage is a core reason embedded-finance volumes in Europe grew roughly three times as fast as directly distributed loans over the past decade.

It also collapses acquisition cost. McKinsey (2024) found that in one major European market, acquiring a qualified SME lending lead through an embedded-finance channel was 15 to 20 times cheaper than a traditional lead. For a platform that already owns the customer relationship, the most expensive part of lending is largely solved before the first loan is written.

Beyond subscriptions: a higher-margin revenue line

Credit deepens engagement, not just revenue. Borrowers interact with the platform far more often during repayment than they do with a passive subscription, which lifts retention on the core product. The combined effect — new credit revenue plus stickier subscriptions — is what makes embedded lending a strategic move rather than a side feature.

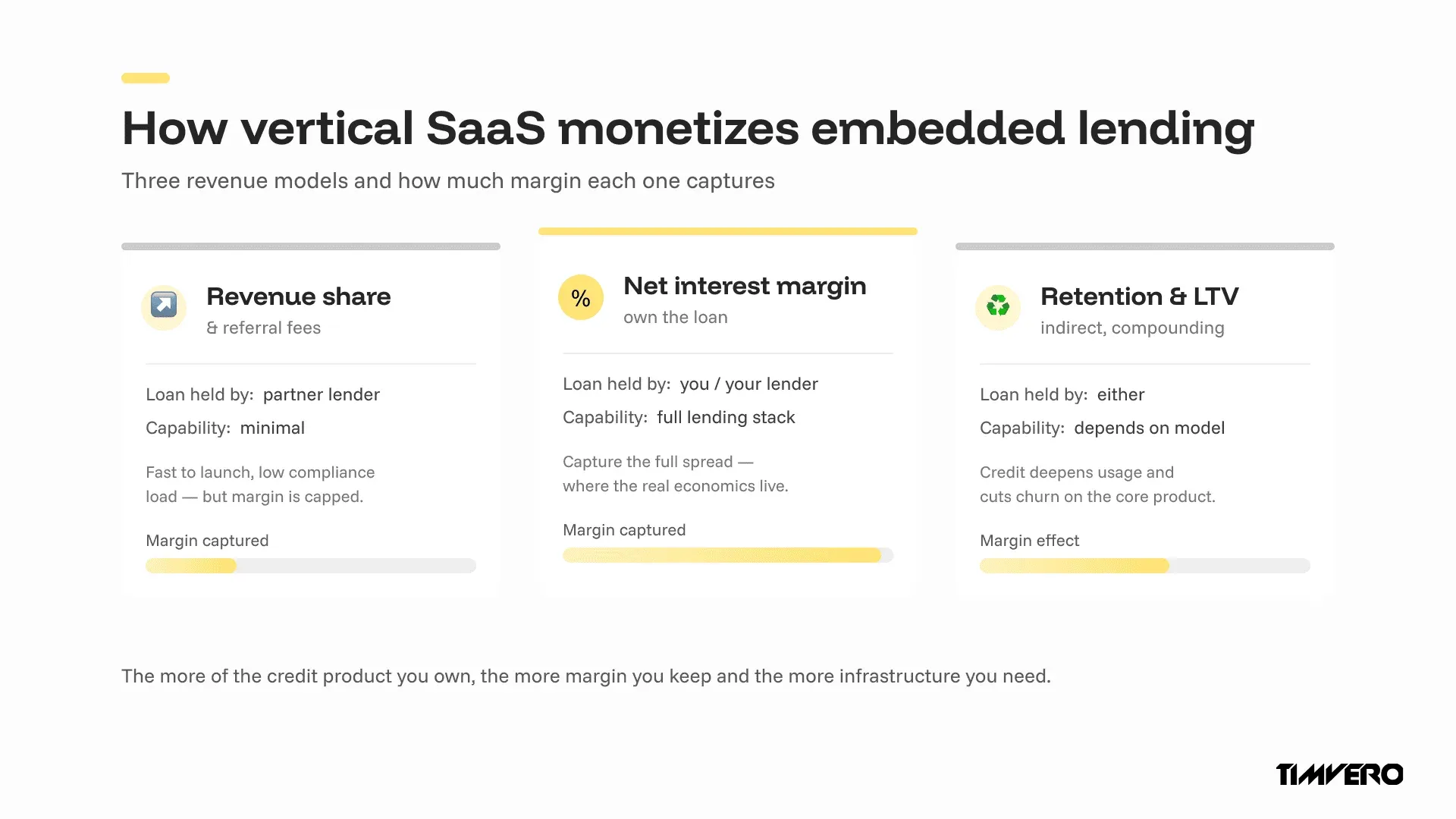

How vertical SaaS platforms make money on embedded lending

There are four ways to monetize an embedded lending program. They are not mutually exclusive, and the mix you choose determines both your revenue ceiling and how much capability you have to own.

Revenue share and referral fees

The lowest-effort model: a partner lender holds the capital and license, and your platform earns a cut of interest and fees, or a flat fee per funded loan. It is fast to stand up and carries little compliance load — but you don’t control pricing, data, or the credit product, and your margin is capped by whatever the partner agrees to share.

Net interest margin — owning the loan

When the platform (or a lender it controls) holds the loan on its own balance sheet, it captures the full spread between funding cost and lending rate. This is where the real economics live. It also requires real lending capability: origination, servicing, accounting, and compliance. The trade-off is direct — the more of the credit product you own, the more margin you keep and the more infrastructure you need.

Retention and lifetime value

Harder to put on an invoice, but real. Embedded credit increases how often and how deeply customers use the platform, which reduces churn on the subscription business underneath. For a vertical SaaS company, a few points of retention can outweigh the direct lending revenue.

Funding the loans you choose to own

The net-interest-margin model raises a question the revenue-share model doesn’t: where does the capital come from? Owning the loan doesn’t require becoming a bank overnight. Most vertical SaaS platforms that hold credit start with a funding partner — a warehouse facility, a forward-flow agreement, or a balance-sheet lender — while keeping the credit logic, customer experience, and servicing on their own platform. What you own is the product and the data; what you source is the capital.

That separation is exactly why the underlying lending system matters. A funding partner will underwrite your facility on the quality of your origination, servicing, and reporting — which means transparent, auditable infrastructure is a financing advantage, not just a compliance checkbox. A platform that can show clean IFRS 9 or CECL provisioning, a full audit trail, and reliable servicing data raises capital on better terms than one whose lending logic sits inside a vendor’s black box.

| Revenue model | Who holds the loan | Margin captured | Capability required | Best when |

|---|---|---|---|---|

| Revenue share / referral | Partner lender | Low (capped by partner) | Minimal | Credit is a side feature; speed over economics |

| Net interest margin | You / your lender | High (full spread) | Origination, servicing, compliance | Credit is — or will become — a core product |

| Retention / LTV uplift | Either | Indirect but compounding | Depends on model | Always — measure it alongside direct revenue |

The pattern is simple: the more of the product you own, the more you earn. That single trade-off is what the “build vs buy vs embed” decision really comes down to.

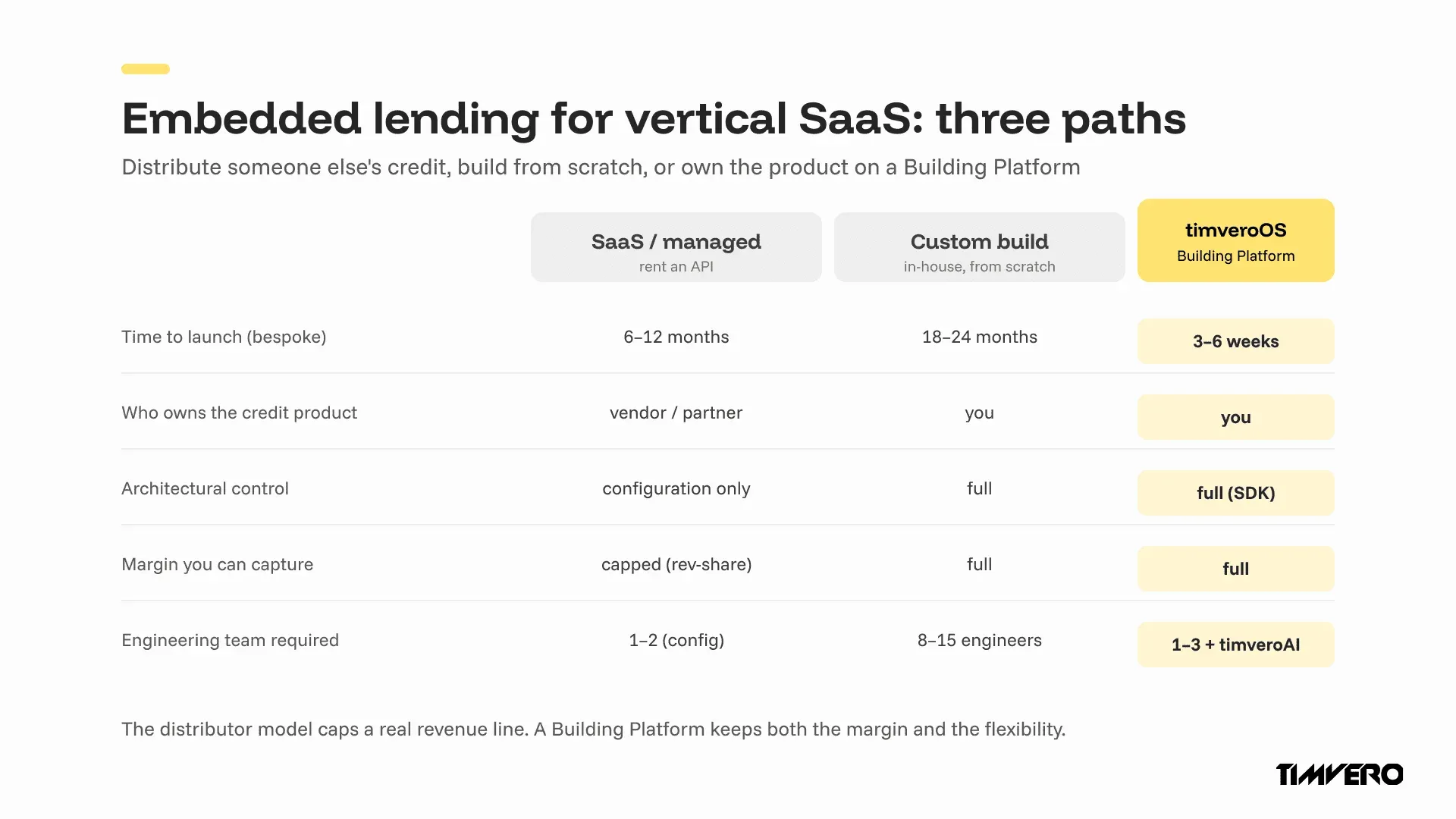

The strategic fork: distribute someone else’s credit, or own the product

Most embedded lending content — and most of the search results for this topic — describe one model only: rent an API, let a provider hold the license and capital, and act as a distribution channel. That works if credit is a convenience feature. It hits a wall the moment credit becomes strategic and you need non-standard structures, your own pricing, and auditable compliance you control.

The SaaS distributor ceiling

A managed or white-label embedded lending product gets you live quickly, but you configure only what the vendor exposes. The first time your vertical needs something non-standard — a usage-based credit line, an industry-specific repayment schedule, a co-borrower flow — you hit an architectural ceiling and join a vendor roadmap queue measured in quarters. For a credit product meant to differentiate your platform, configuration-only is a hard limit.

The custom-build cost

Building a lending stack from scratch removes the ceiling but reintroduces cost and risk: typically 18–24 months and an engineering team of 8–15, with origination, servicing, accounting, and compliance all built before the first loan. For most vertical SaaS teams, that timeline is incompatible with the window embedded lending is opening right now.

The third path: a Building Platform

There is a third path between renting a rigid product and building for two years. A Building Platform like timveroOS ships a working lending system from day one — origination, servicing, accounting, analytics — while giving your engineers code-level access to the underlying building blocks through an SDK (Java/Spring Boot). You start from a running system and shape it at the architectural level, instead of configuring inside a vendor’s limits or assembling everything yourself.

| Criterion | SaaS / managed embedded lending | Custom build (in-house) | timveroOS Building Platform |

|---|---|---|---|

| Time to launch (bespoke product) | 6–12 months on vendor roadmap | 18–24 months from scratch | 3–6 weeks with timveroAI |

| Who owns the credit product | Vendor / partner lender | You | You |

| Architectural control | Configuration only | Full | Full (SDK access to building blocks) |

| Deployment | Multi-tenant cloud only | Self-hosted | Self-hosted or private cloud |

| Margin you can capture | Capped (revenue share) | Full | Full |

| Engineering team required | 1–2 (config) | 8–15 engineers | 1–3 engineers + timveroAI |

| Compliance | Opaque, vendor-controlled | Built from scratch | Explicit building blocks per jurisdiction |

If lending is going to be a real revenue line for your platform, the distributor model quietly caps it. Owning the product on a Building Platform is the only option that keeps both the margin and the flexibility.

How to launch embedded lending fast without losing control

The usual objection to owning your credit product is time. On a Building Platform, ownership no longer means the 18–24-month route — because most of the system already exists and an implementation agent compresses the rest.

timveroAI is a RAG-grounded implementation agent: it is grounded in the Building Platform’s source code, lending ontology, and skeleton library, and it produces the specs, configurations, and code that adapt the platform to your product. It handles 70–80% of implementation work while your engineers keep human-in-the-loop approval, and generated changes run in shadow-run mode — validated against real flows before they go live — so speed never costs you control.

This is also where the architectural differentiators matter most for a vertical SaaS team. Code-level access through the SDK means your engineers extend the building blocks directly instead of filing vendor tickets. Deployment in your own environment keeps your borrowers’ data out of a shared multi-tenant pool. And explicit compliance building blocks — IFRS 9, CECL, audit trails, KYC/AML, jurisdiction-specific reporting — stay transparent and modifiable rather than buried in a black box.

“Most embedded lending offers ask a software platform to choose between speed and ownership — rent a rigid product fast, or spend two years building one you control. A Building Platform removes that choice. You launch a working lending product in weeks and still own the credit logic, the data, and the compliance, because you’re shaping building blocks at the architectural level.”

— Dmitriy Wolkenstein, CEO, TIMVERO

One distinction to keep clean: timveroAI accelerates how you build and change the lending system. The credit decision itself runs on a separate, explainable AI scoring building block that produces auditable reason codes at every decision. The two are different layers — implementation acceleration versus runtime decisioning — and a serious lending product keeps them separate.

What the best embedded lending solutions for vertical SaaS should include

When you evaluate the best embedded lending solutions for vertical SaaS, the comparison that matters is not feature lists — it’s how much of the credit product you walk away owning. Use this checklist:

- Ownership of credit logic. Can you change pricing, risk rules, and product structure yourself, or only what a vendor exposes?

- Data and deployment control. Does your borrower data sit in a shared multi-tenant pool, or in your own environment?

- Non-standard structure support. Can the platform handle usage-based limits, industry-specific schedules, and co-borrower flows without a roadmap negotiation?

- Transparent compliance. Are IFRS 9, CECL, audit trails, and jurisdiction reporting modifiable building blocks, or an opaque “compliance included” claim?

- Time to launch a bespoke product. Weeks, or quarters?

- Margin model. Are you capped at a revenue share, or can you capture net interest margin by owning the loan?

A solution that scores well on all six lets credit become a core, differentiated product line. A solution that scores well only on speed-to-launch is a distribution deal — useful, but capped. For platforms serving regulated or specialized industries, the lending software for fintechs angle and the underlying timveroOS loan management software (opens in new tab) architecture are what make the difference between renting and owning.

Proof: what owning the product looks like in production

Finom, a European business-banking platform serving 200,000+ customers across five EU countries, is the clearest example of a software platform owning its embedded credit product rather than renting it. Finom launched a proactive embedded SME credit line — dynamic limits, multi-country servicing, regulatory reporting — on timveroOS (opens in new tab), reaching banking-grade origination in four months and full servicing in three, with 98% process automation and ROI from day one.

The implementation pattern is what matters for a vertical SaaS evaluation: 80% of the lending infrastructure was supplied ready-to-use, while 100% of Finom’s bespoke requirements were covered — the part a configuration-only product can’t reach.

“Today, we’re running proactive credit campaigns and sophisticated servicing operations on a single platform. timveroOS delivered a competitive advantage under impossible deadlines.”

— Alex Goncharenko, Head of Credit, Finom

Across its client base, the platform supports $5.5B+ in assets under management, operations in 13+ countries, and 7,000+ daily loan applications — evidence that an owned, embedded credit product runs at scale. See the full Finom case study (opens in new tab) for the implementation detail, or start from what embedded lending is (opens in new tab) if you’re earlier in the research.

Frequently Asked Questions

What is embedded lending for vertical SaaS?

Embedded lending for vertical SaaS is credit — term loans, lines of credit, or point-of-sale financing — offered directly inside an industry-specific software platform’s workflow. The platform uses its own operational data (invoices, sales, usage) to power instant underwriting, turning software into a lending channel or owned product.

How do vertical SaaS platforms make money from embedded lending?

Through four models: revenue share on a partner lender’s interest and fees, per-loan referral fees, net interest margin when the loan sits on the platform’s own balance sheet, and indirect gains from higher retention. Owning the loan captures the most margin but requires real lending infrastructure.

What ROI can a vertical SaaS platform expect from embedded lending?

ROI depends on the model. Owning the product captures full net interest margin instead of a capped revenue share, and embedded channels cut SME lead-acquisition cost by 15–20x versus traditional channels (McKinsey, 2024). Retention uplift on the core subscription adds compounding, indirect return.

Should a vertical SaaS company build, buy, or embed lending?

Embed if credit is a side feature; build only if you have 18–24 months and a large engineering team. The third path — a Building Platform — ships a working lending system from day one and compresses bespoke launches to 3–6 weeks, letting you own the product without the custom-build timeline.

How long does it take to launch embedded lending on a Building Platform?

On a Building Platform like timveroOS, bespoke embedded lending products launch in 3–6 weeks with the help of timveroAI, which handles 70–80% of implementation work. As a benchmark, Finom reached banking-grade origination in four months and full servicing in three for a multi-country product.

Who holds the lending license in an embedded lending program?

It depends on the model. In a managed program, the partner lender holds the license and credit risk while the platform distributes. In an owned model, the platform or its lending entity holds the license and risk — and captures the corresponding margin, data, and control over the product.

Ready to launch embedded lending you actually own?

Embedded lending rewards the vertical SaaS platforms that control their credit product, not the ones that rent distribution. See how timveroOS can stand up your program in weeks — with the credit logic, data, and compliance staying yours.

Head of Marketing

Ivan Halynkin leads Growth & Marketing at TIMVERO, the company behind timveroOS and timveroAI. He works across the seam between product and demand — translating composable lending infrastructure into positioning, content, and demos that resonate with banks, credit unions, and fintechs. His writing focuses on what actually moves the needle for digital lenders: origination economics, AI in credit decisioning, and the trade-offs between SaaS lending boxes and building-platform thinking.

LinkedinLatest News

Bank Efficiency Ratio: What It Is and How to Improve It

Best AI-Powered Lending Platforms in 2026: A Buyer’s Guide

What Is Embedded Lending? How It Works and Why It Matters

Best Loan Origination Software in 2026: 10 Systems Compared

Lending Software Beyond SaaS vs Build: The Third Path

How U.S. Banks Should Rethink Credit Card Strategy in a Potential 10% APR Cap Environment

Open Banking Is Quietly Rewriting How Loans Work

Automated Loan Origination: How Lenders Cut Abandonment Rates and Speed Up Approvals

Embedded Lending Platform: APIs and Technical Requirements