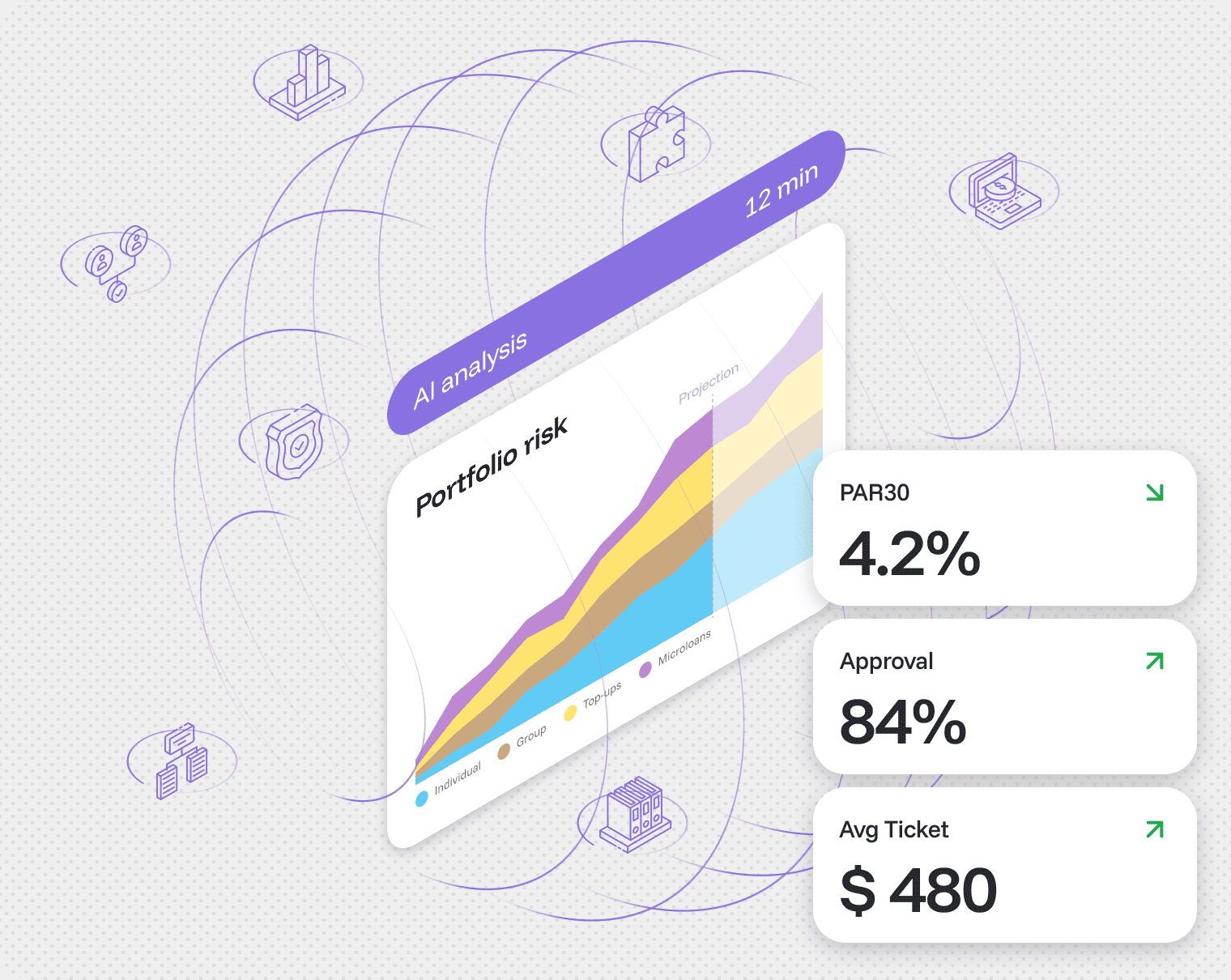

XAI Scoring for Auto Loan Risk and Servicing

The Building Platform’s XAI scoring engine handles runtime credit and risk decisions for auto lending. Two different capabilities of the Building Platform, kept distinct on purpose: timveroAI accelerates implementation, the XAI scoring engine handles runtime decisioning. Models train in your environment on bureau, bank, device, and vehicle data. Every model output, every policy version, every override is logged. Production benchmark: 12x faster decisioning, +20% profit per loan when paired with portfolio analytics.

-

Early Delinquency and Cure Probability

Predict which loans drift toward delinquency 30, 60, or 90 days ahead. Trigger pre-dunning workflows on the Building Platform before charge-off risk crystallizes.

-

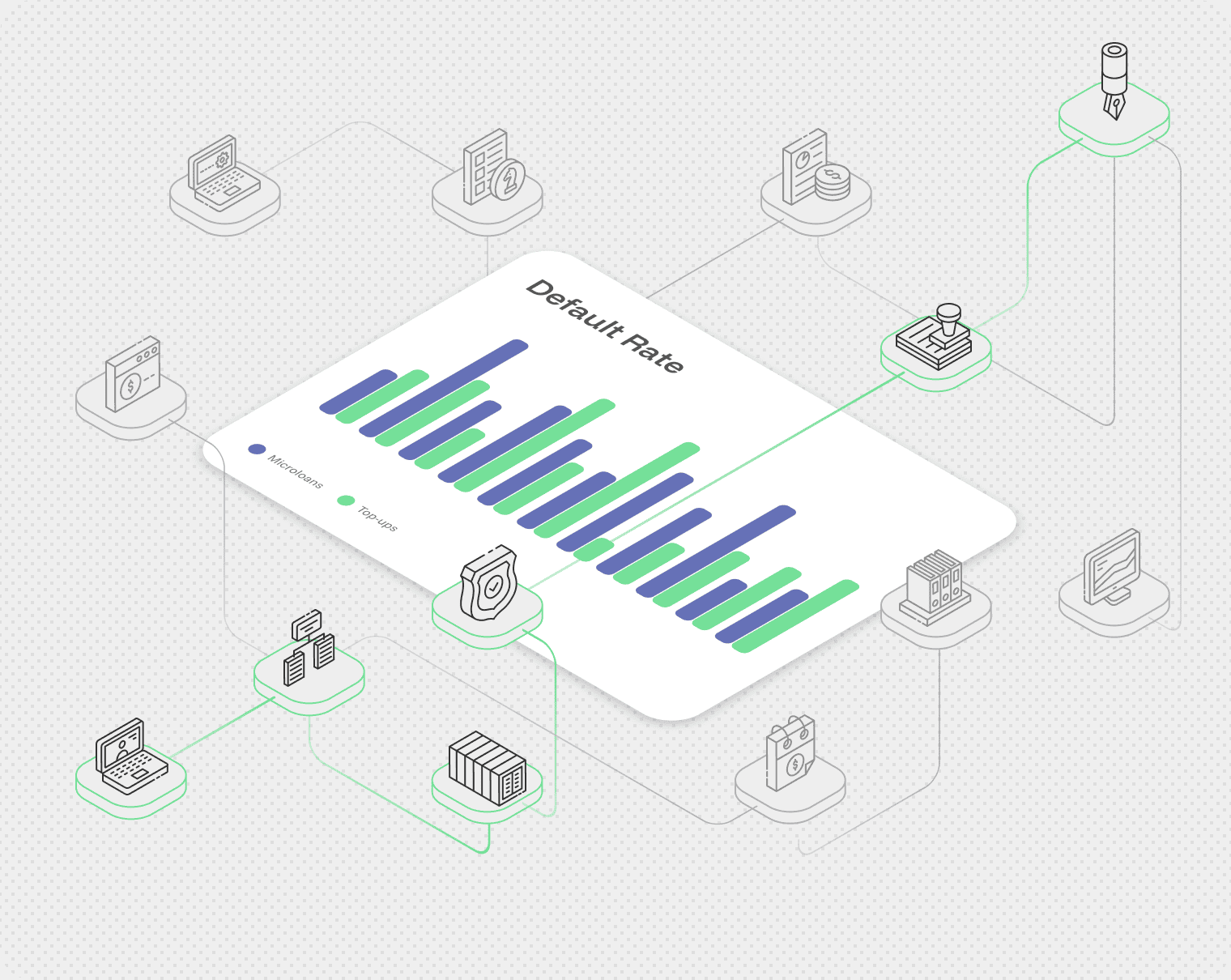

Powerbooking and Synthetic ID Detection

Compare application data against bureau, device, and vehicle signals to flag inflated trim packages, ghost co-applicants, and synthetic identity patterns at funding.

-

Depreciation-Aware LTV Risk Monitoring

Track LTV pressure as vehicle collateral depreciates and loan balance amortizes. Surface portfolio concentration risk before it materializes.

-

Outreach and Dunning Cadence Optimization

Score each delinquent loan on cure probability and recommend the contact channel, timing, and message that maximizes recovery without burning customer relationships. See full XAI scoring and portfolio analytics for runtime decisioning detail.